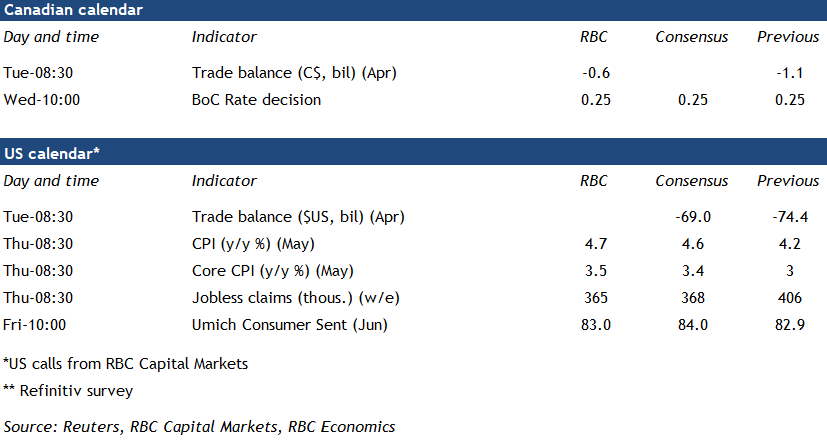

{kind=link}

No meaningful change to monetary policy guidance is expected at next week’s Bank of Canada meeting. Recent economic data has come in somewhat softer than the bank had projected in the April Monetary Policy Report, but not significantly enough to prompt a re-think on the appropriate path of monetary policy support. The 5.6% (annualized) gain in Q1 GDP was close to the BoC’s 7% projection, once incorporating upward revisions to prior quarters. But output fell by 0.8% in April – the first decline in a year – following tightening in restrictions nation-wide. That said, a wide range of government supports remain in place for households that are losing work and businesses that are losing sales. With vaccination rates continuing to ramp up significantly, and provinces beginning a gradual reopening process, the economy is set to rebound substantially beginning in June.

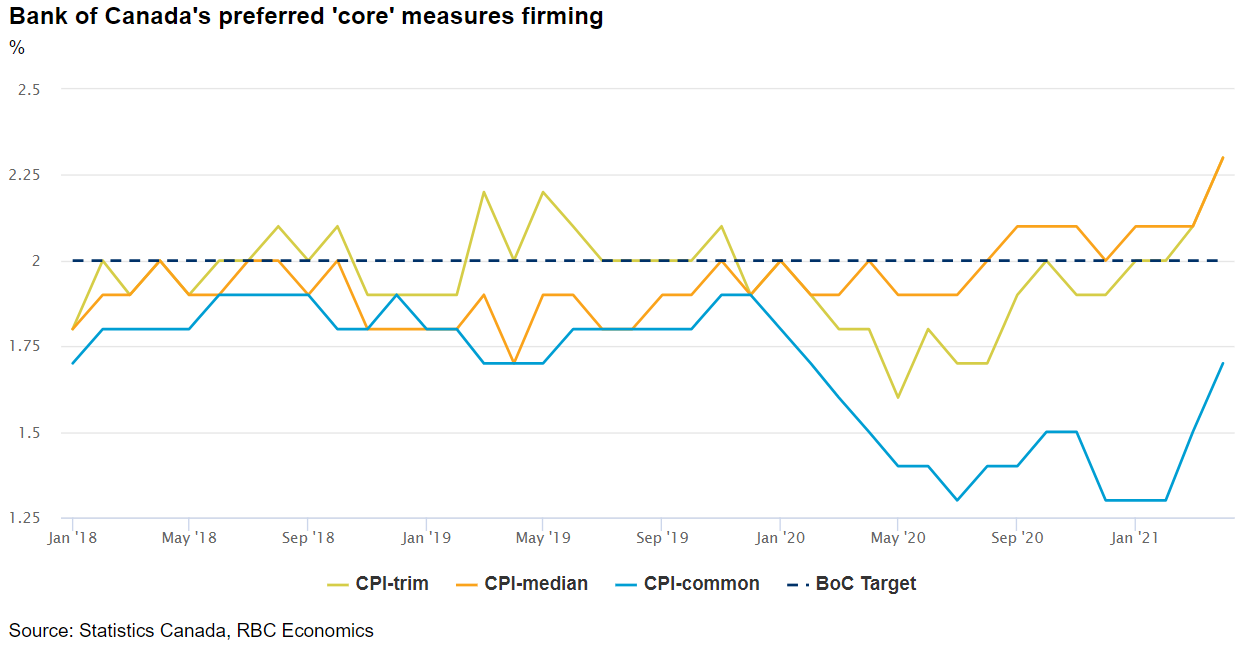

Indeed, with the near-term growth outlook increasingly bright, concerns have shifted to rising production input prices and the prospect for a sharp recovery in consumer demand to stoke inflation pressures. For now, the BoC is likely to posit that near-term increases in consumer price growth rates will prove ‘transitory.’ But there have also been signs of harder-to-dismiss firming in most measures of underlying price growth gauges, including the BoC’s own preferred core measures edging up towards or above the 2% inflation target. For next week’s meeting, the overnight rate is expected to be held at 0.25% with markets watching for any change in language regarding further adjustments to the asset purchase program. We expect a stronger economic growth backdrop and firming underlying inflation pressures will ultimately prompt the central bank to begin to reduce policy accommodation with a further tapering of the QE program later this year with rate increases unlikely until the second half of 2022.

Week ahead data watch:

- April’s Canada trade data is expected to show a narrower $0.6 billion deficit, with both exports and imports falling due to lower auto production tied to the ongoing global semi-conductor shortage.

- Headline US CPI is expected to have remained above 4% in May, distorted in part again by the recovery in energy prices. Though similar to April, a shortage of used cars and more demand for air travel are expected to continue to push up prices for transportation in May.