{kind=link}

The central bank theme will continue over the next seven days with policy meetings by the Reserve Bank of Australia and Bank of England. The RBA will probably maintain some caution after weak inflation figures but there is some speculation the BoE could start to taper its asset purchases as early as the May meeting. On the data front, the nonfarm payrolls report is due out of the United States. However, after the Fed once again dismissed talk of an early withdrawal of stimulus at its FOMC meeting, employment numbers out of Canada and New Zealand might stir more reaction in FX markets.

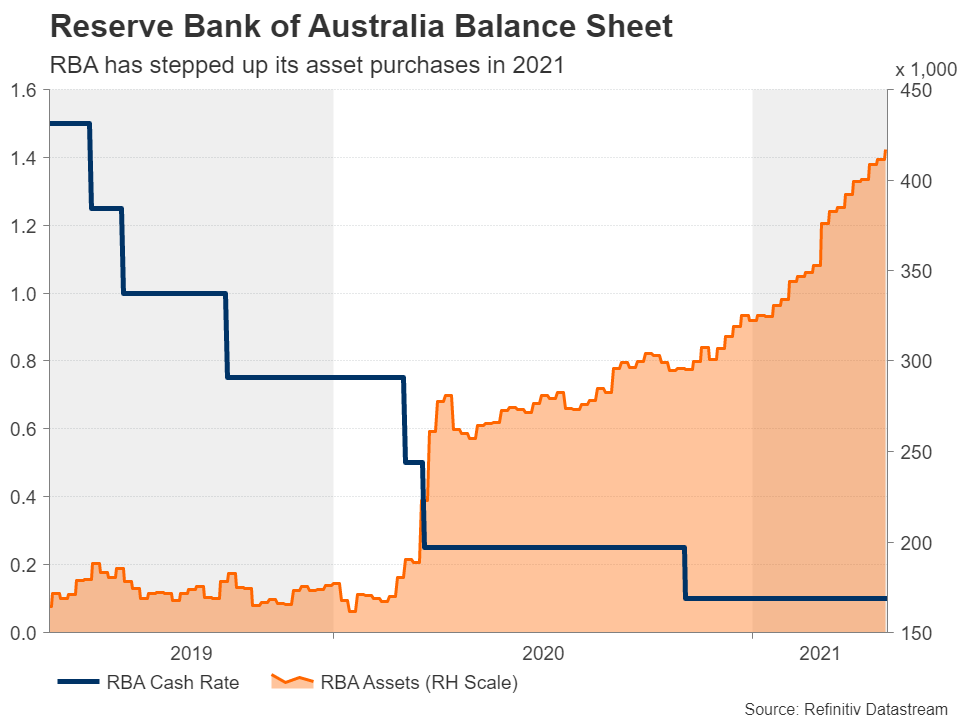

RBA to update forecasts, keep policy unchanged

The Reserve Bank of Australia has been one of the unexpected doves of the central bank world during the pandemic, launching aggressive quantitative easing and yield curve control programmes. Having said that, the RBA does have a tendency to mislead markets with overly optimistic growth forecasts and there might be a repetition of that next week when the Bank publishes its quarterly economic projections on Friday. Ahead of that though, the May policy decision is due on Tuesday.

No change in either rates or QE is anticipated next week as the RBA’s second round of A$100 billion in bond purchases only began a few weeks ago. It is highly likely that a third round will be announced over the summer and the updated forecasts might provide some clues on this. In the meantime, investors will be watching to see if there will be any shift in tone in the policy statement. Inflation data released in the past week revealed price pressures remain subdued in Australia. There’s also the added threat of a regional hit to growth from the virus escalation in India and Japan.

Should the RBA talk up these risks, the Australian dollar might struggle to make much headway just as the US dollar’s yearly uptrend has gone into reverse.

