{kind=link}

- Investors revert to old pandemic playbook amid new US restrictions

- Nasdaq hits new highs, but other stock indices drop alongside oil

- Gold stages heroic comeback, bigger picture still encouraging

- Sterling on the back foot as PM Johnson heads to Brussels

Big tech shines as pandemic concerns resurface

A sense of caution has crept back into global markets, as investors try to balance the prospect of more government stimulus and central bank liquidity against the grim pandemic reality, with California announcing new business restrictions yesterday. California is America’s most populous state and its biggest economy, so this could have dire implications for the entire nation’s recovery.

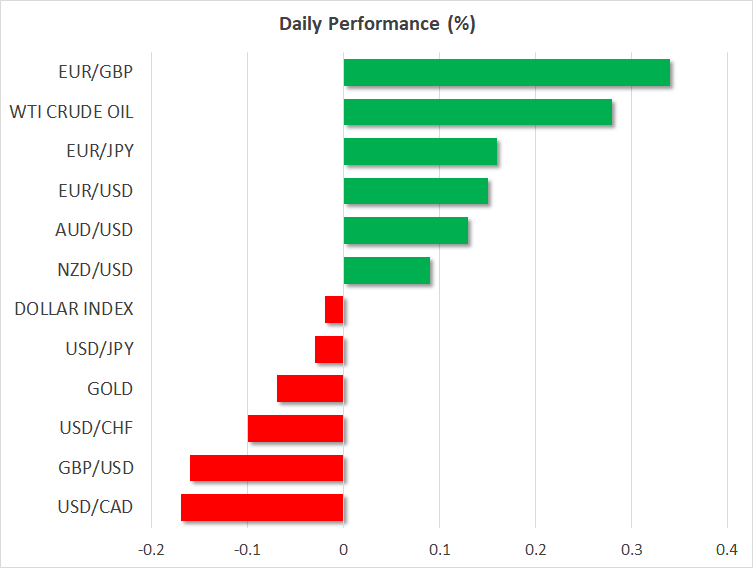

Faced with the risk of a dark winter for economic activity, investors reverted to their old pandemic playbook: buy mega-cap tech stories that are almost immune to shutdowns and hedge some risk by piling into havens like gold and bonds. The prospect of the Brexit talks collapsing also weighed.

Now to be clear, there wasn’t any massive selloff. Most stock indices are still near record highs and the defensive dollar remains near its recent lows, so there is no sense of panic either. Investors know that no matter how bad the winter gets, the endgame is still a post-vaccine world, and another tsunami of stimulus and liquidity is in the pipeline to keep things glued together in the meantime.

Is the ocean of liquidity masking the risks?

The risk is that markets are too complacent. Most measures of market sentiment like call/put ratios are flashing extreme greed and short interest is near record lows, so the bears have thrown in the towel and the ship is being steered solely by the bulls here. And as the Bank for International Settlements warned yesterday, there is still a real risk of a wave of bankruptcies, as loans are not a solution for insolvency.

There are several other risks too, like a spike in unemployment once all the support measures expire or a real acceleration in inflation next year that backs the Fed into a corner. That said, these are discussions for another day. For now, the main variables for the currency and equity markets are how much liquidity the ECB and Fed will unleash in the coming days, how big the new US relief package will be, and how the Brexit saga concludes.

Gold back in the ring to take another swing

Bullion staged a heroic comeback in recent days to cross back above the crucial $1850 zone, capitalizing on a combination of falling real interest rates and a softer US dollar. The revival of the US stimulus talks has seen both inflation expectations and Treasury yields racing higher, but inflation expectations have risen faster than yields, pushing real rates down.

It is not just the stimulus talks of course. Inflation bets have picked up lately as house prices are booming, industrial commodities like copper and crude oil are surging, and savings rates have risen dramatically. All that pent-up demand could really show up in consumer prices once everything reopens, and the Fed is unlikely to take its foot off the gas.

Looking ahead, the outlook for gold still seems favorable. Loose money policies and enormous public deficits are likely here to stay, inflation may be in the pipeline to push real rates even lower, and the consensus on the Street is overwhelmingly for a weaker dollar next year.

Pound retreats, Boris heads to Brussels

The British pound remains on the back foot as fears of a breakdown in the Brexit talks have resurfaced. The latest update is that Prime Minister Johnson will head to Brussels tomorrow to meet EU Commission chief von der Leyen, in a last-ditch attempt to break the impasse.

Neither side can afford a no-deal exit, so a resolution or another extension still seem more likely, even if it goes down to the wire. That said, the pound is having its doubts, and the currency will likely remain a hostage to incoming headlines for now.