U.S. Highlights

- Prospects for fiscal stimulus drove volatility in equity markets this week. Policymakers are reportedly closing in on a much-needed relief package following several months of gridlock.

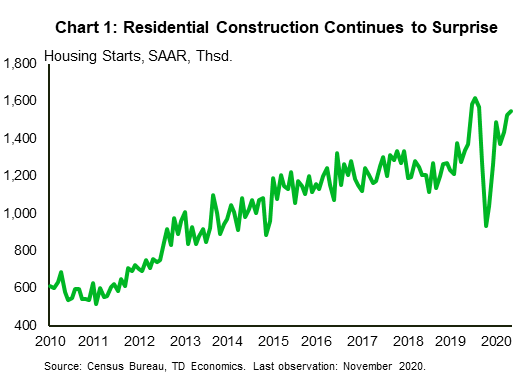

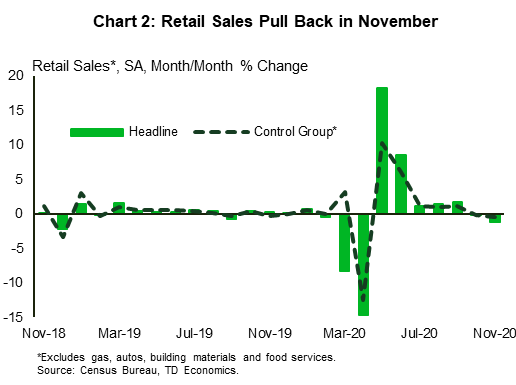

- Economic data released this week were less cheerful. Jobless claims rose to levels last seen in early September, while retail sales declined by 1.1% in November. Housing starts were the exception, increasing by 1.2% last month.

- The Fed reaffirmed its pledge to support the economy. It maintained its current policy stance this week, keeping the fed funds rate near zero and committing to more asset purchases.

Canadian Highlights

- Markets were mixed this week as news of vaccine rollouts competed with on-again-off-again stimulus talks.

- Domestically, virus case counts remain elevated, prompting a new round of restrictions (or talks thereof) in some provinces. Data releases – manufacturing, retail sales – continued to paint a picture of softening economic momentum. That said, housing markets continued to surprise on the upside.

- Bank of Canada Governor Tiff Macklem delivered his final speech of 2020. The speech did not include policy guidance. Instead, it highlighted the role of exports in Canada’s recovery.

U.S. – Holiday Shopping Blues

It was a busy week for economic data. Financial markets, however, devoted their attention to the brightening prospects for a new stimulus bill. Indeed, following several months of gridlock, this week saw considerable progress on that front. News broke that lawmakers are racing to finalize a deal before next week’s recess, which helped lift market sentiment. At the time of writing, the S&P 500 was on track to end the week 1% higher.

By contrast, economic data released this week was decidedly less cheerful. Outside of a positive surprise coming from housing starts, the data continued to paint the picture of a faltering recovery. As discussed in our Quarterly Economic Forecast, a slowdown has been expected, given the surge in new coronavirus cases and the growing number of restrictions being implemented across the country. On the bright side, rollouts have officially begun for Pfizer’s vaccine. Meanwhile, Moderna’s is expected to receive approval very soon and could be made available as early as this weekend.

Back to the data, the strength in residential construction continues to impress. Housing starts rose by 1.2% in November, their seventh consecutive month of increases (Chart 1). Overall, starts have now rebounded within 1.3% of their healthy February-level. Unlike previous months, multi-family starts powered the gains last month, jumping 4% from October. As we discuss in a recent report, this segment of the market continues to face challenges due to shifting housing preferences toward bigger homes and more outdoor space. Nonetheless, single-family starts saw a more muted increase last month (+0.4%).

Despite its resilience, the construction sector’s outlook is softened by deteriorating affordability. In fact, construction costs have risen at the same time as inventories remained low. These factors could weigh on housing demand in 2021.

Less encouraging was the continued rise in initial jobless claims, suggesting that layoffs are picking up. Claims, which increased to 885,000 last week, were at their highest since early September. The November retail sales report was similarly disappointing. Sales fell by 1.1% last month (Chart 2), following a downwardly revised October reading (-0.1%).

