{kind=link}

The Swiss National Bank will wrap up its meeting at 07:30 GMT Thursday. It will most probably keep rates at the lowest level globally and stress that it will continue to intervene in the FX market, as the franc has started to regain ground. Looking ahead though, it’s difficult to be positive about the franc in an environment where foreign central banks start withdrawing liquidity but the SNB doesn’t.

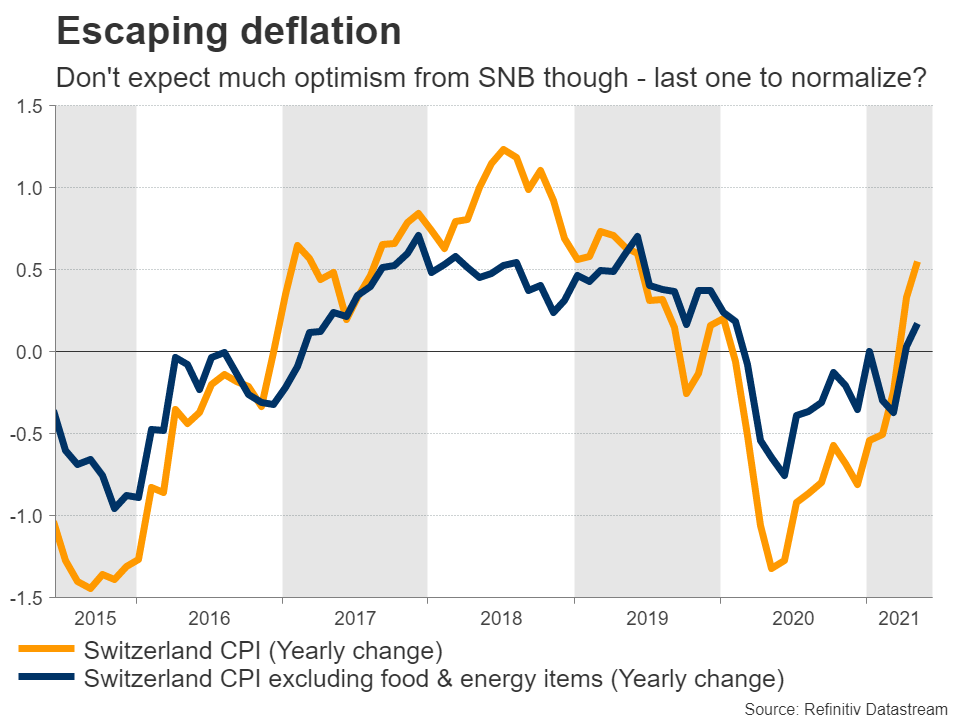

Return of inflation

The Swiss economy escaped from deflation lately, but don’t expect any optimistic signals from the central bank this week. The improvement has been minor so far and most importantly, any positive remarks could fuel more demand for the franc, which the SNB desperately wants to avoid.

A stronger exchange rate makes exports less competitive abroad and pushes down on the prices of imported products, dampening both economic growth and inflationary pressures. As such, the SNB has been actively intervening in the FX market for years now to weaken the franc, which it considers ‘highly valued’.

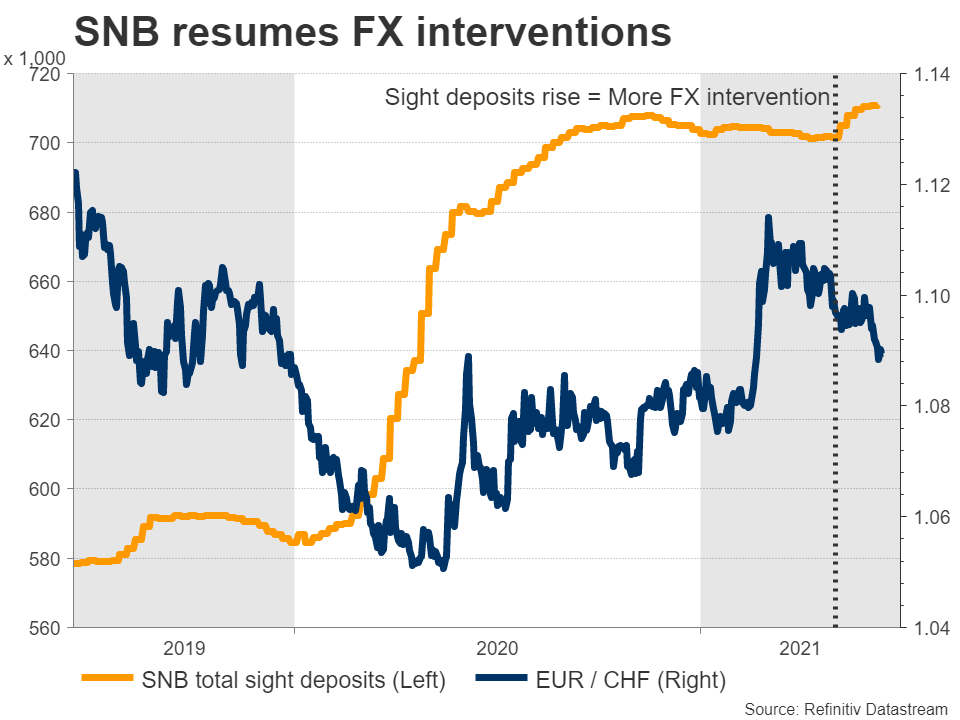

The Bank stopped intervening in the first quarter of the year, as the franc was losing ground on its own thanks to the spike higher in foreign bond yields. However, the second quarter has seen the franc regain some strength, forcing the SNB to resume interventions.

