{kind=link}

The US employment report for January will hit the markets at 13:30 GMT Friday. Forecasts point to another soft report, which would confirm that the labor market recovery is plateauing. But that may not be as bad as it sounds for markets, as another disappointment could pressure the politicians to speed up the massive relief package they’ve promised. In this sense, the risks surrounding the dollar and equities from this dataset seem asymmetric and tilted to the upside.

Slowing down

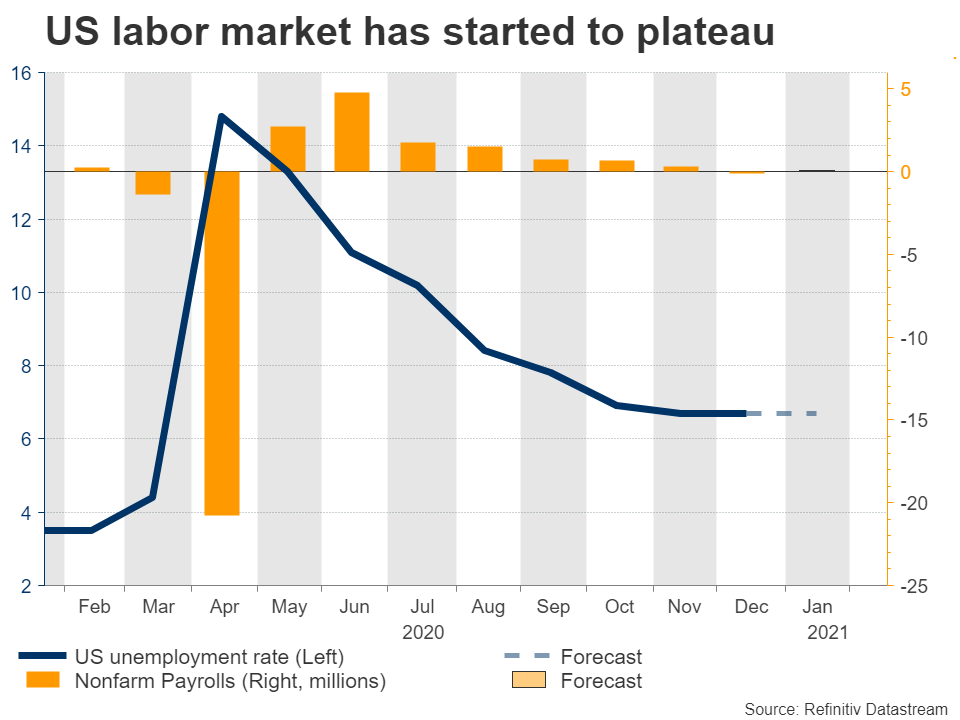

There’s been a striking divergence within the US economy lately. Even though the latest PMI surveys suggest large businesses are doing great, the labor market is starting to show real signs of stress amid ongoing lockdowns and restrictions in several states.

The economy lost 140k jobs in December, and weekly jobless claims suggest this softness persisted into January. The forecast is for nonfarm payrolls to rise by 50k, but that increase wouldn’t even be enough to keep up with US population growth. The unemployment rate is expected unchanged at 6.7%, where it has been stuck since November.

Asymmetric risks

Now in terms of the market reaction, the risks surrounding the dollar and stock markets from this dataset seem tilted to the upside. Let’s explain.

If there is a positive surprise, that’s good news for future consumption and by extension for stocks. Additionally, a strong print could intensify speculation about how soon the Fed might begin to scale back its QE program, which is positive for the dollar.

On the flipside, a minor disappointment is unlikely to inflict much damage on either asset. More signs that the recovery is losing steam would imply the Fed will keep its extraordinary support measures in place for longer, which is encouraging for equities.

As for the dollar, more Fed support is bad news, but a disappointment could also put more pressure on Congress to approve the $1.9 trillion relief bill quickly, and raise the chances of a separate infrastructure package down the road. That would imply a stronger economy, potentially negating the negative Fed effects on the reserve currency.

