{kind=link}

The greenback rebounded on Friday, following the release of the US employment report for July and subsequently, some comments on tax reform from the Director of the US National Economic Council, Gary Cohn. Kicking off with the jobs data, nonfarm payrolls rose by 209k, more than the consensus of 183k. The unemployment rate ticked down, while average hourly earnings accelerated in monthly terms, both in line with expectations.

The second and biggest leg higher in USD came after Cohn said that the US administration aims to reduce the corporate tax rate to around 23%. He added that the new plan will include incentives for US corporations to repatriate cash held abroad. If such a plan materializes, a repatriation would likely provide a significant boost to USD in the longer-term, as corporations would need to convert billions held in foreign currencies back to dollars.

Nonetheless for now, despite Cohn’s remarks and strong jobs data, we are not ready to call for a reversal in the dollar yet. Even though the market reacted to Cohn’s comments, any tax-reform plan is still months away from being announced and implemented, at the least. On the data front, both investors and the Fed are aware that the labor market is robust and thus, further improvement in that sector is unlikely to lift materially the probability for another hike by year end. Indeed, the implied probability for another hike in 2017 stayed more or less unchanged at around 50% in the aftermath of these data. In our view, a strong rebound in inflation is needed before rate-hike bets rise materially and help the dollar change its fortune. In this respect, CPI data due out on Friday will probably attract attention, though the consensus is for another set of lackluster prints.

EUR/USD tumbled on Friday in the aftermath of the US jobs data and Cohn’s comments. The rate fell back below 1.1830 (R1), but hit 1.1725 (S1) and started to recover. The rate continues to trade above the short-term uptrend line taken from the low of the 22nd of June and thus, we consider the near-term picture to still be positive. We would treat Friday’s slide as a corrective phase and we expect the bulls to continue erasing these losses. We believe that they may challenge the 1.1830 (R1) line as a resistance soon. A clear break above that level could set the stage for another test near the 1.1900 (R2) territory.

Oil producers meet to discuss compliance with cuts

Today, oil traders will probably turn their sights to Abu Dhabi, where OPEC and non-OPEC officials will meet to discuss why some countries are falling behind in their pledges to cut production as agreed in May. Any signals that the cartel may take a harder line on members not complying with their quotas, or that OPEC could take other steps to boost compliance, may help oil prices to trade higher.

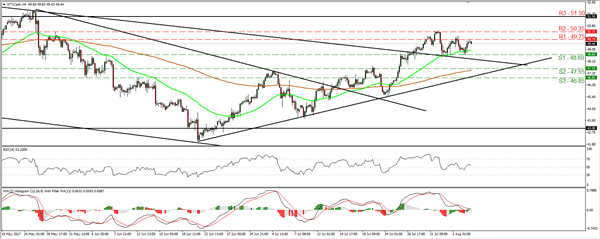

WTI traded north on Friday, despite the dollar’s strength on the US employment report and Cohn’s remarks. The price rebounded after it hit once again support near the 48.60 (S1) line, but the recovery stopped at 49.75 (R1). WTI continues to trade above the upper bound of the medium-term downside that contained the price action from the beginning of February until the 27th of July, which keeps the door open for further recovery. A break above the 50.35 (R2) obstacle would confirm a forthcoming higher high on the 4-hour chart and could open the way for the critical hurdle of 51.50 (R3).

That said, we repeat for the umpteenth time that we are mindful on whether a healthy long-term uptrend can be established. Any future gains may be capped by the USD 51.50 – 55.00 range, where US producers may be tempted to increase production significantly.

As for the rest of today’s highlights:

The only noteworthy indicator we get is Germany’s industrial production for June. We also have two speakers on the agenda: St. Louis Fed President James Bullard and Minneapolis Fed President Neel Kashkari.

As for the rest of the week:

On Tuesday, China’s trade balance for July is out while on Wednesday, we get the nation’s CPI and PPI data for the same month. On Thursday, during the early Asian morning, the RBNZ will announce its policy decision. We believe that policymakers could deliver a more cautious narrative on the economy, and perhaps even issue a warning about the recent strength of NZD. Finally on Friday, we will get the highly-anticipated US CPI data for July.

EUR/USD

Support: 1.1725 (S1), 1.1655 (S2), 1.1615 (S3)

Resistance: 1.1830 (R1), 1.1900 (R2), 1.1980 (R3)

WTI

Support: 48.60 (S1), 47.55 (S2), 46.85 (S3)

Resistance: 49.75 (R1), 50.35 (R2), 51.50 (R3)