{kind=link}

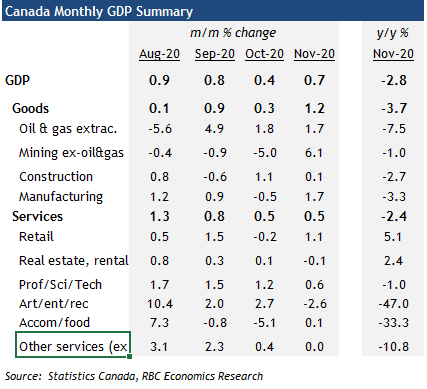

- Monthly GDP estimates surprised on the upside in November (+0.7% m/m) and December flash estimate (+0.3% m/m)

- Lockdowns still taking a toll on hospitality and travel services, but other sectors continuing to grow

- Near-term GDP tracking above prior assumptions, medium-term still highly reliant on vaccine rollout/effectiveness

The Canadian economy grew 0.7% in November and surprisingly posted another 0.3% gain in December according to Statistics Canada’s flash estimate. Those increases were despite escalating COVID-19 containment measures over that period.

The pace of improvement still slowed in December with containment measures reportedly starting to bite more significantly in the hard-hit accommodation & food services industry, as well as lower retail sales as restrictions on in-store sales at non-essential retailers ramped up.

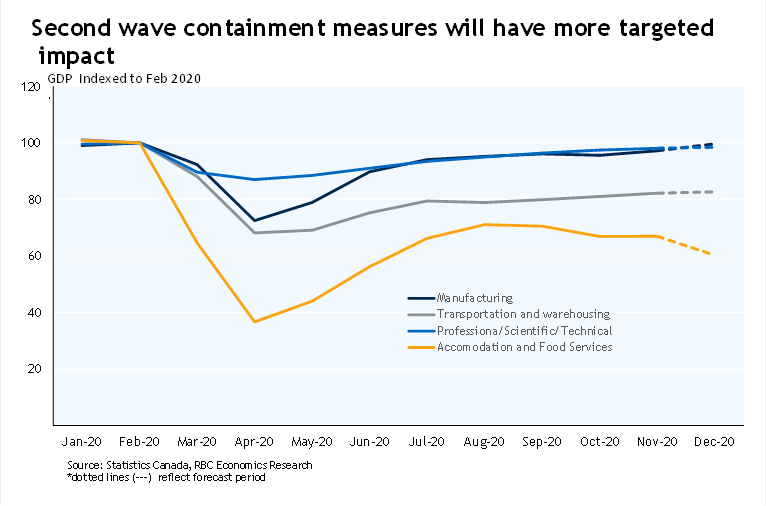

Lockdowns have been more targeted by industry through the second wave. The manufacturing sector has continued to recover as has activity in service-sector activity like professional services. Oil & gas output has been recovering. GDP was still down almost 3% from a year ago in November, but roughly half of that weakness comes from the accommodation & food services, recreation, and ‘other’ services sectors.

Virus containment measures likely bit more significantly on overall growth in January – but the Nov/Dec numbers clearly flag upside risk to our Q4 GDP growth forecast (closer to an 8% annualized GDP increase compared to RBC and BOC’s ~4 1/2% projections). And slowing virus spread means that January restrictions could begin to be gradually eased as early as February that may be enough to prevent a decline in overall GDP in Q1 as well. Beyond the very near-term, a more sustainable recovery in GDP back to ‘new normal’ levels still depends heavily on the rollout and effectiveness of vaccines.