Having said all this, US employment reports have lost their ‘bang’ in recent months. The market reaction nowadays is usually minor and fades within a few minutes. It has essentially become an intraday volatility event, not something that sparks new trends like in the past.

The bigger picture

Now looking at the broader outlook for the dollar and equities, it seems positive as well. In terms of stocks, the economy is healing, the vaccine rollout is progressing well, the Fed is all-in, and there’s massive government spending in the pipeline.

The main downside risk is whether the existing vaccines will be effective against all the mutated strains of covid. If even a single strain proves to be resistant to the vaccines, the narrative that everything is going back to normal later this year could take a serious blow. However, even in this case, the timeline for re-opening the global economy would simply be pushed back a few months, so any episode of risk aversion is unlikely to last very long.

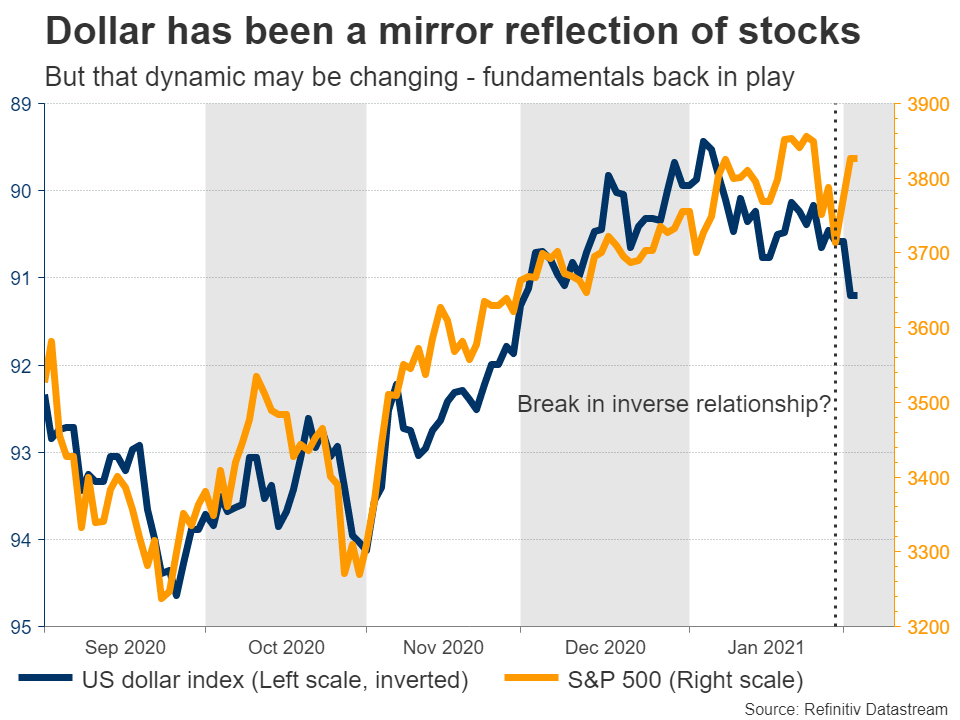

As for the dollar, it has been acting like a safe-haven throughout this crisis, but that dynamic seems to be changing lately, with the reserve currency becoming more aligned with US fundamentals. From a purely economic perspective, the outlook for euro/dollar in particular seems negative.

Most of Europe is still in a harsh lockdown, it has fallen far behind America in the vaccination race, its economy will almost certainly suffer a double-dip recession, and there isn’t any impressive stimulus coming either. There is hardly anything to be optimistic about in Europe, and the narrative of US economic outperformance could become the dominant FX driver going forward.

