{kind=link}

U.S. Highlights

- Job growth picked up in May, with the economy adding 559k jobs and the unemployment rate falling to 5.8%.

- ISM indexes pointed to strong growth in manufacturing and services sectors in May, though supply constraints linger.

Canadian Highlights

- Canada’s economy grew at 5.6% (annualized) in the first quarter, below consensus estimates for a 6.8% print. Considering the health restrictions on the service sector in place during the quarter, this was still a decent outturn.

- This resiliency did not extend into the third wave. Flash GDP estimates for April point to a contraction in activity during the month (-0.8% m/m). Today’s Labour Force Survey release hints at continued weakness in May, with job losses totaling 68K and a nearly flat performance for hours worked (+0.1%).

Financial – An Equity Market Check-Up

- Equity market momentum has come off the boil. While corporate earnings continue to improve, a high bar has been set. At the same time, economic data surprises have become fewer and farther between. Investors are patiently waiting for the path forward to become clear.

- Though downside risks are always present, the economic recovery is likely to be supportive of corporate earnings and financial conditions should continue to support investor sentiment. This provides a favorable backdrop for risk assets.

U.S. – Music to American’s Ears

An overture to May’s economic performance, this week’s data set a positive tone, which we hope will play accelerando from now onward. Friday’s much-anticipated employment report came in slightly lower than forecasters hoped for but had an upbeat spirit with hiring picking up in key sectors and the unemployment rate falling to 5.8% from 6.1% in April.

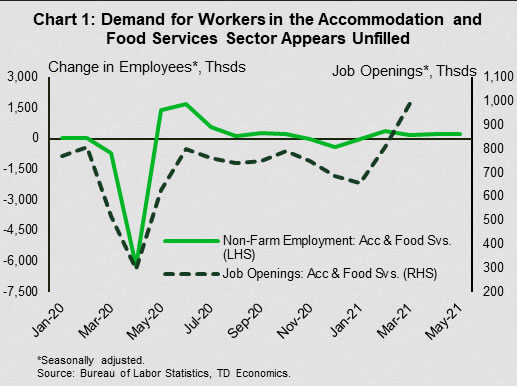

While challenges in finding workers, especially in the low-wage segment, continue to be highlighted in qualitative reports, (including the Fed’s June Beige Book), the pickup in job growth pushes back, at least a little, on the notion that labor shortages are a major constraining factor to the economic recovery. Accommodation and food service firms have been singled out as a sector with a sizeable number of unfilled positions, as echoed in job openings data (Chart 1). This is leading some businesses to offer sign-on bonuses and higher wages. Fortunately, they appear to be working. The sector continued to lead job growth in May, with 221k positions added, accounting for 40% of all the net jobs created in the month.

According to research by the Federal Reserve Bank of Atlanta, wage pressures are concentrated in low-wage service occupations that come with the highest customer contact. While expanded unemployment benefits may be contributing to a reluctance of some people to rejoin the workforce, wage pressures point to a well-functioning labor market where workers are offered higher pay to compensate them for the higher risk of exposure to COVID-19. Nonetheless, half of states have decided to halt federal unemployment subsidies by mid- to end of June in an effort to bring more workers to the labor market. This may hasten the job search for some but will leave those unable to come back to work due to health concerns or lack of childcare to suffer losses in income.

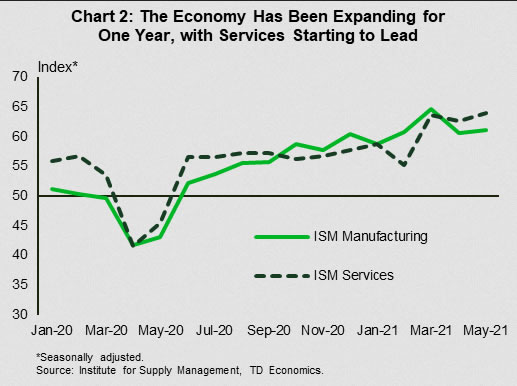

Other economic data also played in a major key this week. The Institute for Supply Management’s (ISM) reports on manufacturing and services sectors registered a full year of growth in a single month in May. The services sector broke its growth record set earlier this year in March, while maintaining an advantage over the manufacturing sector – a phenomenon more typical to “normal” times (Chart 2). Both sectors’ demand indicators gained momentum, while supply bottlenecks seem to have reached a high note with both backlog of orders sub-indexes hitting historical highs.

