{kind=link}

- Most currency pairs confined to tight ranges, stocks set for new records

- Sterling opens a touch higher as Britain gets a new health minister

- Big week ahead, featuring an OPEC meeting and a US employment report

Wall Street set for more gains but currencies quiet

Global markets are quiet on Monday, with news flow being rather light and movements subdued across most asset classes, as traders keep some powder dry ahead of crucial events later in the week. Dollar pairs are generally stuck in a holding pattern, caught between opposing forces. Hopes that the regime of cheap money is slowly drawing to an end are being negated by the euphoric mood in equity markets.

Wall Street hit a new record high on Friday in the wake of some disappointing US inflation data, which helped calm concerns around an imminent normalization of Fed policy. President Biden added more fuel to the rally over the weekend after he walked back his threat to veto the trillion-dollar bipartisan infrastructure package unless it is accompanied by a separate plan that focuses on ‘human infrastructure’.

Ergo, the good news keeps on coming for stock markets, which are set to round off their fifth consecutive month of gains. Even the Fed’s recent bombshell was unable to make the market bleed, highlighting that investors don’t think a couple of rate hikes over a couple of years are going to dramatically alter the landscape for equities.

UK gets a new health minister, Sydney goes into lockdown

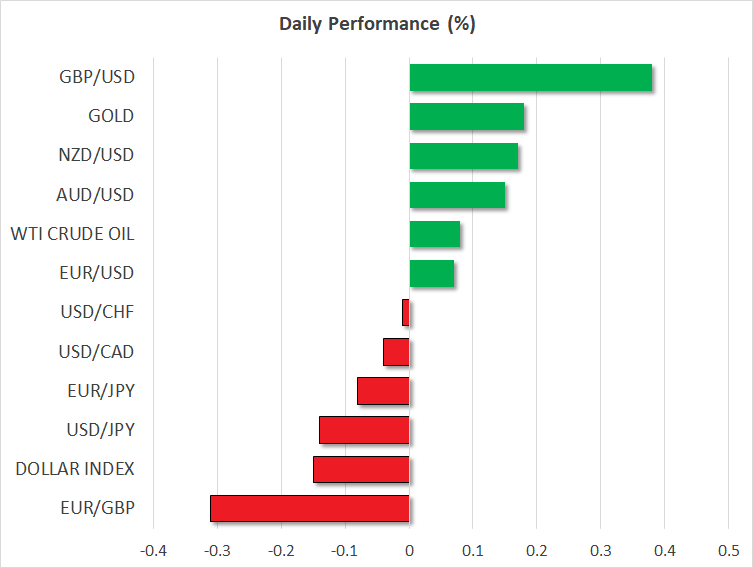

The only currency that’s making any decent moves on Monday is the British pound, following the resignation of the nation’s health minister on Saturday, who was caught breaking social distancing rules. This was the latest scandal to shake the Boris Johnson government, although judging by the market reaction, traders ultimately saw it as a net-positive development.

Sajid Javid – the previous Finance Minister – will now return to lead the health department. This has sparked optimism for stronger synergies between the two ministries as the economy takes the final step towards a complete reopening. The logic goes that if the former Chancellor is managing public health, he’s also likely to prioritize the economy’s wellbeing.

Of course, this isn’t any huge development in the bigger picture but it’s something for markets to work with on a quiet session. As for the pound, the overall trajectory still seems positive with the UK set to outperform many nations economically, likely leading the BoE to exit asset purchases much earlier than the likes of the ECB or BoJ.

In Australia, news that the country’s most populous city of Sydney went back into lockdown saw the aussie dollar open with a minor gap lower today, although it managed to recover quickly. This period is the danger zone for Australia as temperatures are low and vaccinations have been slow so far. On the bright side, the market hasn’t really cared about covid numbers for a while.

Central bankers kick off exciting week

The economic calendar is low key today, with the only noteworthy events being some speeches by central bank officials. The BoE’s outgoing chief economist Andy Haldane will get the ball rolling at 12:00 GMT, before the Fed’s Williams hits the wires at 12:45 GMT. Then at 14:00 GMT, the focus will turn to ECB Vice President de Guindos. Wrapping things up will be the Fed’s Harker at 15:00 GMT and Quarles at 17:00 GMT.

While today’s session may be slow, the rest of the week seems quite exciting, with an OPEC meeting on Thursday and a US employment report on Friday to spice things up. This edition of nonfarm payrolls could single-handedly determine whether investors spend the summer positioning for a withdrawal of cheap money or whether all that is premature.