{kind=link}

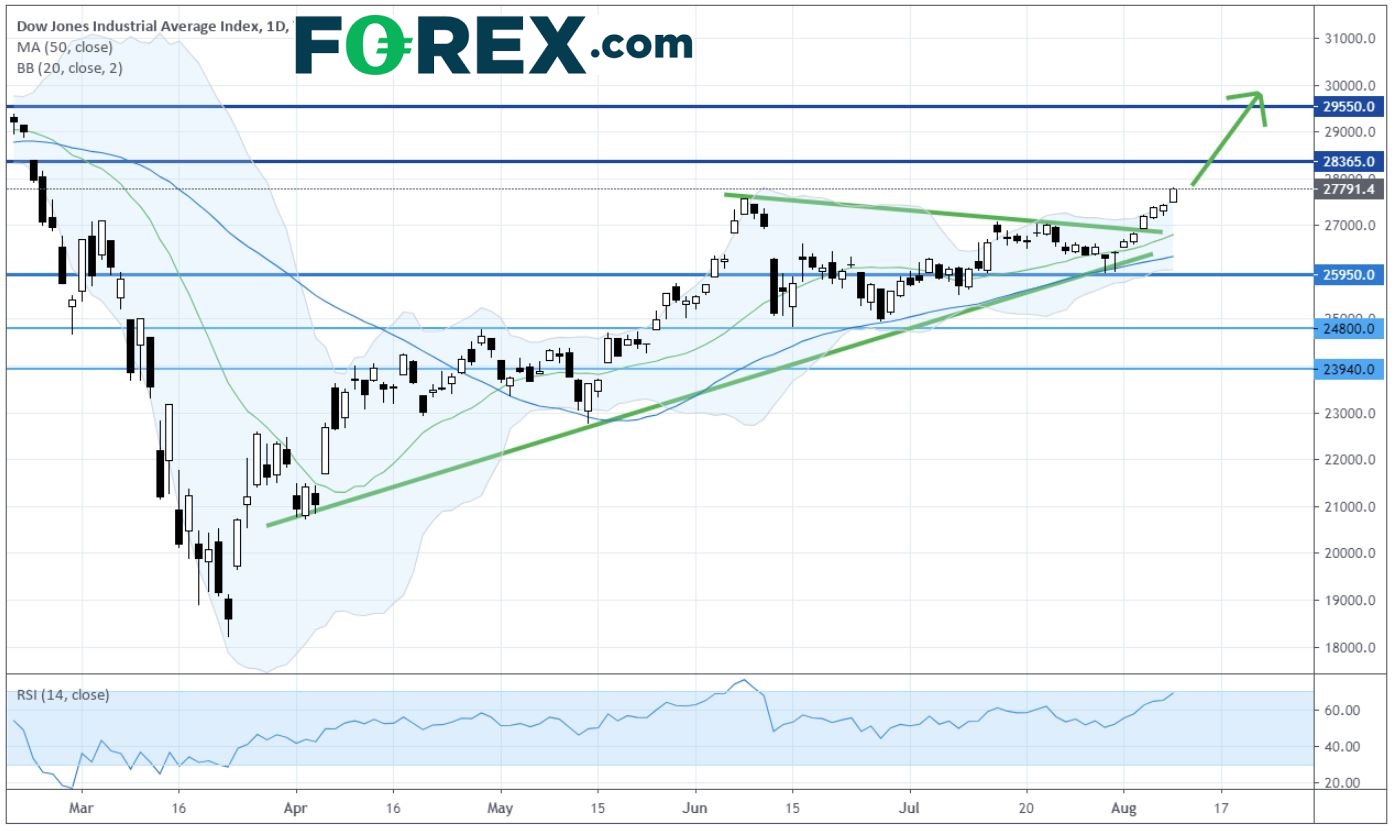

On Monday, U.S. stocks closed mixed again as tech stocks lagged behind. The Dow Jones Industrial Average jumped 358 points (+1.30%) to 27791 posting a seven-session rally. The S&P 500 added 9 points (+0.27%) to 3360, while the Nasdaq 100 dropped 54 points (-0.49%) to 11085.

Dow Jones Industrial Average: Daily Chart

Automobiles & Components (+3.86%), Energy (+3.08%) and Consumer Durables & Apparel (+3.01%) sectors traded higher, while Software & Services (-1.42%), Media (-0.72%) and Pharmaceuticals, Biotechnology & Life Sciences (-0.5%) sectors were under pressure.

MGM Resorts International (MGM +13.77%), Wynn Resorts (WYNN +9.96%), Royal Caribbean Cruises (RCL +10%), United Airlines (UAL +9.35%) and Fedex (FDX +8.96%) were top gainers.

European stocks were stable. The Stoxx Europe 600 Index climbed 0.30%, Germany’s DAX 30 edged up 0.10%, France’s CAC 40 gained 0.41% and the U.K.’s FTSE 100 was up 0.31%.

The benchmark 10-year Treasury yield stepped up to 0.571% from 0.562% Friday.

Spot gold price was down for a second session falling $7.00 to $2,027 an ounce. Spot silver price jumped 2.8% to $29.12 an ounce, the highest close since March 2013.

U.S. WTI crude oil futures (September) charged 1.7% higher to $41.94 a barrel.

On the forex front, the ICE U.S. Dollar Index gained 0.2% on day to 93.61, up for a second straight session.

EUR/USD fell 0.4% to 1.1741. Later today, the German ZEW Current Situation Index for August will be released (-69.5 expected).

GBP/USD marked a day-low of 1.3020 before closing up 0.2% at 1.3074. Investors will focus on the U.K. jobless rate for the three months to June due later in the day (steady at 4.2% expected).

USD/JPY was little changed at 105.96.

Meanwhile, USD/CAD dropped 0.2% to 1.3357, as the Canadian dollar was lifted by a rebound in oil prices.

Other commodity-linked currencies were broadly lower against the greenback. AUD/USD slipped 0.1% to 0.7150 and NZD/USD was down 0.2% to 0.6590.