The Fed continues see these “supply-demand mismatches” as transitory. In a speech this week, Fed Governor Brainard noted that these mismatches are evident “on both the employment and inflation sides of [the Fed’s] mandate”, but also highlighted that the biggest contributors to core PCE last month were categories that are not the typical drivers of inflation. With that, it may be a good time to lower the volume on inflation worries, sit back and enjoy the tune of growing economic momentum.

Canada – The Final Stretch

Canada’s economy has shown its grit during the second wave of the virus (see our latest Quarterly Economic Briefing). The National Accounts for the first quarter kicked off this week’s data-heavy calendar. Economic growth in the first quarter came in at 5.6% (annualized), below consensus estimates for a 6.8% outturn. This was still a solid performance considering the restrictions on activity and elevated caseloads seen during the quarter. The monthly GDP picture for March was even more encouraging with a 1.1% increase in real GDP in the month providing a strong handoff into the second quarter.

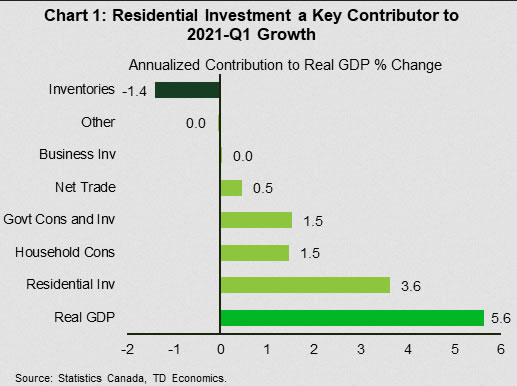

Unfortunately, the details of the report were less stellar. Positive contributions from consumption and net trade were encouraging, but residential investment was by far the largest contributor to growth (Chart 1), up a whopping 43.3% (annualized) in the quarter. This is reigniting concerns that the Canada’s economic recovery has been overly reliant on housing and government spending. What’s more, the resiliency witnessed during the winter does not appear to have extended into the third wave. Statistics Canada provided a flash estimate for April’s real GDP, pointing to a 0.8% contraction in activity during the month. This didn’t come as a surprise. Hours worked barely nudged in response to the second wave, but saw a sizeable decline in April.

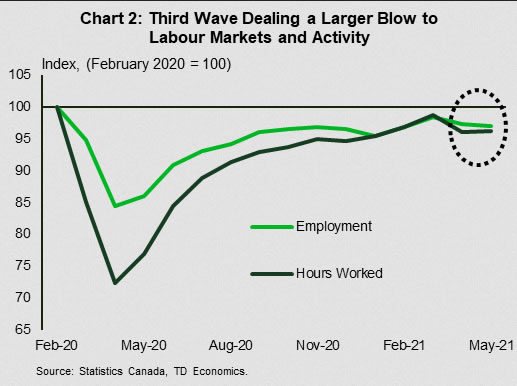

This week’s other top-tier data release – May’s Labour Force Survey, corroborates his narrative and suggests that weakness continued into May (Chart 2). The economy saw 68k job losses, with hours worked almost flat on the month (+0.1% m/m). With most provinces staying the course on restrictions during May, weakness was broad-based, with 8 of the 10 provinces experiencing job losses. A drop in the overall participation rate is another concern, and will be watched closely for signs of potential scarring in the coming months.

Notwithstanding the string of weak data, higher frequency indicators suggest that June will be the turning point for the Canadian economy. Health indicators have seen a sharp improvement in recent weeks, with cases in free fall across most provinces. Vaccination rates continue to increase, with Canada’s now the highest across large advanced economies (though second dose administration still lags). With 9 of the 10 provinces having released reopening plans (See our Provincial Tracker), a strong rebound should begin this month. Pent-up demand, a hefty savings cushion, and strength in the U.S. economy should help rotate growth away from housing and the public sector to consumer spending and business investment.

