{kind=link}

U.S. Highlights

- President Biden’s inauguration was the marque event this week. Previous market optimism on the stimulus potential of the new administration seemed to run out of steam at week’s end.

- The current administration has ambitious plans for further Covid-19 relief, but it remains uncertain what Congress will agree to. In our recent report, we outline some potential scenarios for upside risks to economic growth.

- The housing market hasn’t run out of steam, with starts activity rising to new heights. It will be clearer in the coming months if the pandemic’s race for space and low mortgage rates have kicked off the next leg up in the housing market.

Canadian Highlights

- Economic data released this week were a bit of a mixed bag. Manufacturing sales declined in November, while the gain in retail sales surprised on the upside.

- With the virus still spreading rapidly and restrictions mounting, the near-term outlook looks bleak. Accordingly, the Bank of Canada left the policy rate at 0.25% and continued the QE program at its current pace.

- Given positive vaccine developments and fiscal stimulus, the Bank upgraded its medium-term outlook. Despite this, it reiterated that it will keep the overnight rate at the effective lower bound until into 2023.

U.S. – Biden’s Stimulus Would Boost Growth

President Biden’s inauguration was the marque event this week. Since the Georgia Senate run-off elections gave the Democrats a razor thin majority in Congress, equity markets have cheered the changeover in power. However, towards week end, sentiment soured a bit, perhaps as investors question how far the rally has gone.

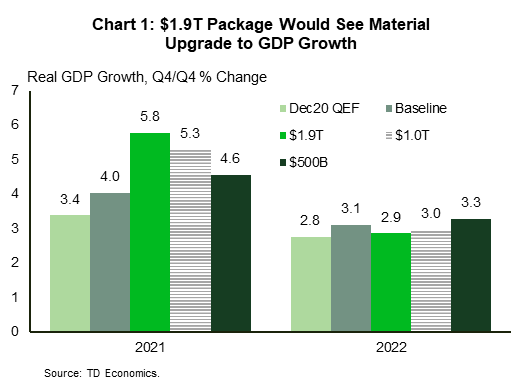

Equity markets had been pricing in greater optimism on the American economy, hopeful that Democratic control in Congress would mean more fiscal stimulus and a faster recovery. However, it is still too early to determine what size of package will get through Congress. In a recent report we looked at three different scenarios for the next round of Covid-19 relief ranging from $500 billion to $1.9 trillion, and estimate the potential growth responses of each. The range of forecasts is shown in Chart 1.

These scenarios do not include a larger plan that the administration could pursue later in the year encompassing spending on campaign commitments such as infrastructure, and health and education, funded by higher taxes. These could have further implications on medium-term growth, particularly infrastructure spending, which has been shown to have some of the highest growth multipliers, particularly when the economy is weak.

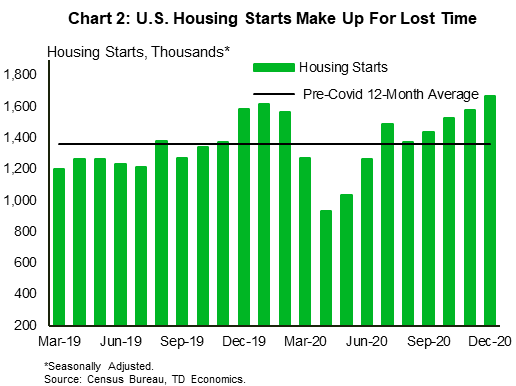

The area of the economy that has rebounded most strongly from the pandemic-driven weakness in the spring is the housing market. Housing starts beat expectations in December, rising 5.8% to 1.67 million units (annualized), the highest level in 14 years. Once again, single family starts led the way, as demand for space has intensified since the pandemic, and inventory in the resale market remains drum-tight.

