{kind=link}

- Dollar approaches 2-month top as stimulus hopes push up yields, euro falters

- Stocks rise again as Wall Street rebounds, retail craze cools, silver plunges

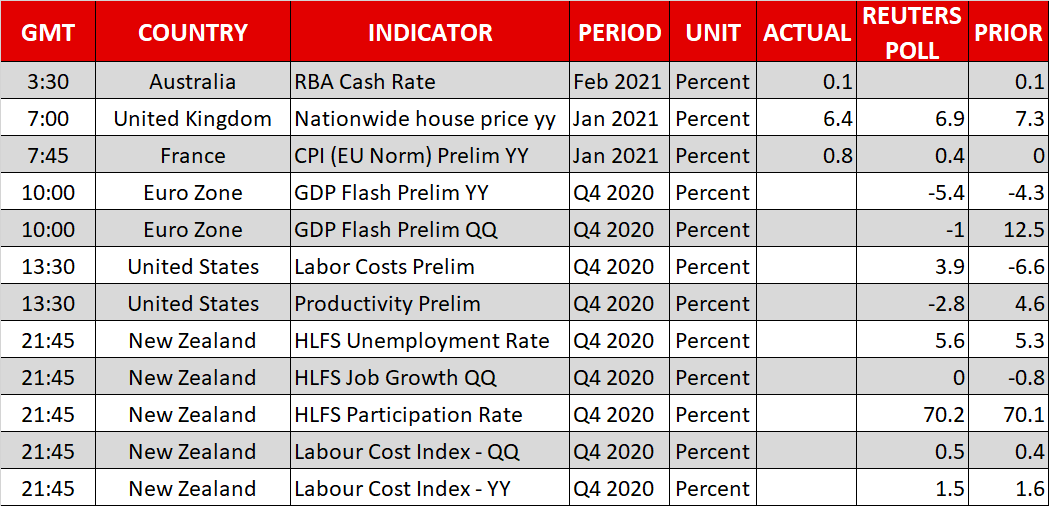

- Aussie bounces back, shrugs off surprise QE boost by RBA

A dollar comeback?

The US dollar appears to be on the rise again, mirroring a similar upward drive in 10-year Treasury yields in recent days. Expectations that the United States is moving closer to another big stimulus package lifted the greenback to near 2-month highs against a basket of currencies yesterday. At the same time, fears about new Covid strains and the patchy vaccine rollout in Europe and elsewhere are preserving a certain degree of risk aversion in the markets, supporting safe havens.

However, this time round, the gains do seem to be much more of a dollar story than anything else and dollar/yen’s breakout last week above its long-term downtrend line is testament to this. Hopes of more fiscal stimulus to come and rising inflation expectations are pushing up US yields, offsetting dovish talk by Fed officials.

A jump in the prices component of the ISM manufacturing PMI to a 10-year high in January was another reminder yesterday that the Fed may be downplaying the inflation risks during the recovery. However, it’s probably too soon to assume that the build-up of these price pressures is anything more than transitory, especially as the size of the next virus relief bill is yet to be determined.

Ten Republican Senators met up with President Biden at the White House on Monday to propose a $618 billion alternative to Democrats’ $1.9 trillion plan. However, unless the Republicans were to significantly up their offer, it’s more likely that the Democrats will bypass the GOP by using the process of budget reconciliation to get their oversized package through both chambers of Congress.

Equities in cheery mood again

The prospect of more fiscal stimulus in America and expectations that the Fed will ignore any temporary spikes in inflation are certainly good news for stock markets. But it’s not just the US benefiting from easy money as China’s central bank just injected liquidity into the money markets, cutting the rates on its 7- and 14-day reverse repos. The move was to counter the recent spike in China’s overnight repo rate, which had soared to a 5-year high on Friday.

The Reserve Bank of Australia also announced policy easing on Tuesday. Although rates were kept unchanged, the RBA surprised markets by expanding its asset purchases by another A$100 billion.

Most major indices in Asia closed higher by about 1% or more, while European shares also look set to post a second straight day of solid gains. US stock futures, meanwhile, were last up by about 0.8% after a strong session on Monday. The Nasdaq surged by 2.5% in anticipation of strong earnings results from the likes of Amazon and Google parent Alphabet. Both tech giants are due to report their results after today’s market close, but ahead of that, Exxon Mobil, Pfizer and Alibaba will announce their earnings before the opening bell.

The busy earnings week might help detract attention away from the ‘meme stocks’, whose rally appears to be losing steam. GameStop tumbled by 31.5% yesterday, though other Reddit favourites, such as Blackberry and Nokia continued to advance.

Outside of equities, retail investor’s newest target – silver – was also not having the best of times as it’s down more than 4% today, having briefly topped $30/oz on Monday. With the recent volatile action coming under increasing scrutiny from regulators and the online trading platform Robinhood facing backlash for its decision to limit trading in those Reddit stocks, it will be interesting to see whether the frenzy will flare up again or die down.

Aussie recovers from RBA punch, euro edges higher

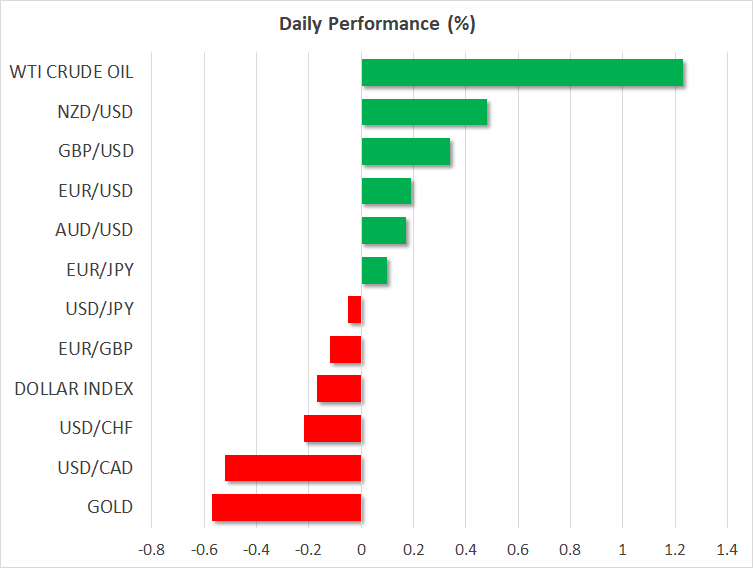

The Australian dollar managed to pick itself up following the RBA’s unexpected decision to boost its bond purchases, but the currency nevertheless lagged its peers. The New Zealand and Canadian dollars were the strongest performers, with the loonie being additionally lifted by higher oil prices.

The pound was another currency that sought to recoup yesterday’s losses, though it was struggling to reclaim the $1.37 level.

The euro has managed to find some support from better-than-expected Q4 GDP readings for the Eurozone. But persisting doubts about the EU’s ability to clean up its vaccine mess and the prospect of prolonged lockdowns continues to put a dampener on the currency. The euro was last trading marginally higher at $1.2065.