What does this mean for the Bank of Canada’s announcement next week? First quarter growth was below the Bank of Canada’s earlier estimates. The third wave has also had a more dampening effect than initially expected. Nonetheless, with a strong rebound in the cards for the third quarter, the central bank is unlikely to alter its messaging. The Bank of Canada has been among the less dovish this year, changing its forward guidance on monetary policy and beginning to taper its asset purchase programs. We expect this messaging to continue and remain of the view that the central bank is likely to hike its overnight rate in late 2022.

Financial – An Equity Market Check-Up

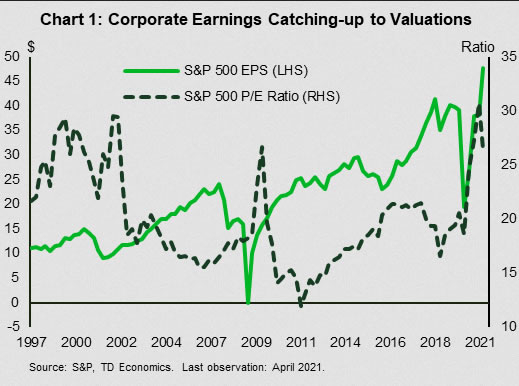

With the price of everything from running shoes to washing machines rising on high sales volumes, the profits of large corporations are surging. This has resulted in the earnings per share of S&P 500 companies reaching new all-time highs, more than double what they were a year ago. At the same time, the equity price advance witnessed over the last year has slowed. The S&P 500 and the Global Dow (ex-US) indexes have leveled out over the last two months, though they are still up approximately 10% over 2021. The trend is even more apparent in the NASDAQ Composite, which has been range-bound for all of 2021, after outperforming in 2020. Though investors might bemoan the relative stability in equities, this has allowed earnings to catch-up to high equity prices. This dynamic has led to an improvement in equity valuations (Chart 1).

The long-term driver of equity prices is corporate earnings. With a robust economic recovery, the outlook for corporate profits is encouraging. The consensus call for earnings per share of the S&P 500 is expected to be 50% higher by the end of 2022 than it was at the end of 2020. That suggests the growth rate in profits could be triple that of nominal GDP growth over the same time period.

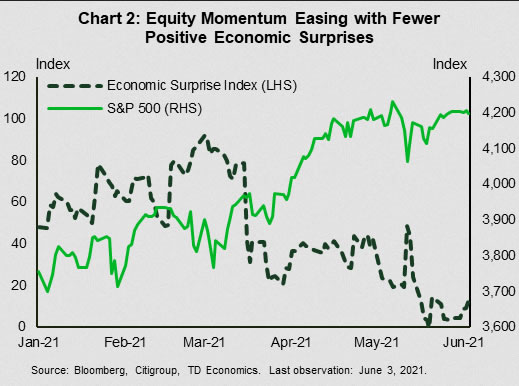

The economic narrative is compelling, but stock prices have largely priced this outcome. In other words, the bar for profits has been raised. A significant move higher in equities will require expectations for corporate earnings to move even higher. Though earnings for the first quarter have been solid, real-time economic data has been more settled, and largely come in at or below admittedly buoyant expectations (Chart 2). .

This has resulted in a number of clients voicing concern about the vulnerability of equities. They wonder whether flat equities are in for a Wile E. Coyote moment – waiting to fall once investors realize that the economic growth narrative is crumbling beneath their feet. To that point, equities typically drop 10% to 15% once a year and it has been a solid 16 months without a retracement. There is always a risk of a correction, but it is unlikely to persist for long. Today’s employment report, which showed strong wage gains, along with the beat in ISM manufacturing and services this week, should assuage fears on this front.

The bottom line is that the current economic recovery is in its early innings and has a long way to run. The economy is set to grow well above its trend-pace over the next two years, supporting even stronger growth in earnings. Additionally, loose monetary policy is still in place and will be for some time. In spite of the risks and recent slowing in equity momentum, the fundamental backdrop still favors equities and risk assets in general.