{kind=link}

U.S. Review

Service Elevator

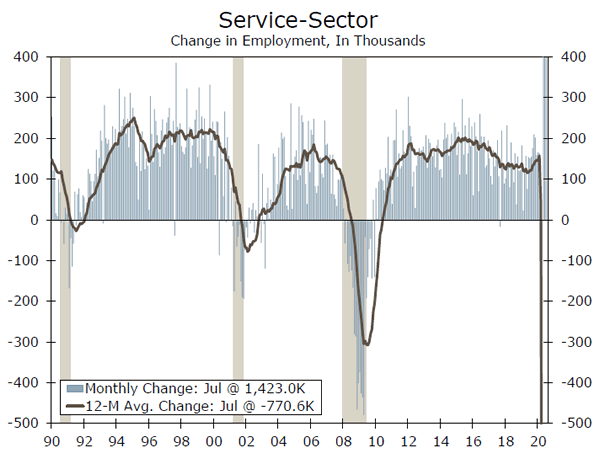

- Despite rising virus case counts in July, unexpected strength in the service sector was evident in the economic data this week.

- The better-than-expected July jobs report was driven primarily by hiring in the service sector, which accounted for 1.42 million of the overall 1.76 million jobs added in the month.

- The ISM index for the service sector was arguably the biggest economic surprise of the week climbing to 58.1 with some subcomponents reaching multi-year highs.

- It remains a long road to recovery and the virus still sets the timetable, but numbers moved in the right direction this week.

Signs of Resilience

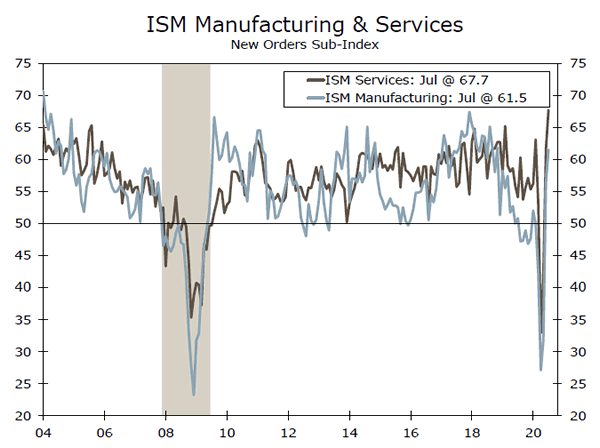

Even as virus case-counts rebounded in July, the re-opening of the economy continued largely undaunted. The manufacturing recovery picked up momentum during the month, with the ISM index rising to 54.2. Underlying details of the manufacturing report paint a brighter picture than previous months as well.

The service sector was widely expected to weaken in July amid the flare-up of new cases, but the rebranded ISM Services (formerly called ISM Non-Manufacturing) rose to 58.1 in July. In both reports, it is worth noting these ISM diffusion indexes can be prone to big swings at turning points in the cycle and are based on the share of firms reporting an increase in activity versus a decrease. It is therefore a measure of the breadth rather than the degree of change in activity within them. Service sector business activity at a 16-year high in July is a great example of this. Obviously amid a pandemic, the service sector is not more active than it has been in 16 years, rather a broad group of businesses note improvement relative to the prior month. Still, the broad improvement in both manufacturing and services activity offer signs of resilience as the economy begins to dig out from the pandemic.

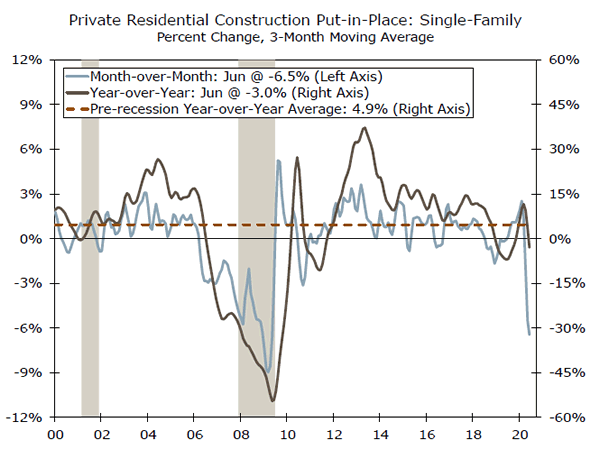

Soft Patch for Construction Spending

So while July data looked a bit better, figures released this week revealed that June was not a particularly good month for construction activity. Construction outlays fell 0.7% during June, well below the consensus estimate of a 1.0% increase. Private and public construction spending both fell 0.7%.

