{kind=link}

- BoE unlikely to shake markets today, minor upside risks for sterling

- Dollar back in the ring as Fed lets the hawks out

- Stocks elevated, another heavy dose of Fed-speak coming up

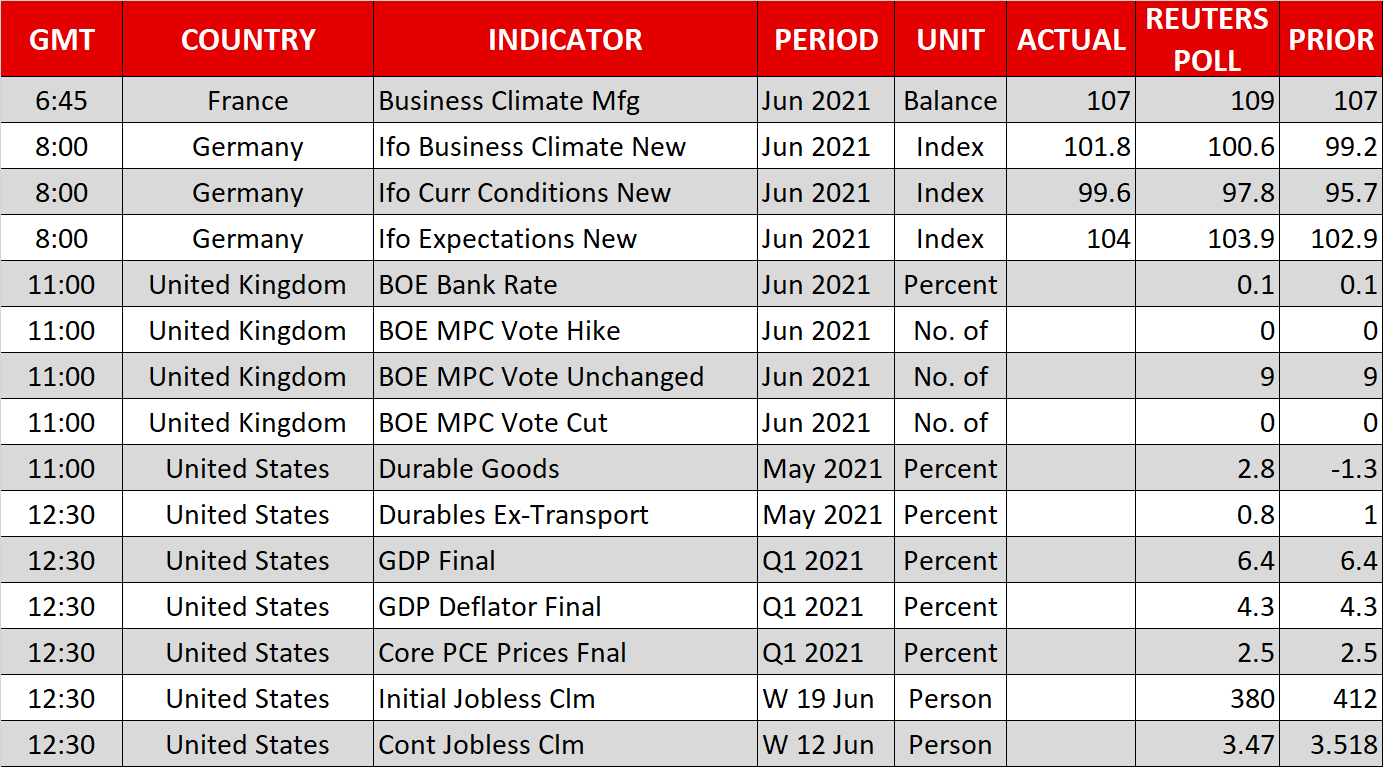

BoE set to maintain optimistic tone

All eyes will be on the Bank of England today. This is one of the smaller meetings without a press conference or updated economic forecasts, so any seismic policy signals are rather unlikely. Still, there is a risk that the BoE upgrades its language around the economy, which is firing on all cylinders.