By all accounts, the third wave of COVID-19 infections is weighing on this year’s holiday shopping season. Sales declined the most at clothing stores, alongside food services and drinking places which are most susceptible to be impacted by restrictions. By contrast, food and beverage stores, as well as building material retailers recorded positive sales growth last month.

The fragility of the economic recovery was acknowledged during this week’s Federal Reserve Open Market Committee (FOMC) policy announcement. Members unanimously voted to maintain the current policy stance, keeping the fed funds rate at its effective lower bound and committing to more asset purchases. The Fed reaffirmed its pledge to use the full array of policy tools at its disposal to support the economy until the recovery is complete. The missing piece of the puzzle is additional fiscal support. But, with that likely on the way, coupled with vaccines, the light at the end of the tunnel is finally looking a little brighter.

Canada – Second Waves Dampen Near-Term Growth

Financial markets were mixed this week as optimism on vaccine rollouts competed with news of on-again-off-again U.S. fiscal stimulus talks. The S&P/TSX Composite was almost flat on the week (+0.4% as of writing). Meanwhile, commodity prices continued to advance on vaccine developments, surging Chinese demand, and tightening inventories. Namely, WTI oil prices were up 4.7% to US$48.8/barrel, while copper prices surged past $3.6/lb. – their highest since 2013, at the time of writing.

As noted in our recently-released Quarterly Economic Forecast, vaccine developments have lifted the medium-term outlook for Canada and the global economy. However, this improvement is preceded by near-term uncertainties relating to surging virus case counts. This week’s negative news flow in Canada corroborates this narrative. Early excitement of vaccine rollouts were tempered by sharply rising case counts in Ontario and still-elevated case counts elsewhere. This has prompted a new round of restrictions (or talks thereof) across several provinces.

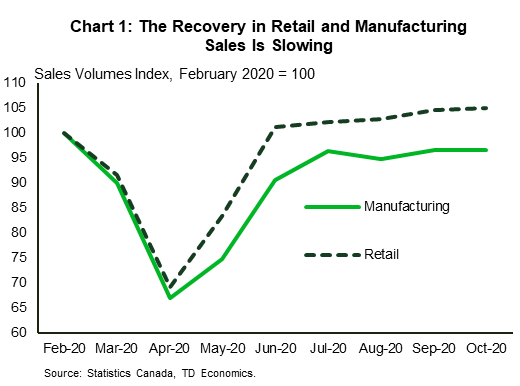

On the data front, we continue to receive evidence of weakening economic momentum. October’s manufacturing shipments surprised to the downside, increasing by a modest 0.3%. Worse, volumes were flat on the month (Chart 1). Retail sales were better than expected, rising 0.4%, though with a less encouraging (0.2%) uptick in volumes. It bears noting that this week’s releases are backward-looking and do not fully capture the impacts of new restrictions. Indeed, Statistics Canada’s preliminary estimates point to a flat performance for retail sales in November. Moreover, higher frequency indicators, including mobility data, TD spending data, and restaurant reservations all point to a further loss in momentum in the past two months.

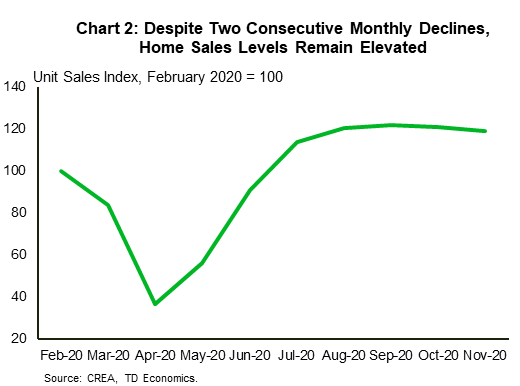

Still, some parts of the economy – namely the housing market — continue to defy gravity. Housing starts soared to 246K in November. Existing home sales pulled back for the second consecutive month but remain elevated relative to year-ago levels (Chart 2). Looking ahead, we expect housing activity to slow, in line with historical trends.