It is uncertain how long the current pace of construction can be sustained. In the 12 months prior to the pandemic, housing starts averaged 1.36 million. In the March through June period they ran well below that level, creating a backlog of pent-up demand. Since then, housing starts have been mainly above this trend, but have not quite yet made up for the ground lost in the spring. Once the backlog has been made up, we would expect starts to move toward their previous trend level.

Still, it is also possible that rock-bottom interest rates, increased confidence among homebuilders, and price pressures in the resale market will lead to a higher level of construction than we had anticipated pre-pandemic. The demographic fundamentals are certainly a positive factor as the largest segment of millennials is 25-29 years old, just starting to enter the peak phase of household formation. The next few months will be key to see if the construction industry can keep up the current pace.

Thankfully, infections have been trending down. The pace of the vaccine rollout has fallen short of the initial goal, but the country is doing well relative to its advanced economy peers. Regardless of what is achieved in terms of further stimulus from Congress, we expect the U.S. economy will see a much faster pace of growth come the second quarter, as people are able to resume more of their pre-pandemic behaviors.

Canada – Near Term Weakness, Medium Term Strength

It was a blur of a week, with multiple data releases, a Bank of Canada interest rate decision, and of course, a presidential inauguration south of the border. The S&P/TSX composite index took much of this in stride, rising for most of week until Thursday, when it saw a sizeable drop due to weakness in the technology sector. This was followed by a further slide on Friday, leaving the index -0.4% below close last week at the time of writing.

Turning to the string of economic data released this week, it was a mixed bag. Manufacturing sales declined for the second straight month, falling 0.6% on the month in November. The details were better than the headline. Contractions were limited to only five of the 21 industries. Meanwhile, retail sales rose at their fastest pace since September, climbing 1.3% in November. The increase was driven by gains in food and beverage and online purchases; the latter benefitting from Black Friday sales. However, with the virus still spreading quickly, and some provinces enforcing tougher restrictions, future data points are likely to take a turn for the worse. Indeed, Statistics Canada estimates retail sales declined 2.6% in December.

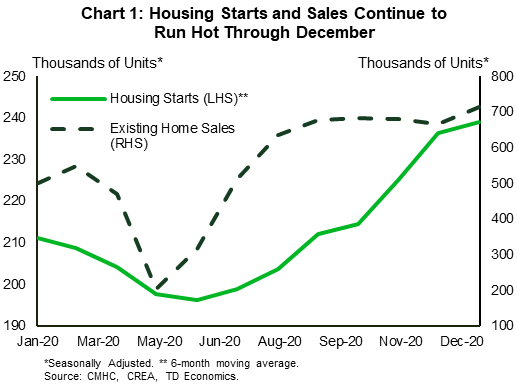

The near-term outlook isn’t gloomy for all areas of the economy. The housing market has shown spectacular strength through the pandemic and December was no different. Last week’s extraordinary sales data were followed by housing starts figures that remained elevated at 228.3k units (Chart 1). This level could have been even higher if surveying issues hadn’t resulted in the Kelowna CMA being excluded from the data last month. Looking ahead, Ontario has imposed new restrictions on non-essential construction, but they do not apply to residential projects for which permits have already been granted. Given that issuance has been solid recently, home construction could see little slowing this month.

The Bank of Canada considered this strength, as well as the broader slowing of the economy in its monetary policy decision this week. Judging the economy still required extraordinary support, the Bank opted to leave the overnight rate unchanged at 0.25% and keep the quantitative easing program running at its current pace of (at least) $4 billion per week. In addition, the Bank said that it will hold the policy rate at the effective lower bound until 2023.