The continued decline in construction spending for single-family homes is probably the biggest surprise in the June report. Spending for single-family homes fell 3.6% in June. Most of the recent data here have been positive with sales, buyer traffic, mortgage applications and pending sales collectively running at their strongest pace in years. The weakness is due in part to the fact that the bulk of construction outlays for new homes tend to occur 45 to 60 days after construction begins. The uptrend in housing starts figures suggests single-family home construction is likely headed higher.

Labor Market Recovery

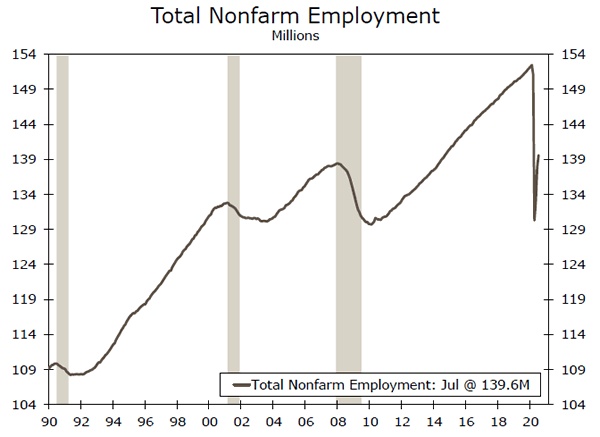

Friday’s employment report showed that employers added 1.763 million people to their payrolls in July. Job growth in prior months saw slight upward revisions as well. The jobs number beat expectations, here again the upside strength was in the service sector, which added 1.423 million, though manufacturing jobs also rose slightly (+26K).

The U.S. economy lost just over 22 million jobs during the pandemic. In the past three months, roughly 9.3 million jobs have come back, more than 40% of the share that was lost.

For those who have not found work, this week is a difficult one as it marks the first week without the $600 federal supplement to topup state-level unemployment benefits. While Congress continues to debate another relief package the loss of supplemental benefits could become a headwind for consumer spending. The consumer has been a key driver of the services recovery thus far.

U.S. Outlook

CPI • Wednesday

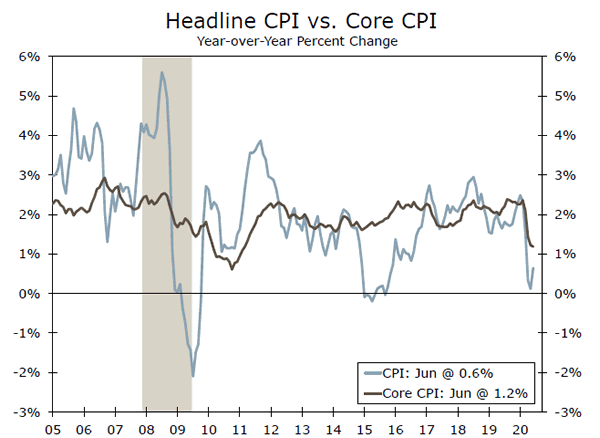

In June, the streak of deflationary readings came to a halt, with headline CPI increasing 0.6%. Retail gasoline prices jumped 12.3% last month and accounted for more than half of the gain in overall CPI. Food prices continue to rise as grocery stores adjust to stronger demand. Excluding food and energy, core CPI rose a more moderate 0.2%, restrained by a slowdown in rents.

The impact of the coronavirus pandemic on the inflation outlook is uncertain. Though as demand continues to recover and firms feel like they can relax discounting efforts, consumer prices should continue to edge higher. Assuming our base case unfolds (no significant resurgence of the virus leading to another widespread lockdown), we expect prices to steadily rise in the coming months, albeit at a modest pace.