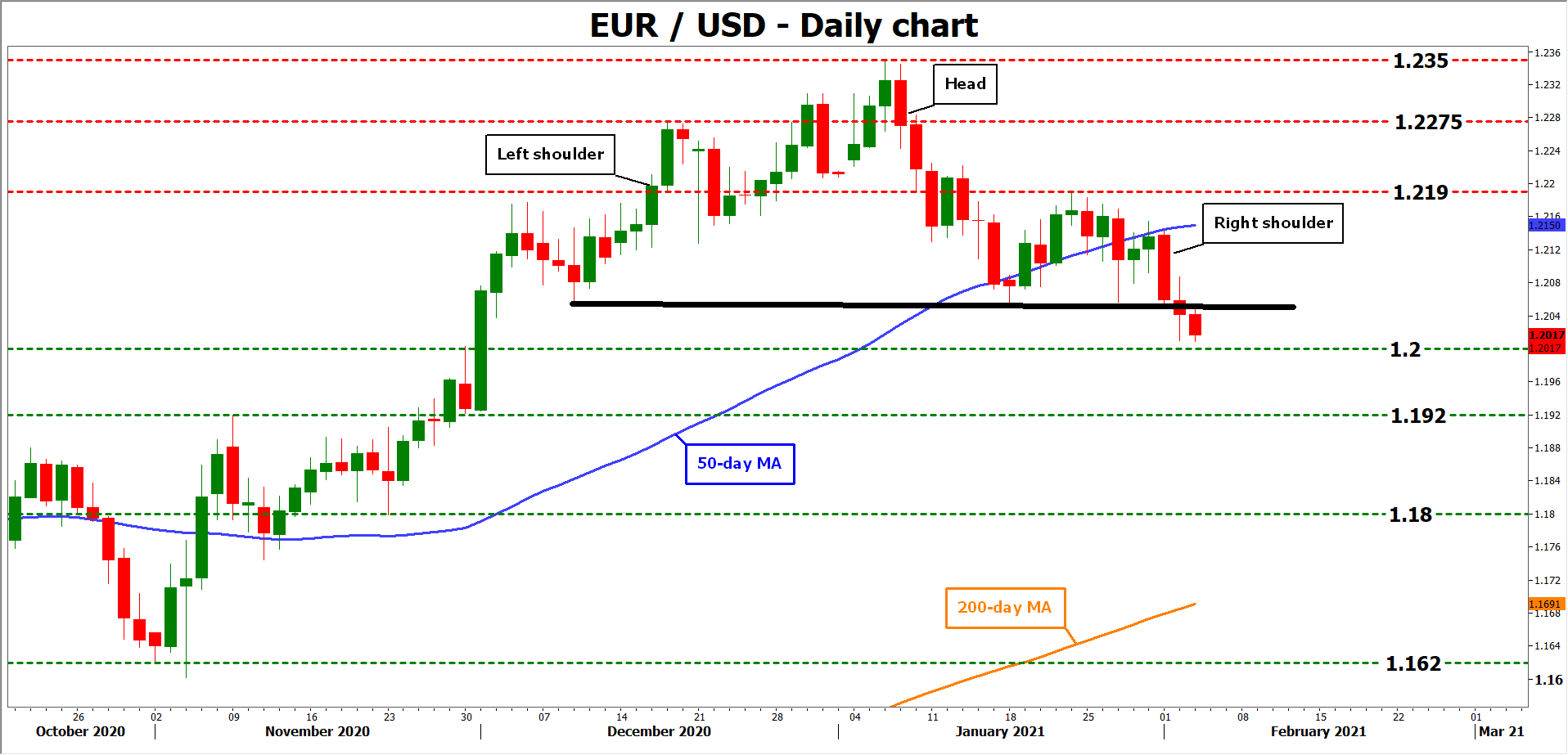

Euro/dollar’s technical picture points in the same direction. The pair recently completed a head-and-shoulders formation, which is typically a harbinger of more losses. A potential break below the psychological 1.2000 handle could bring the 1.1920 support zone into play next.

On the upside, a move back above the neckline of the formation around 1.2050 could see buyers challenge the 1.2190 region again.