Demand is booming across the UK as consumers have been unchained and the latest PMI surveys suggest this spell of powerful growth is likely to persist. Meanwhile, inflation already breached the BoE’s target of 2% in May and seems destined to keep accelerating thanks to raging supply constraints, according to the same surveys.

The only cause for concern is the delay of the economy’s complete reopening because of the new delta variant, but considering that this only affects a few isolated sectors, it shouldn’t be a huge deal. The tariff threats from the EU have subsided lately, with reports suggesting a ‘ceasefire’ is imminent.

As for the pound, it got knocked down lately as the dollar came back to life, but the longer-term trajectory seems promising. The BoE could be the first to raise rates again, with markets currently pricing in the first move for November next year, so sterling could shine against low-yielding currencies like the yen, franc, and euro as the theme of policy divergence crystallizes.

Dollar stays afloat as Fed lets hawks loose

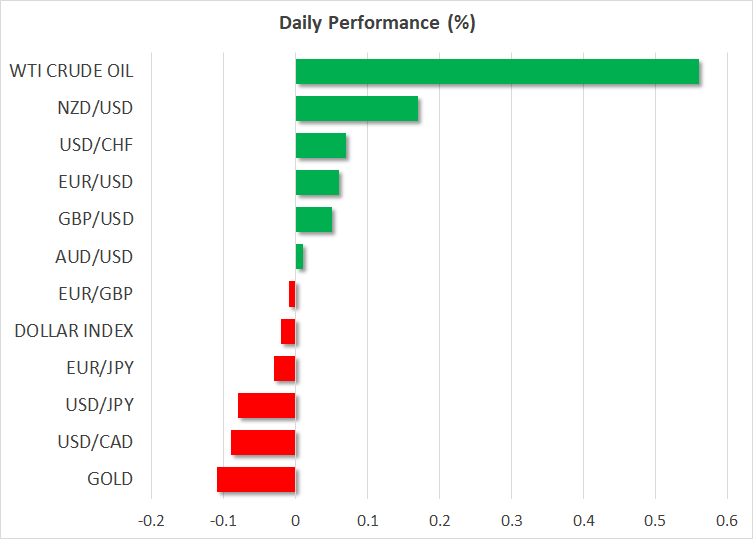

It was an eventful session in the FX arena. The dollar took some early fire after a disappointing round of PMI data, only to bounce back once investors digested the encouraging details of those surveys, with some hawkish Fed commentary adding fuel to the move.

The Markit composite PMI fell to 63.9 in June, from a record high of 68.7 previously, which sent the signal that growth may have peaked. However, the details revealed that this slowdown really comes down to companies being unable to meet demand because of worsening supply shortages, not any cooling of the US economy.

With supply disruptions getting worse instead of better, there is a very real risk that inflationary pressures continue to snowball, forcing the Fed to accelerate its normalization timeline even further. Echoing this exact view was the Fed’s Bostic, who argued this inflation episode may take longer to fade and that he’s in favor of a rate increase next year already.

For the dollar to really regain momentum, the missing piece of the puzzle is the labor market. It is still missing some 7.5 million jobs for a full recovery, which is the primary reason the Fed thinks this inflationary shock will fade by itself. Hence, next week’s edition of nonfarm payrolls will be absolutely critical for whether the tapering ball gets rolling soon.

Stocks hold near records, oil cheers OPEC news

Wall Street remained in a holding pattern near its record highs on Wednesday, but that is impressive in itself considering the discouraging news investors had to grapple with lately. The incredible resilience markets have shown to signals that the era of cheap money is drawing to an end suggests there will be no taper tantrum this time. It’s going to take more than a super-slow normalization cycle to make stocks bleed.

Over in energy markets, crude oil keeps going from strength to strength, even following reports that OPEC is looking to raise its production by 500k barrels a day in August. With prices trading at these levels, market participants apparently feared an even bigger supply hike, hence this was seen as a positive surprise.

Finally, there’s another flurry of Fed speakers coming up today. Bostic and Harker will get the show going at 13:30 GMT, before Williams hits the wires at 15:00 GMT ahead of Bullard at 17:00 GMT.