{kind=link}

The USD tended to be on the rise during today’s Asian session against a number of its counterparts as US yields rose over the past few days. The hesitation of the Fed to expand its borrowings, seems to be one of the reasons for the rise of the US yields, while the recent comments of the Fed’s Vice Chair Clarida that the Fed is not abound to change its $120 billion purchases of debt per week, as reported by Reuters, were characteristic of the Fed’s attitude. At the same time some political uncertainty seems to be underway in the US given that the momentum to impeach Trump for a second time seems to be growing in the US House of Representatives, yet such a scenario could be in the more distant future. Nevertheless, some safe haven inflows for the USD, may continue to be observed, stemming from the political uncertainty in the US, given its current liquidity. At the same time, it should be noted that expectations for another substantial stimulus are still ongoing and President elect Biden could announce such plans. Should the risk off mood of the market continue to dictate its direction, we may see the USD continuing to strengthen, while US stock markets could weaken.

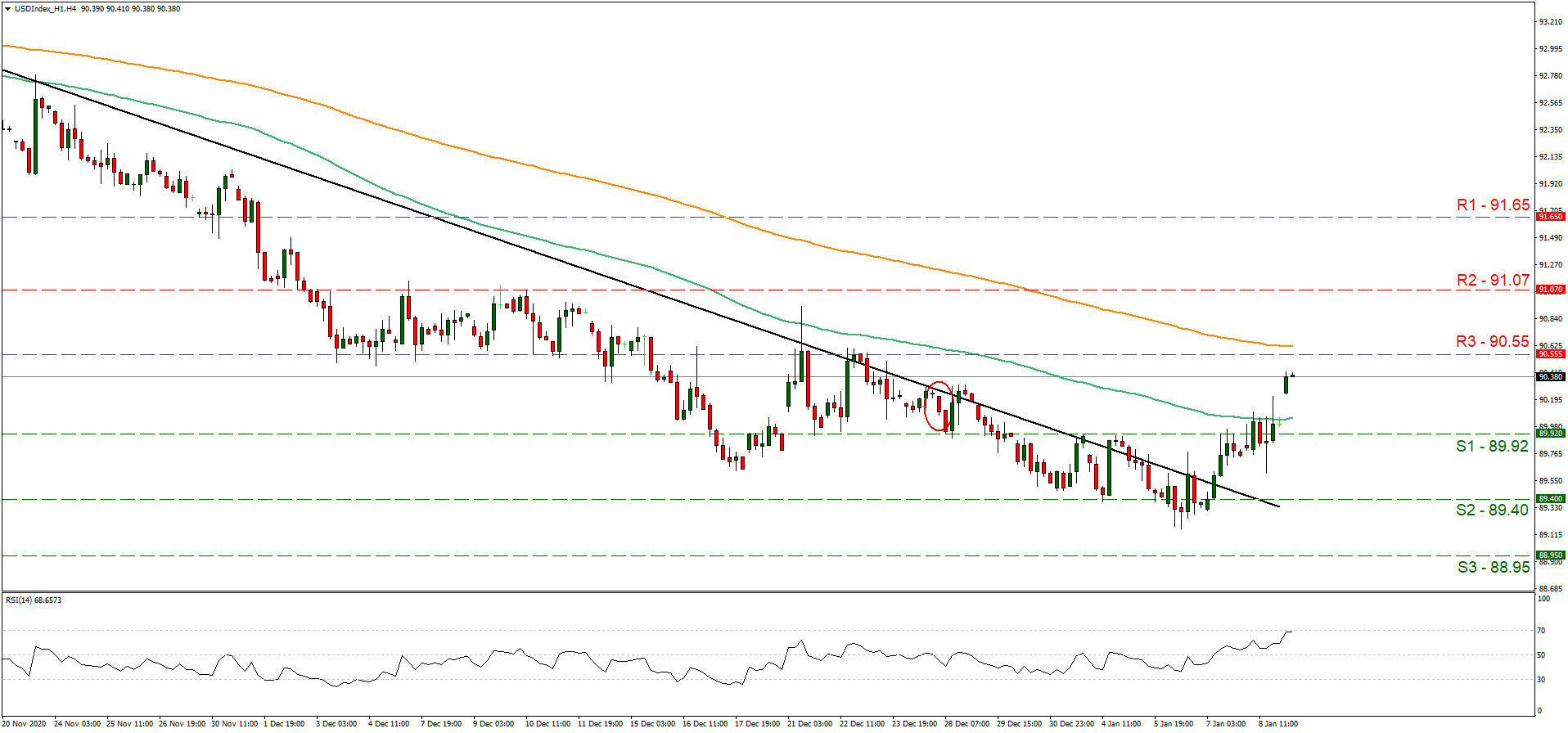

The USD Index opened with a positive gap this morning aiming for the 90.55 (R1) resistance line. A correction lower could be in the cards for the index given the sudden rise, yet today’s fundamentals could alter the indexes’ direction. Please note that the RSI indicator below our 4-hour chart, has reached the reading of 70 confirming the presence of the bulls on the one hand, yet on the other may imply that the instrument’s long positions may be somewhat overcrowded. If there is further demand for the USD, we could see the USD Index breaking the 90.55 (R1) resistance line and start aiming for the 91.07 (R2) resistance level. If a selling interest is displayed, we could see the index breaking the 89.92 (S1) line, aiming for the 89.40 (S2) level

Oil prices retreat on Covid 19 worries

WTI prices were on the retreat during today’s Asian session as increased Covid 19 cases in China and the US seemed to worry oil traders. Mainland China’s number of daily infections were the highest for a number of months, with the epicenter being reported to be in the Hebei province and tend to create some worries for slowdown of economic activity which in turn may reduce oil consumption for the economic giant. Also, despite the vaccination being ongoing in the US and Europe, the high number of cases and the strict lockdowns seem to worry traders as well, creating an adverse effect on oil prices. Covid 19 worries seem to currently overshadow the support oil prices got from Saudi Arabia’s decision to reduce production and should they intensify we may see oil prices retreating further.