This meeting will likely be uneventful. The Bank will probably stress that it has no plans to exit negative rates or stop FX interventions. Various SNB officials have said as much lately and if they simply repeat this old message, any market reaction is unlikely.

Last to normalize?

In the bigger picture, the dominant theme over the next years will be which central banks raise interest rates first to keep inflation under control. The SNB could be the last to do so. The other contender is the Bank of Japan. Both are economies with chronic deflation problems.

That’s bad news for the franc. In an environment where foreign interest rates are rising but Swiss ones aren’t, the franc would become even less attractive.

The SNB will be thrilled about this. Waiting longer than everyone else to normalize monetary policy would kill two birds with one stone – it would minimize downside risks to the economy and demolish the franc.

In this respect, it’s almost impossible to be bullish on the franc. Not only could it suffer because of widening rate differentials, but safe-haven demand for the currency could also fade as the global recovery powers up. And if that wasn’t enough, the bulls will also have to fight the SNB at every step of the way.

What could revive the franc?

The main risk to this view would be some economic or political shock that hits global markets and sparks panic, sending investors towards defensive assets. Perhaps some monster covid mutation that is highly resistant to vaccines or some geopolitical ‘accident’ in the South China Sea or the Middle East.

That would probably breathe life into the franc. That said, whether any strength lasts is another story, as the SNB would start to intervene overtime. In other words, the longer-term trajectory for the Swiss currency seems negative, but the journey probably won’t be a straight line.

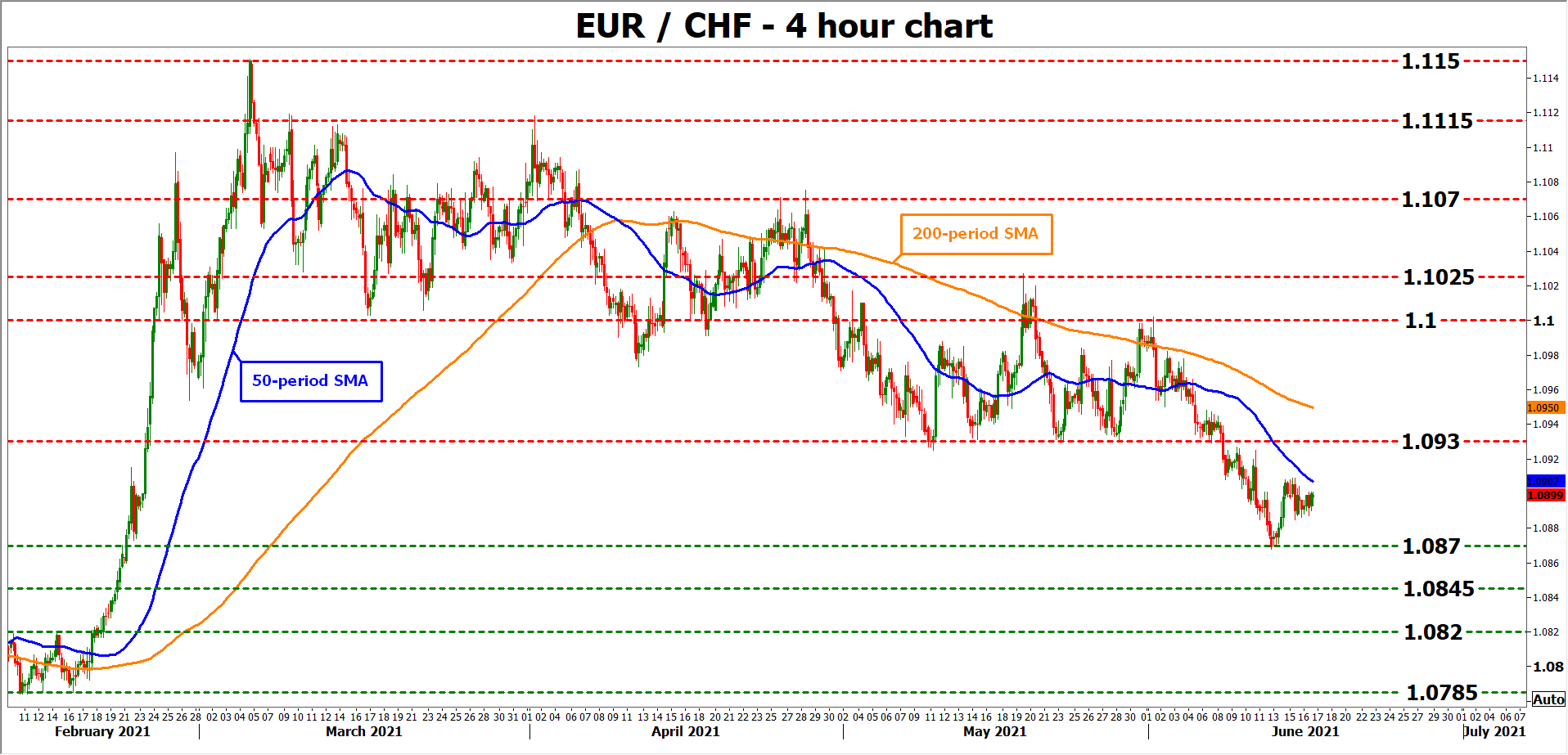

Taking a technical look at euro/franc, if buyers retake control and manage to overcome the 1.0930 zone, the next obstacle may be the latest high near 1.1000.

On the downside, initial support to further declines may be found at the 1.0870 low, a violation of which would turn the focus towards the February peak of 1.0845.