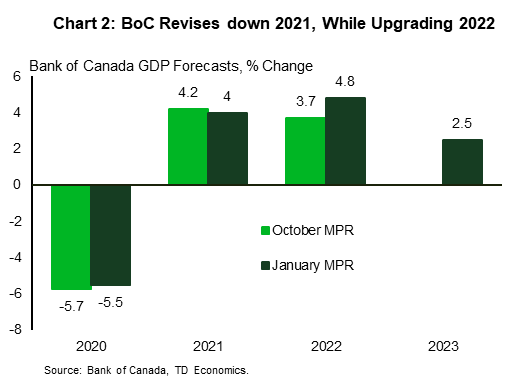

The Bank’s commitment to not hiking rates came even as it upgraded its medium-term outlook. While the 2021 forecast was lowered a touch due to near term challenges, the 2022 projection was revised up by 1.1 percentage points to 4.8% owing mainly to the earlier-than-expected availability of vaccines and fiscal supports (Chart 2). The Bank also introduced the 2023 forecast, which stood at 2.5%.

Notably, the projection also assumed consumers will not spend the additional savings they had accumulated so far through the pandemic. By our estimates, these “excess savings” could amount to around $150 billion (6.4% of GDP). If deployed, it could generate inflationary pressures sooner and force rate hikes before 2023. Expect the Bank to watch these trends closely in the coming quarters.

U.S: Upcoming Key Economic Releases

U.S. FOMC Meeting – January

Release Date: January 27

Previous: 0.25%

TD Forecast: 0.25%

Consensus: 0.25%

Changes to the FOMC statement are likely to be fairly minor, consistent with no plans for policy changes anytime soon. The chairman will likely remain dovish on the policy outlook in his press conference even as he expresses some optimism about growth in the year ahead—with vaccines and fiscal stimulus ultimately contributing to strength. Inflation will be key to tapering as well as tightening, and most officials appear to be skeptical that a few strong quarters for growth will suddenly lead to a sustained pickup in the trend.

U.S. Real GDP – Q4 Advanced

Release Date: January 28

Previous: 33.4%

TD Forecast: 3.0%

Consensus: 4.4%

Real GDP appears to have slowed in Q4, potentially to the point of contraction as the quarter ended, but it was likely up moderately in Q4 as a whole; we estimate a 3% q/q AR, down from 33.4% in Q3. Most components likely slowed; we estimate a 2.5% pace for real consumption, down from 41.0% in Q3. Inflation likely remained well below the Fed’s 2% goal; our 1.3% q/q AR estimate for core PCE prices implies 1.4% y/y (unchanged from the pace in Q3).

U.S. Personal Income & Spending – December

Release Date: January 29

Previous: Spending: -0.4% m/m; Income: -1.1% m/m

TD Forecast: Spending: -0.7% m/m; Income: 0.2% m/m

Consensus: Spending: -0.5% m/m; Income: 0.2% m/m

Consumer spending likely fell in December, similar to the pattern already reported for the less comprehensive retail sales series. The weakening probably reflects the impact of new COVID restrictions as well as relatively weak holiday-related spending. Income appears to have risen modestly, however, with wage income up even though payrolls fell. PCE prices probably picked up on a m/m basis, led by the energy component but with a fairly solid gain at the core level as well. The 12-month change in core prices probably remained at 1.4%, which is down from 1.9% in February (pre-COVID).

Canada: Upcoming Key Economic Releases

Canadian GDP – November

Release Date: January 29

Previous: 0.4%

TD Forecast: 0.5%

Consensus: NA

Industry-level GDP is forecast to rise by 0.5% m/m in November, slightly above flash estimates for 0.4%, in what could be the last month of positive growth before new COVID measures tip the economy back into contraction. We look for November’s growth to be led by the goods-producing sector with a solid tailwind from energy and construction. November crude production rose into positive territory on a year-ago basis for the first time since March 2020, and November housing starts were among the strongest on record. Services should see more modest gains, with a solid performance in retail/wholesale trade offset by headwinds to accommodation/food services and other components affected by public health measures. Flash estimates for December will be included with the release and could receive nearly as much attention as the November results; COVID restrictions became more intense into year-end but the relatively modest decline in hours worked (-0.3%) for December, and composition of jobs lost, suggest any contraction should be far smaller than those observed last spring.