{kind=link}

- ECB decision the main event today, can policymakers over-deliver?

- Stock markets retreat from record highs as US stimulus talks stall

- Pound drops after top-level Brexit meeting yields no breakthrough

- Gold under pressure too, yet aussie dollar defies cautious mood

ECB preview: Sinking the euro won’t be easy

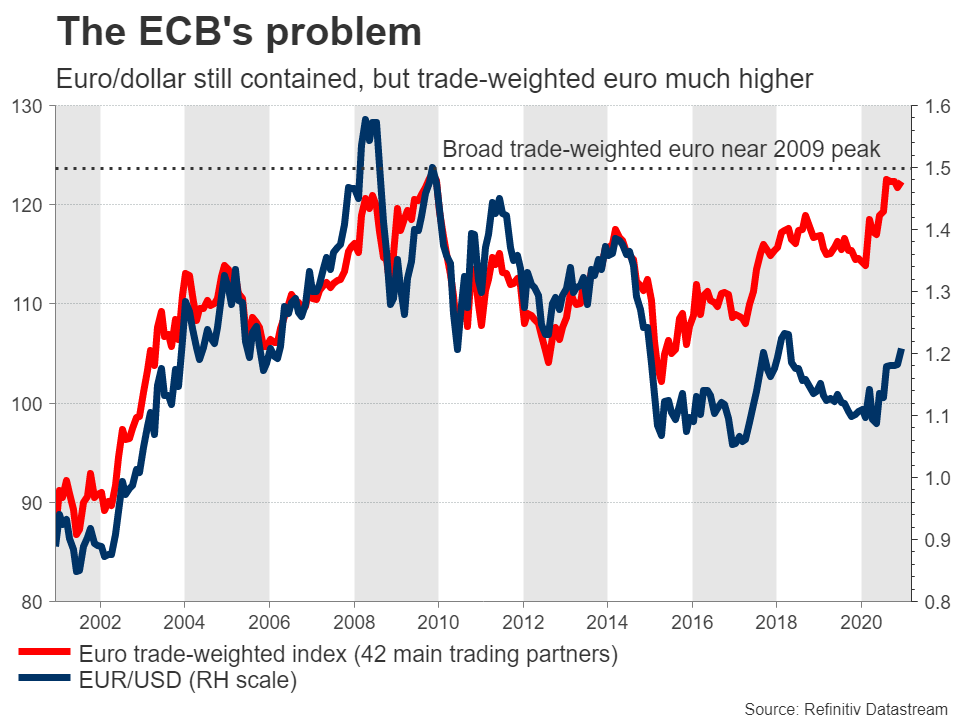

The spotlight will fall on the European Central Bank today, which is widely expected to deliver another easing package of around €500bn, likely complemented by more ultra-generous loans to banks. The bad news for the ECB is that this package has already been well telegraphed and priced in, and yet the trade-weighted euro has continued to race higher.

A stronger currency can dampen growth and inflation, and with the Eurozone economy already battling deflation, an even stronger euro could be a real headache. Hence, the ECB ideally wants to deliver something over and above what investors expect, to clip the euro’s wings. Perhaps a QE package closer to €1 trillion or a rate cut could do the trick.

But can it? Several of the ‘hawks’ may not be willing to go all-out. They argue that with interest rates already negative, the benefits of massive QE here are minimal, and doing too much could encourage excessive speculation. What’s more, when the ECB pre-committed to this package, vaccines had not been announced yet. Those news minimize the longer-term risks and may diminish the appetite for ultra-aggressive action.

The bottom line is that markets may be left disappointed by the size of this package. If so, that would argue for a positive reaction in the euro. There is the prospect that President Lagarde tries to ‘talk down’ the currency during her press conference, but that only works if investors believe there is a credible threat of action to back it up. Just saying you want a weaker euro doesn’t work for long, and the ECB already played this card back in September.

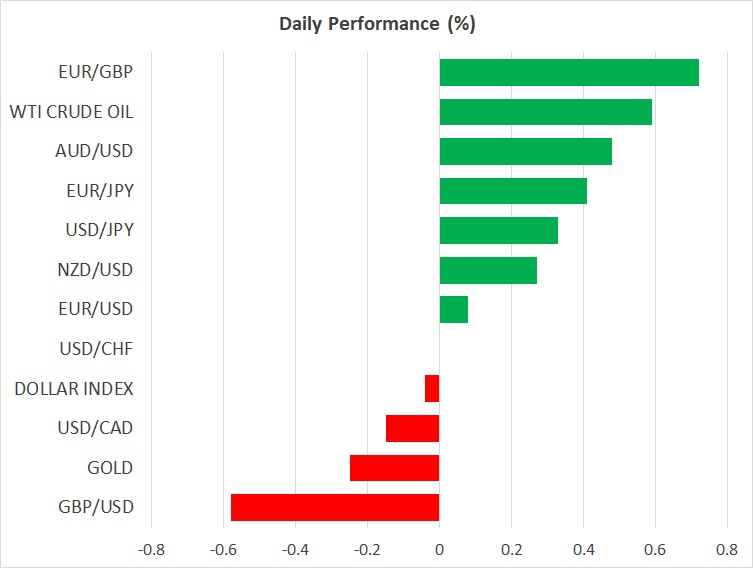

Stocks tumble, US stimulus nerves to blame?

Risk aversion made a rare appearance on Wednesday, with tech shares leading the US equity markets lower. There was no clear catalyst behind this selloff, though the absence of a breakthrough in the US stimulus talks may have given investors an excuse to take some profits at elevated levels.

That said, the setback wasn’t dramatic. The S&P 500 fell back to where it was trading last Friday, whereas the heavier-hit Nasdaq is now merely flat on the month. This suggests the broader narrative has not changed. Vaccines are still on the horizon and more stimulus is still on the menu, even if there is more political theater until we get there.

Another victim of this selloff was gold, which fell back below the crucial $1850 region despite real US yields edging lower. The short-term correlation between real yields and bullion is exceptionally weak at this stage, but if historical patterns hold, that is unlikely to last long.

The yellow metal was pressured by a revival in the US dollar, which has staged a comeback under the radar this week, bolstered by the cautious mood and the absence of progress in the Brexit talks that is keeping the pound and euro on a leash.

Boris eats ‘cold fish’ in Brussels

The dinner between the UK Prime Minister and the EU Commission chief yielded no breakthrough in the Brexit saga yesterday. The two sides agreed to continue negotiating until the end of the week, even though they “remain far apart”.

The pound fell but was not totally annihilated, so investors remain fairly optimistic that a deal is still within reach. Both sides have too much to lose, and Boris Johnson is notorious for taking negotiations to their absolute breaking point before conceding.

There is an EU Council meeting taking place today, though Brexit is not officially on the agenda.

Finally, the aussie miraculously defied the cautious mood to reach new multi-year highs, boosted by soaring iron ore prices and an almost virus-free Australian economy.