{kind=link}

Sterling has been languishing for almost a month, unable to find fresh impetus above February’s peak. On Friday, the monthly GDP growth figures (06:00 GMT) for April could be good news for the UK economy, though whether the data can energize the pound bulls remains to be seen as the spread of the Indian variant puts the final stage of reopening and hence growth prospects somewhat in jeopardy.

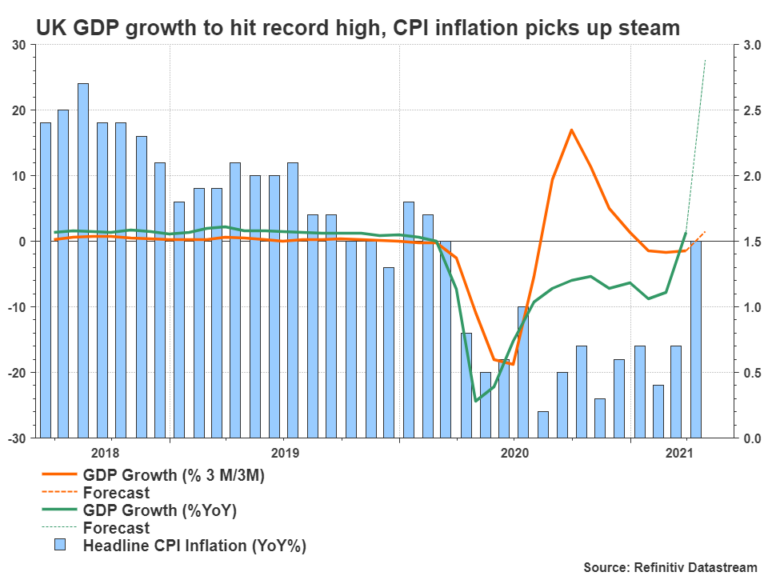

UK GDP growth could hit record high

The British government opened the roadmap for easing lockdown restrictions in mid-April, allowing non-essential shops to resume activities as the vaccination rollouts were a national pride back then, progressing above target and faster than those in other developed economies. As a result, retail sales soared by more than double the pace analysts anticipated in April, while consumer confidence surged beyond pre-pandemic levels, indicating a consumer-led growth boom in the second quarter.

On Friday, monthly GDP growth figures for April could give form to this optimism. Although the month-on-month change is expected to be tenuously higher at 2.2%, analysts estimate a whopping boost to 1.5% in the three-month average gauge compared to -1.5% seen previously, while the annual expansion is forecast to skyrocket to a record high of 27.6% versus the minimal 1.4% reading posted in March. The industrial and manufacturing production data released on the same day are also projected to print a record double-digit growth despite a potential monthly pullback.

Indian variant could ruin full reopening plans

In mid-May the government moved to the next reopening stage, lifting bans on retail and hospitality businesses. Hence, the economy has likely further build its positive momentum in the second quarter and the growth sparkle could even extend to the third quarter if the remaining restrictions are removed as planned on June 21. That said, the latter is still in doubt as the spread of the fast-transmittable Indian variant, which elevated UK infection cases to the highest since the end of March, could delay the complete reopening for at least two weeks, especially if hospitalizations prove to be a wave and not a ripple.

Perhaps Boris Johnson would not like to derail the progress the economy has made and could keep some important limitations in place when the official announcement is made on June 14. Nevertheless, the UK is at the top list of the most vaccinated countries, aiming to inoculate all adults by the end of July. Therefore, hopefully another wave of infections could be relatively more manageable.

Pound could shrug off GDP data

Given the caution around the recent mild resurgence in virus cases and expectations that the expansion could get new legs in the second quarter, the pound may stay on the sidelines in the wake of the GDP readings on Friday. Instead, the FOMC policy meeting on June 15-16 and the reaction in the dollar could be the major catalyst for the pound in the week ahead, as the scenario of a tighter monetary policy in the US takes roots in investors’ mind. If the Fed concedes to tapering calls, seeing a withdrawal of stimulus sooner than initially estimated, a potential rebound in the dollar could knock the pound sharply lower.

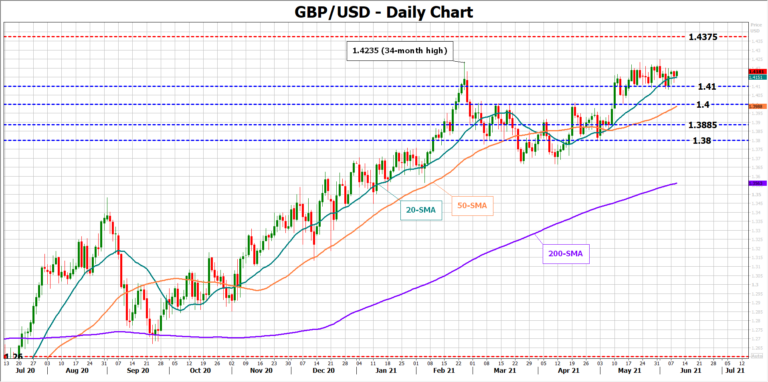

From a technical perspective, the bulls could take charge if pound/dollar breaches February’s peak of 1.4235, a move required for an advance towards the 2018 top of 1.4375.

On the downside, the 1.4100 number could be the threshold for a steeper decline towards the 50-day simple moving average (SMA) and the 1.4000 mark.

A week later the Bank of England will next review its policy settings on June 24, and although no inflation reports are due this time, it would be interesting to see how policymakers will guide markets through a tighter policy following the step towards ending the QE program in the previous gathering and the rising speculation for a rate hike in late 2022. Note that this meeting will be the last for BoE chief economist Andy Haldane before he steps down, while the release of employment and CPI inflation figures will precede the policy decision next week.