{kind=link}

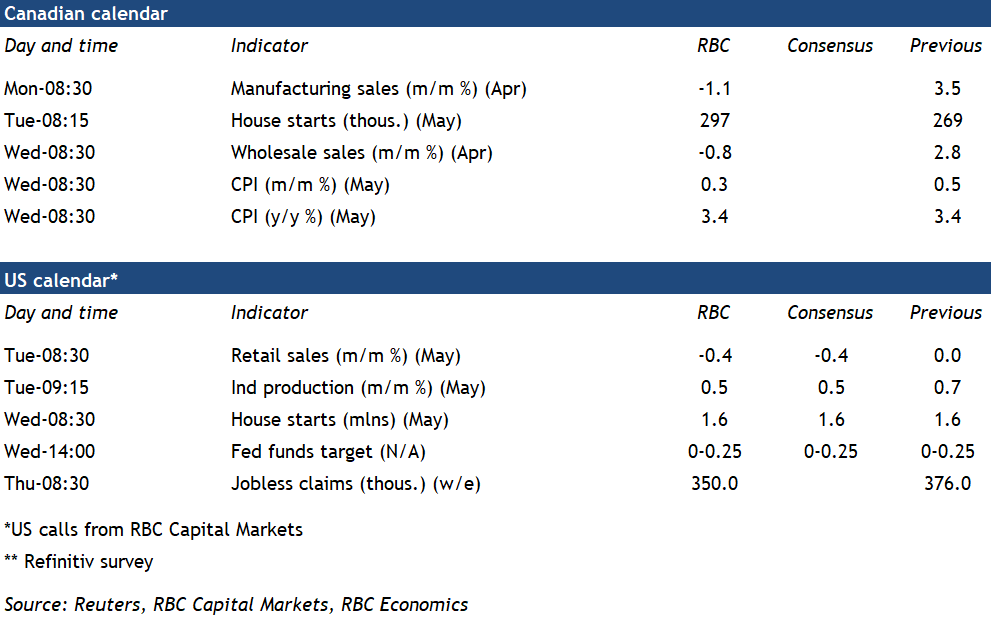

We expect next week’s inflation report to show the headline rate held firm at 3.4% in May—matching April’s rise. This would mark the strongest back-to-back increases in a decade, although the jump is off of an exceptionally low base set a year ago, when activity ground to a halt during the initial COVID wave. Surging year-over-year growth in energy prices is expected to be ‘transitory’ and will begin to ease going forward. But policy makers will nevertheless be watching carefully for any signs that underlying, more broadly-based, price growth is firming up.

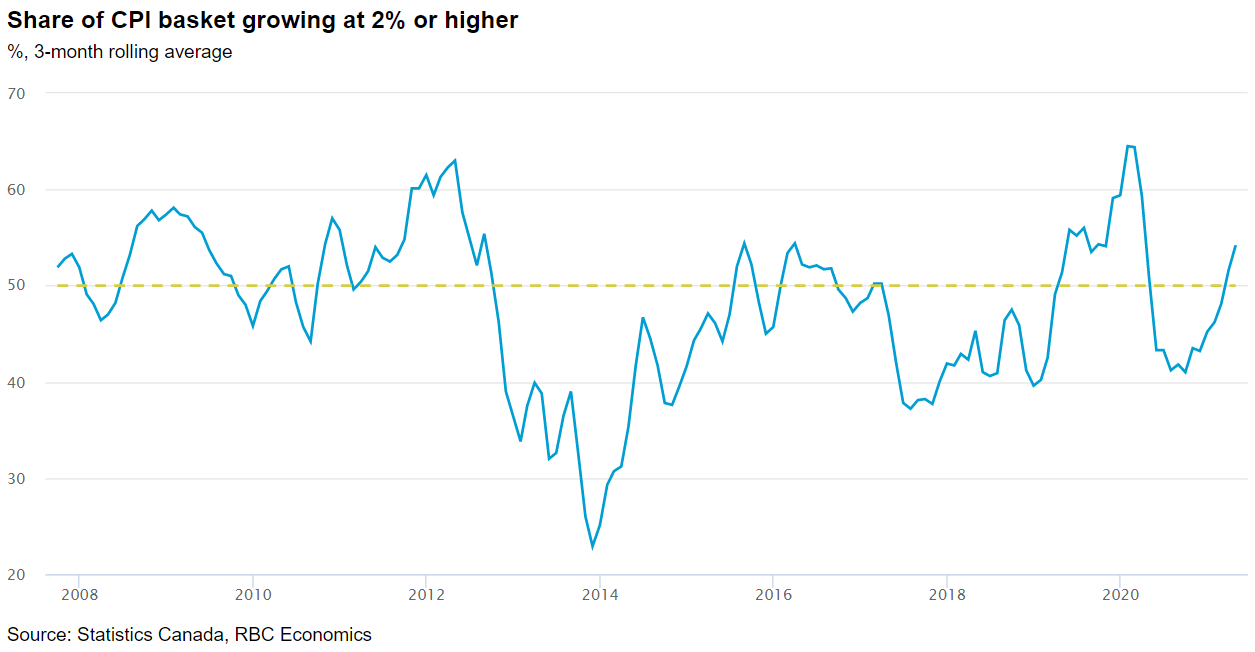

By our own count, more than 50% of the goods and services in the consumer basket posted price increases above 2% in April compared to a year earlier. That’s before the surge in household demand that’s expected to happen as virus containment measures ease in second half of this year. The Bank of Canada’s preferred core measures are likely to edge higher once again—with the ‘median’ and ‘trim’ measures already running above 2%.

Week ahead data watch:

- The US Fed is expected to leave interest rates unchanged despite a surge in CPI growth and an increasingly optimistic near-term economic outlook.

- Canadian housing starts are likely to show another firm reading at 297K in May, well above longer run trends. The solid pipeline of building permits points to the strong momentum continuing in the near term.

- Early estimates for April manufacturing and wholesale sales have already been released. Both show pullbacks, with the global chip shortage weighing heavily on auto production in particular.

- Active COVID cases have fallen substantially in Canada and the national positivity rate sits at ~ 2.6%. The vaccination rollout continues to gain steam. Over 60% of Canadians have at least one dose and almost 10% are fully vaccinated.