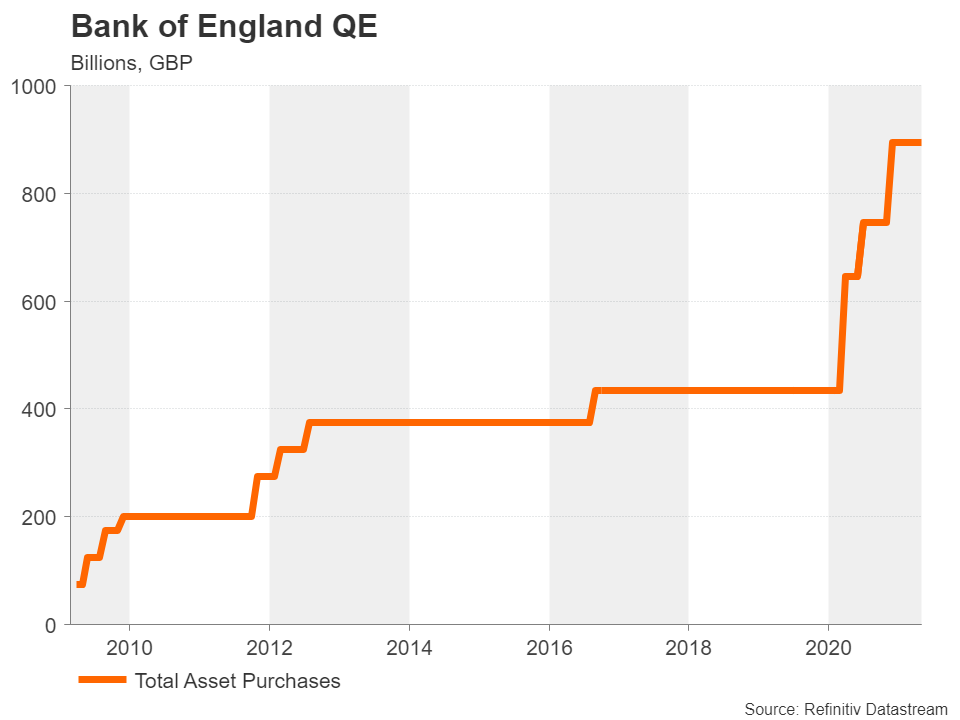

Will the BoE follow the BoC’s lead?

Britain’s lockdown has only just ended and economic output is already soaring, at least according to the flash PMIs for April. The latest remarks from policymakers indicate the Bank of England is confident the economy will rebound strongly in the current and next quarters. Hence, growth forecasts will probably be revised higher in the Bank’s quarterly Monetary Policy Report on Thursday. Investors will also be keeping an eye on the revised inflation forecasts as there is some evidence of higher input costs in the UK.

The rapid turnaround in the virus picture on the back of the prolonged lockdown and successful vaccine rollout has spurred talk of QE tapering by some analysts. However, there have been very few clues of such a move so it doesn’t seem very probable that policymakers would reach a decision as early as next week’s meeting. But the Bank might communicate such an intention on Thursday. If it does, the likely scenario is that the BoE will want to slow down the pace of asset purchases but spread them over a longer period of time.

Any tapering signal would come as a shock to the markets so the pound could jump higher on the news, though political storms could limit any gains. Voters in Scotland go to the polls on May 6 for Scottish parliamentary elections. Pro-independence parties are expected to secure a majority, which could force Westminster to authorise another Scottish independence referendum. Local council elections in England will also be watched as Boris Johnson’s Conservative party has been hit by sleaze allegations. A poor performance for the pro-business Tories could weigh on sterling.

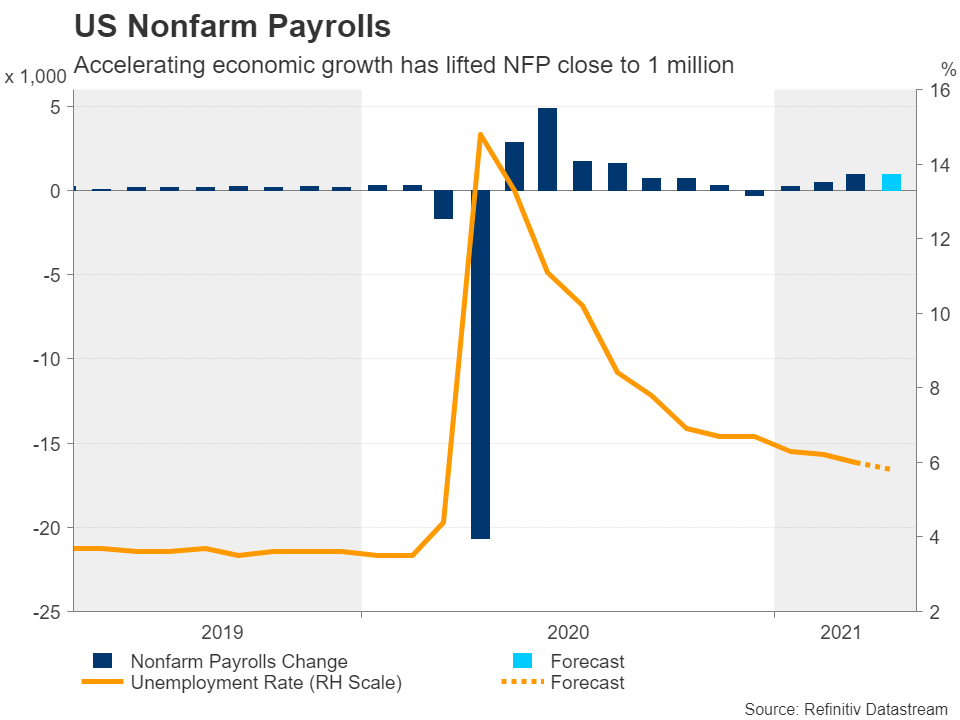

Dollar could shrug off another outstanding US jobs report

It’s going to be a packed data week across the Atlantic starting with the ISM manufacturing PMI on Monday. Factory orders will follow on Tuesday and the ISM’s non-manufacturing composite is due Wednesday. Forecasts for all three are for an improvement over the previous period and Friday’s nonfarm payrolls report is not expected to buck the trend. After the impressive +916k gain in March, the US economy is on course to have added another 925k jobs in April. This would push the unemployment rate down to a new post-pandemic low of 5.8%.