Previous: 0.6% Wells Fargo: 0.3% Consensus: 0.3% (Month-over-Month)

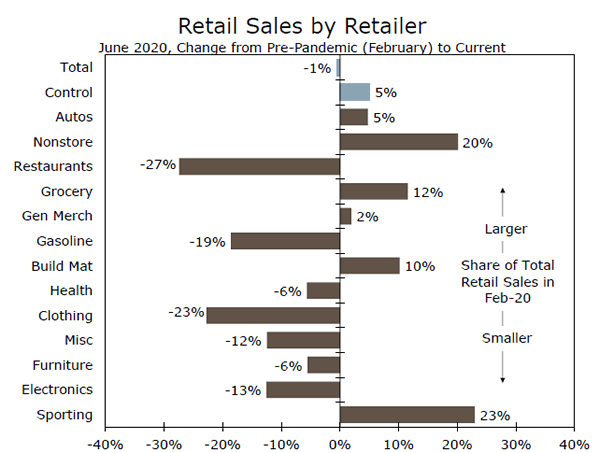

Retail Sales • Friday

Retail sales have rebounded strongly over the past two months, with total sales just 0.6% off its February pre-virus level and control group sales are 5.0% above February levels. The broad based easing of lockdowns last month, alongside pent up demand, resulted in retail sales rising 7.5% in June, with gains reported in nearly every major retail sector.

That said, the composition of spending is not evenly divided. Traditional retail stores are still struggling, especially anything in the services sector. Consumers have shifted spending towards online shopping and household items/improvements given that workers are spending more time at home these days. We remain cautious on the near-term consumer spending outlook, reflecting a resurgent virus, the absence of an extended fiscal stimulus deal and persistent uncertainty about the outlook in general.

Previous: 7.5% Wells Fargo: 1.4% Consensus: 1.8% (Month-over-Month)

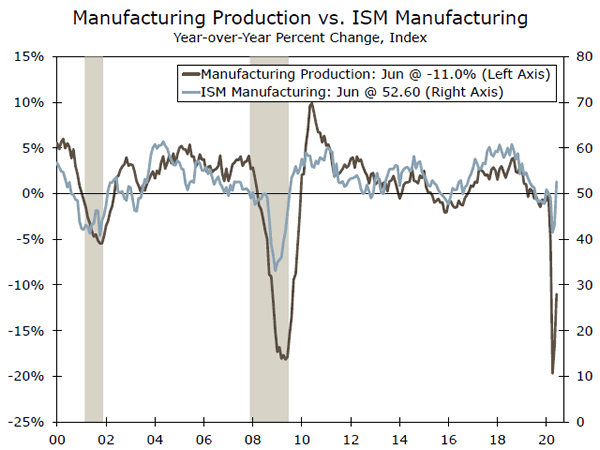

Industrial Production • Friday

Clawing its way back from the monstrous declines in March and April, total industrial production increased 5.4%, its largest monthly gain since 1959. Manufacturing production recovered solidly with every major manufacturing industry up, and most notably motor vehicle production, which has staged a rapid recovery over the past two months, rose more than 100%. Utility output also increased, while the drag from mining eased as oil demand has firmed a bit.

Looking ahead, the ISM manufacturing index increased for the third straight month in July, suggesting the industrial sector is picking up some steam in the face of firmer orders and lean inventories. That said, we are cautious on the outlook given depressed global growth, weak capex, high unemployment and a resurgent virus which, collectively, provide strong headwinds to the factory sector. Industrial output is still nearly 11% below prepandemic levels.

Previous: 5.4% Wells Fargo: 2.8% Consensus: 3.0% (Month-over-Month)

Global Review

Global Economy Continues to Recoup Lost Ground

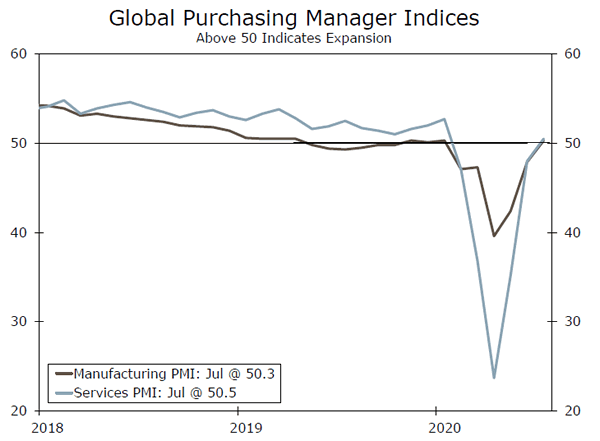

- There were more signs of global recovery this week and PMI surveys improved further across the world. Indeed, the global manufacturing and services PMIs rose above the breakeven 50 level, suggesting the global economy has returned to positive growth in Q3.