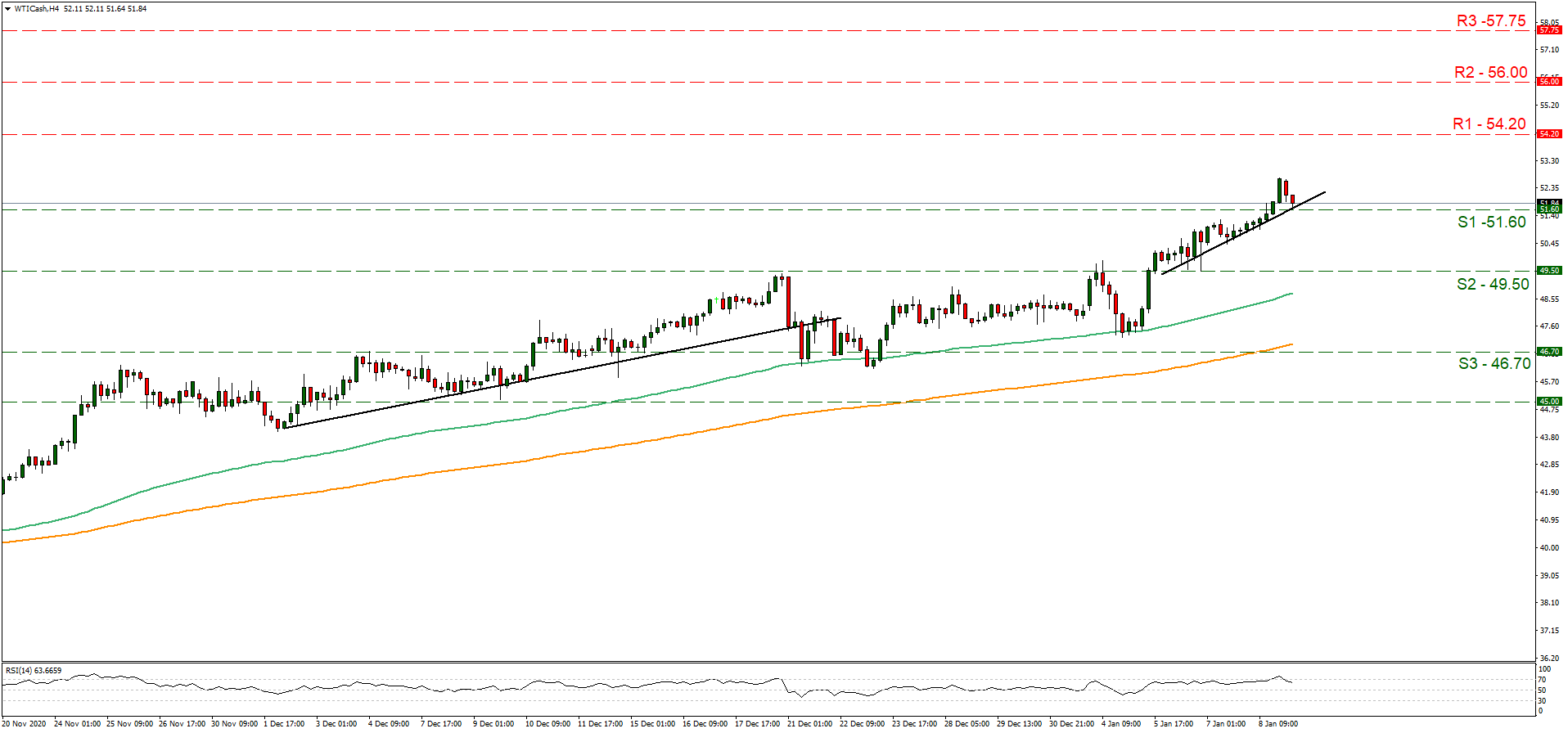

WTI prices declined somewhat during today’s Asian session, aiming for the 51.60 (S1) support level. Despite the drop we maintain a bullish outlook and for it to change in favour of a sideways motion initially, we would require a clear breaking of the upward trendline incepted since the 6th of the month. Should the bears maintain control over the commodity’s prices, we could see it breaking the 51.60 (S1) support line and aim for the 49.50 (S2) level. Should the bulls regain control, we could see it breaking the for the 54.20 (R1) resistance line and aim for the 56.00 (R2) resistance hurdle.

Other economic highlights today and early Tuesday:

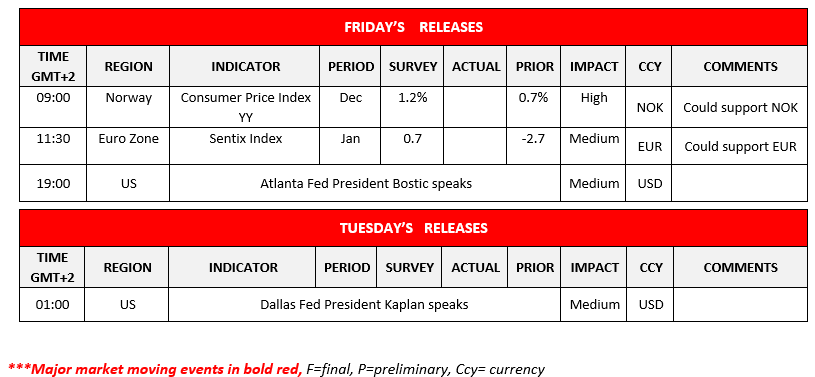

Today during the European session, we note Norway’s CPI rates for December as Eurozone’s Sentix index for January. As for speakers please note that Atlanta Fed President Bostic and Dallas Fed President Kaplan speak.

As for the rest of the week

No major financial releases are expected on Tuesday while on Wednesday, we get Eurozone’s industrial production growth rate for November and the US inflation measures for December. On Thursday, we get Japan’s corporate goods prices for December and machinery orders growth rate for November, while from China the trade data for December, from Germany the GDP rate for 2020, and from the US the weekly initial jobless claims figure, while Fed’s Chairman Jerome Powell speaks. On Friday, we highlight UK’s GDP rates for November, and note from France December’s final CPI (EU Normalised) rate while form the US we get the industrial production growth rate for December and the preliminary University of Michigan consumer sentiment indicator.

USD Index H4 Chart

Support: 89.92 (S1), 89.40 (S2), 88.95 (S3)

Resistance: 90.55 (R1), 89.40 (R2), 88.95 (R3)

WTI H4 Chart

Support: 51.60 (S1), 49.50 (S2), 46.70 (S3)

Resistance: 54.20 (R1), 56.00 (R2), 57.75 (R3)