{kind=link}

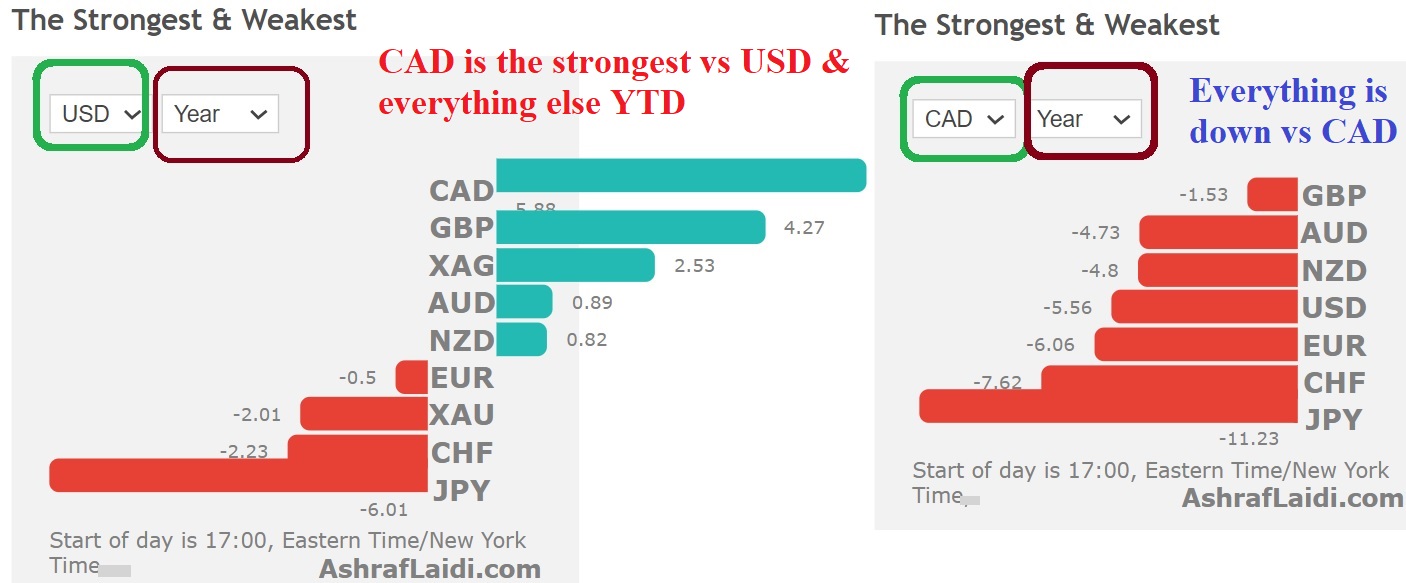

Crude oil broke out as OPEC+ confirmed it will follow its script to slowly return production but the Canadian dollar failed to follow. Much of that may have been the result of a strong bid in the US dollar to start the month but the June seasonal trends aren’t great for USD.

Oil challenged the March highs five times in May before finally breaking through on the first day of June, rising more than 3% to crack $70 in Brent and $68 in WTI. The OPEC+ decision was no surprise but the commentary from oil ministers was also constructive and cohesion appears to be strong.

OPEC, like everyone else in the oil market, is now waiting to see what happens with Iran nuclear discussions. We tend to think that a return of that oil is fully priced in but how fast supply ramps up is a wild card. For now the market is signaling that crude is destined to follow other commodities much higher.

So why then didn’t the loonie follow it? USD/CAD touched a marginal new two-year low at 1.2005 but couldn’t break through the figure and climbed to 1.2075. The answer is that a broad US dollar bid hit that was likely flow driven. ISM manufacturing data was close to expectations as supply bottlenecks continue to cloud the clarity around the numbers but the underlying metrics are strong. The numbers likely weren’t behind the dollar bid, which was also counterintuitive to a dip in yields.

For USD/CAD it may only be a matter of time. The 1.20 level is a key psychological level but is also the 2018 low, making it doubly important. If oil can hold at these levels through an Iran deal, it would be an incredibly powerful buy signal for crude and sell signal for USD/CAD.

Seasonally, there is also some good news for commodity currencies. June is the 2nd strongest month for CAD, AUD and NZD over the past 20 years. It’s also a stronger month for oil.

In general, it’s a soft month for the US dollar, with USD/CHF particularly soft, falling in 10 of the past 11 years. It’s also the third best month for EUR/USD.

In equities, there’s an interesting divergence were it’s a solid month for the Nikkei 225 but the second worst month over the past 20 years for the S&P 500.