- The Eurozone economy showed increased momentum in June as retail sales returned to pre-pandemic level and industrial output rose for the region’s four largest economies. We expect that improved Eurozone momentum carried into Q3. Meanwhile, the recovery is slower in Latin America, where Brazil and Mexico both still appear to be contracting.

Eurozone’s More Encouraging Run Continues

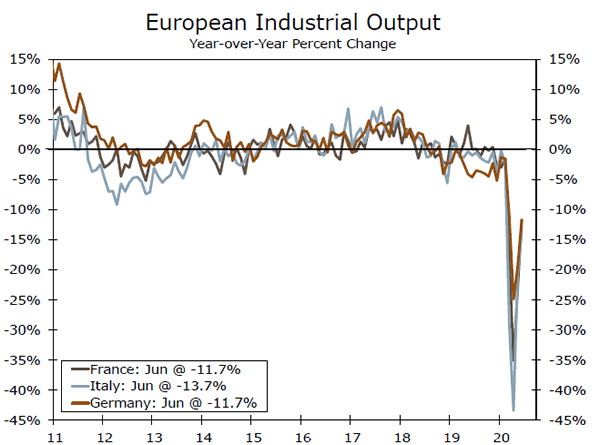

The incoming flow of data continues to point to better momentum for the Eurozone economy in June, after what was a very tough second quarter as a whole for the region. June retail sales rose 5.7% month-over-month, slightly less than expected, although the May sales increase was revised higher to 20.3%. With the June gain, retail sales have returned to their February (or prepandemic) levels. Eurozone manufacturing also continues to recover, albeit at a more gradual pace. June industrial output rose across the Eurozone’s four largest economies. German industrial output rose 8.9% month-over-month, while in France, Italy and Spain output rose 12.7%, 8.2% and 14.0%, respectively. That said, the year-over-year change remains well into negative territory for all four countries. The overall improvement in the retail and manufacturing sectors suggest a decent-size rebound in GDP could be in store for the Eurozone in the third quarter, though a moderate but perceptible uptick in new COVID-19 cases over the past several days does pose some risk to the extent of that gain.

Latin American Laggards

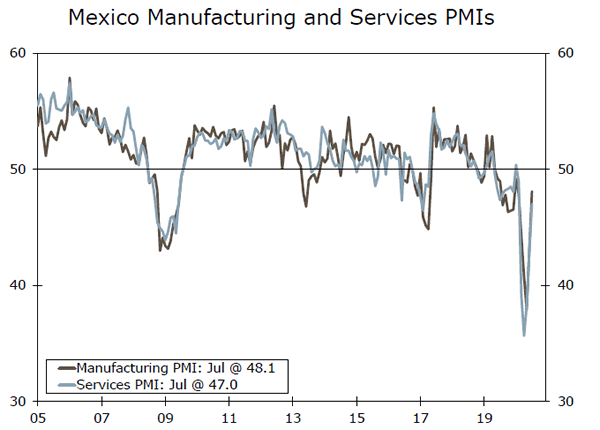

The environment is more challenging across Latin America, where recovery is slower than most G10 economies. In Brazil there has been some improvement in manufacturing, with the July manufacturing PMI rising to 58.2 and June industrial output rising 8.9% month-over-month. The rebound in the service sector remains much slower, however, as the July services PMI rose to just 42.5, suggesting the overall economy is probably still in contraction. Against this backdrop Brazil’s central bank cut its Selic rate a further 25 basis points to a record low 2.00%, but indicated there was only limited space for further monetary easing. Recovery is also gradual in Mexico. The July manufacturing and services PMIs rose in July, to 48.1 and 47.0, respectively. However, with both remaining below the breakeven 50 level, Mexican economic growth has likely not yet returned to positive territory. Finally, Chile’s June economic activity indicator rose 1.7% monthover- month, though after large declines in March, April and May, activity is still 15% below its February peak.