However, the Fed has become dubious of the official jobs data lately, indicating that it believes the true jobless rate is much higher. The Fed not only wants the labour market to recover fully from the virus crisis but to also get unemployment to below pre-pandemic levels. Some are worried that the excessive focus on achieving full employment will stoke inflation just as there’s price pressures brewing from other sources.

But Fed chief Jerome Powell made it clear in his post-meeting press briefing on Wednesday he wants to see several months of strong data before opening a debate about whether or not to pull back some of the stimulus. Markets aren’t so convinced as Treasury yields have started to firm again, though the dollar’s bearish bias hasn’t altered materially. A bumper NFP report isn’t likely to either.

Canadian lockdowns: a ‘temporary’ blow to jobs market

The Canadian dollar has skyrocketed to more than 3-year highs, extending its gains after the Bank of Canada reduced its weekly bond purchases by a further C$1 billion at its April policy meeting, having cut them by a similar amount back in October. The BoC is now officially the first major central bank to have begun the process of withdrawing the pandemic era emergency stimulus. A surprisingly powerful rebound in the labour market in February and March likely contributed to this decision.

However, fresh lockdowns in some provinces in April are expected to have set back the recovery so Friday’s employment numbers are anticipated to be much weaker than the previous months’ prints. Nevertheless, with Canada now having accelerated its vaccination pace, investors are hopeful the latest lockdowns will be the last. Still, the loonie looks vulnerable to some profit taking following its recent winning streak and poor data could be the trigger.

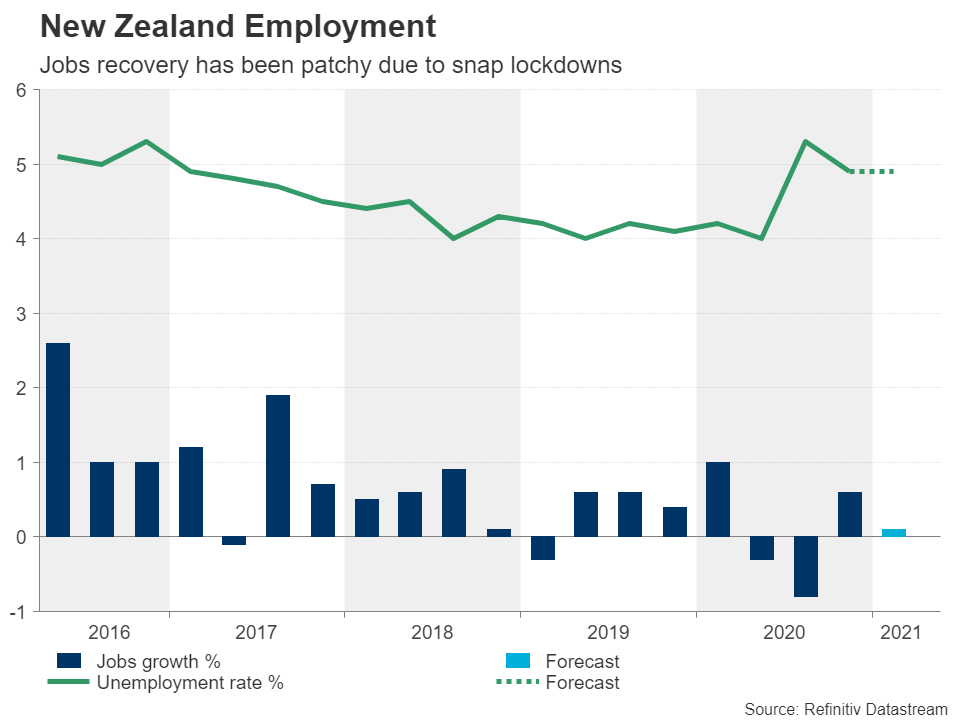

New Zealand’s jobless rate might have ticked up in Q1

New Zealand will also be publishing jobs figures next week. Despite having maintained a low infection rate, New Zealand’s recovery has not been any less bumpy than other countries. The country’s largest city – Auckland – has been in an out of lockdown and fresh restrictions in February were bruising for consumers and businesses. Hiring is therefore also expected to have suffered a slowdown and the unemployment rate might have ticked up in the first quarter. But should the quarterly data out on Wednesday not point to any deterioration in the labour market, it would suggest there was a quick rebound in March.

This could boost the New Zealand dollar, which is currently approaching two-month highs versus the greenback, as it would bolster expectations that the Reserve Bank of New Zealand could soon start to wind down its large-scale asset purchase programme.