{kind=link}

- Level of GDP back within 1% of pre-shock (Q4/2019) levels, remaining gap expected to close quickly as virus threat eases

- Remaining weakness heavily concentrated in high-contact hospitality sectors

- Surge in household incomes from government stimulus checks will support go-forward spending recovery

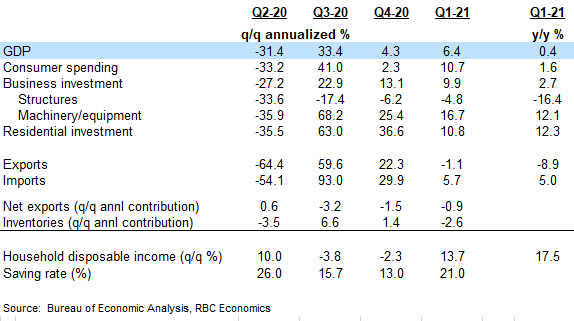

The increase in Q1 GDP was widely expected with the US economy continuing to grow through the winter. Consumer spending rose almost 11% (at an annualized rate) in Q1 – bringing spending back just shy of pre-shock levels on rising demand for goods.

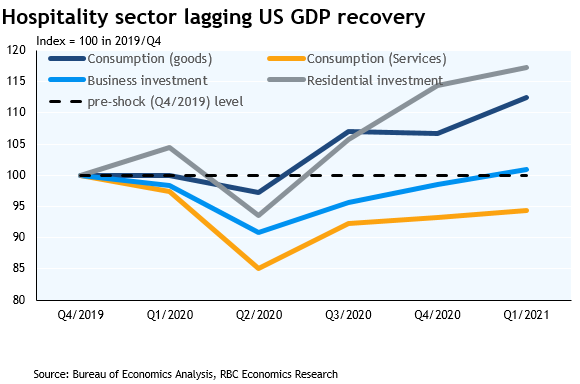

Household spending on services remained almost 6% below pre-shock levels with the virus threat keeping a lid on spending in the high-contact hospitality sectors. But that weakness in service-sector spending will also ease along with the virus threat as the pace of vaccination continues to ramp up.

Another round of stimulus checks and improving labour markets boosted household disposable incomes by another 13.7% (not annualized) in Q2, sending the household saving rate up to 21%. Households have ample purchasing power to boost spending as containment measures ease.

Outside of those high contact service sectors the recovery has been stronger. Business investment was back slightly above pre-shock levels as of Q1 already, while residential investment and consumer spending on goods are already running well-above those levels. Exports also remain soft relative to pre-shock levels, but those are expected to continue to increase going forward with vaccination also ramping up among close US trading partners.