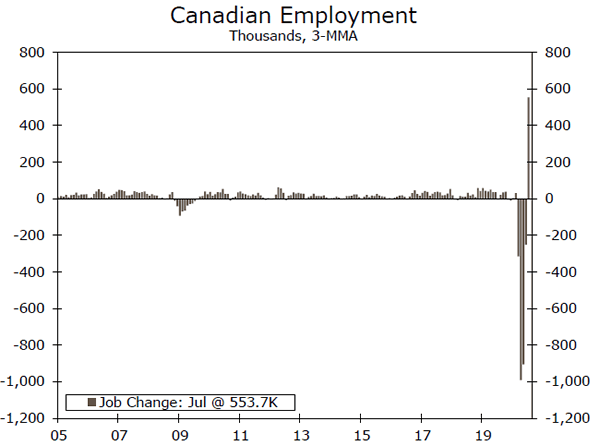

Canada’s Labor Market Recovering Lost Ground

July saw another positive jobs report from Canada as employment rose 418,500, more than expected and a third straight monthly increase. The details of the report were also reasonably constructive as full-time employment rose 73,200 and part-time employment jumped 345,300, although private sector jobs did rise some 375,800. Total hours worked also rose 5.3% month-overmonth, while the unemployment rate has continued to reverse its upward spike from earlier this year, declining to 10.9%.

While there is still some way to go, the Canadian labor market has made decent progress in recouping its losses from early 2020. During March and April, Canadian employment fell by a cumulative 3,004,500. In May, June and July however, employment rose by 1,661,000, meaning more than half of the decline in jobs has already been recovered. The unemployment rate does have a ways to go, however, before it falls to it prepandemic rate of 5.6%.

Global Outlook

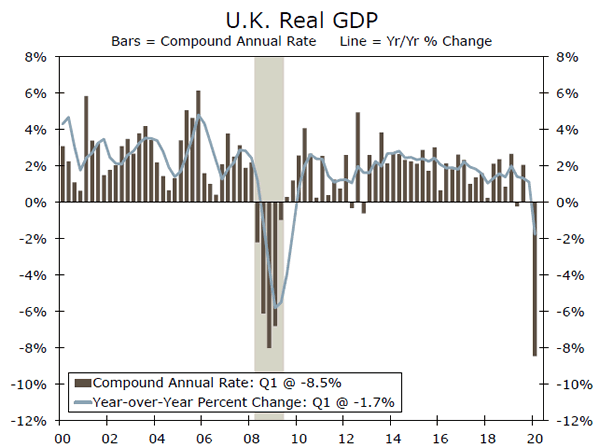

United Kingdom Q2 GDP • Wednesday

The release of Q2 GDP figures will provide a comprehensive assessment of the economic damage caused by COVID-19. The Q2 fall in GDP is expected to be especially large–we forecast a 20.5% quarter-over-quarter decline, matching the consensus estimate. The Q2 softness in the economy should be broad based, with services output forecast to fall 20.1% and industrial output by 16.7%, while consumer and investment spending should also fall sharply.

In addition to the quarterly GDP figure, June GDP figures will be keenly watched to see how quickly (or not) the U.K. economy is recovering from its Q2 downturn. After April GDP collapsed 20.3% month-over-month, May saw a very modest 1.8% increase. The consensus looks for a stronger outcome in June. Overall GDP is forecast to rise 8.6% month-over-month, with services and industrial output expected to rise 8.0% and 10.0%, respectively.

Previous: -2.2%% Wells Fargo: -20.5% Consensus: -20.5% (Quarter-over-Quarter)