Statistics Canada also released Q3 population estimates this week. The data showed population growth pulling back to its slowest pace since comparable data collection began in 1946. It goes without saying that the culprit here is international immigration – which tumbled on virus-related travel disruptions.

On a separate note, Bank of Canada Governor Tiff Macklem delivered his final speech of 2020. The speech did not offer guidance on policy. For this, we can turn to last week’s speech (see note) from Deputy Governor Beaudry and still-subdued inflation readings (November’s headline CPI inflation came in at 1% this week). Instead, the speech highlighted the importance of competitiveness, diversifying Canada’s exports and trading partners, and the crucial role trade will play in lifting Canada’s economy from its sizeable contraction. Indeed, as the focus shifts away from near term-setbacks, an economic rotation to exports and business investment will be critical in eliminating lingering economic slack.

U.S: Upcoming Key Economic Releases

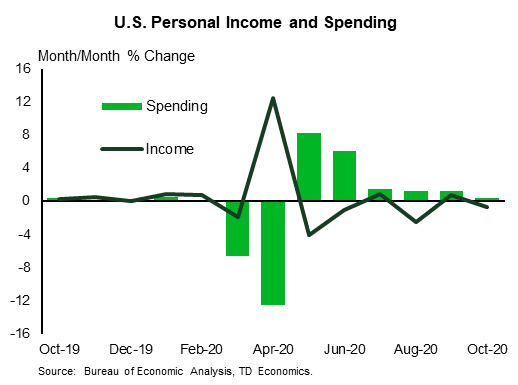

U.S. Personal Income and Spending- November

- Release Date: December 23rd, 2020

- Previous: PCE deflator: 0.0% m/m, 1.2% y/y; core PCE deflator: 0.0% m/m, 1.4% y/y; personal spending: 0.5% m/m; personal income: -0.7% m/m

- TD Forecast: PCE deflator: 0.0% m/m, 1.1% y/y; core PCE deflator: 0.0% m/m, 1.4% y/y; personal spending: -0.4% m/m; personal income: -0.8% m/m

- Consensus: PCE deflator: 0.1% m/m, 1.2% y/y; core PCE deflator: 0.1% m/m, 1.4% y/y; personal spending: -0.2% m/m; personal income: -0.2% m/m

Consumer spending likely fell in November, similar to the pattern already reported for the less comprehensive retail sales series. Income likely fell even more, dragged down by a fading of the boost from fiscal stimulus (particularly the Payroll Protection Program, the benefits of which were spread over six months in the data). We expect the inflation parts of the report to be weak as well, with total and core PCE prices both 0.0% m/m and up just 1.1% and 1.4%, respectively, y/y. Core PCE inflation is down from 1.9% y/y in February (pre-COVID).

Canada: Upcoming Key Economic Releases

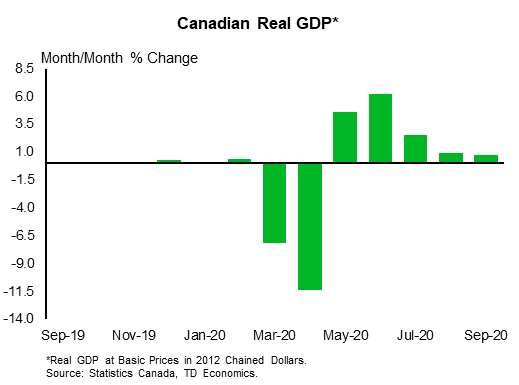

Canadian Monthly GDP – October

- Release Date: December 23rd, 2020

- Previous: 0.8%

- TD Forecast: 0.5%

- Consensus: NA

Industry-level GDP growth is forecast to slow to 0.5% m/m in October as momentum continues to fade from the strong Q3 rebound. Energy will provide a tailwind to the goods-producing sector on higher oil sands output that should help make up for a lackluster performance in manufacturing, while construction should also make a positive contribution. Looking to services, real estate will benefit from resale transactions that were just shy of record levels while wholesale trade provides another source of strength. A 0.5% print would leave output just 4.2% below year-ago levels and mark the fifth time that GDP growth has outperformed flash estimates (0.2% for Oct) over the last six months.

{kind=link}