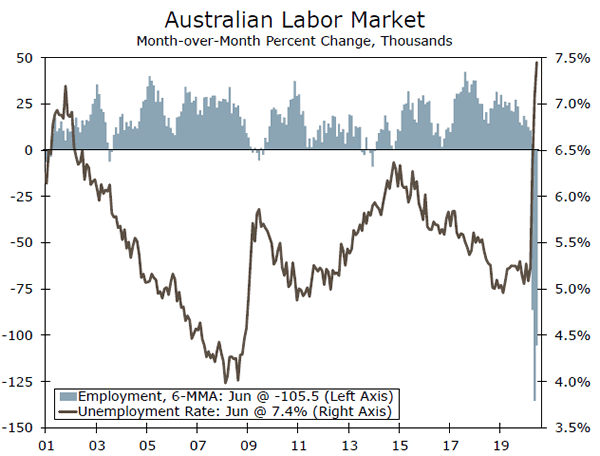

Australian Employment • Thursday

Australia’s July employment report will provide an early read on Q3 economic activity, although it might be too early to capture the full economic effects of the renewed lockdown measures imposed in Melbourne and across Victoria. Following especially large job declines in April and May, employment partially recovered in June with a gain of 210,800. For July, however, the pace of job recovery is expected to slow. The consensus forecast shows employment rising by 30,000, while the unemployment rate is expected to rise to 7.8%. As usual, it will be worth watching the split of full-time versus parttime jobs.

Given the timing of monthly employment survey period it is likely the full effects of the renewed Victoria lockdown will not be captured, and given declines in weekly payroll figures we would not be surprised to see an outright decline in Australian employment when the official monthly labor market data for August are released.

Previous: 210,800 Consensus: 30,000 (Monthly employment change)

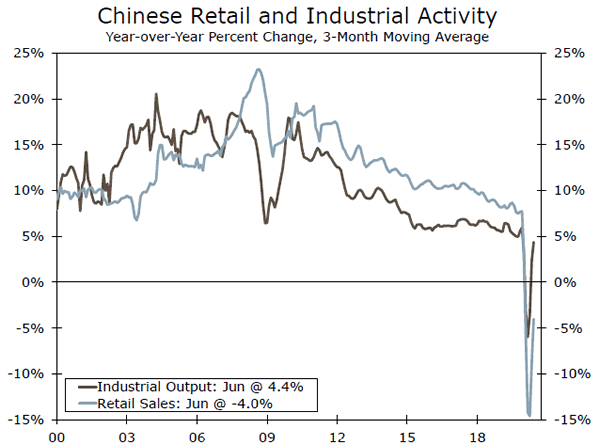

China Retail & Industrial Data • Friday

China’s economy has been leading the global economic recovery from the COVID-19 crisis, and we expect that trend continued into July. Already released survey data for July were mixed, with the manufacturing PMI edging higher and the services PMI easing, although both remained above the breakeven 50 level.

Meanwhile, economists expect a more consistent improvement in activity data for July. The consensus forecast is for industrial output to firm further to 5.1% year-over-year, which would be the largest increase since December. The rebound in retail activity continues to be more gradual, although July retail sales are expected to rise 0.1% year-over-year, which would be the strongest reading (and first increase) since December. Among the week’s other releases, July consumer price inflation should be little changed, with the consensus forecasting a 2.6% year-over-year gain. We still see China’s full-year 2020 GDP on track for a modest gain of 1.2%.

Previous: Retail Sales -1.8%; Industrial Output +4.8% Consensus: 0.1%; 5.1% (Year-over-Year)

Point of View

Interest Rate Watch

Treasury Keeps Terming out the Debt

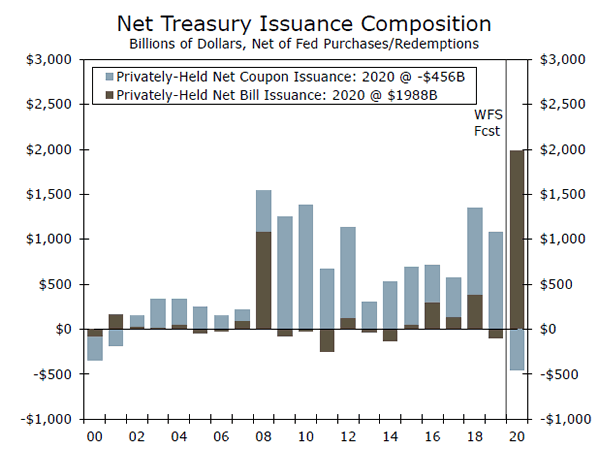

The U.S. Treasury significantly increased nominal coupon auction sizes at this week’s refunding announcement. All told, the increases were particularly noteworthy at the long-end of the Treasury curve. For the 10Y, 20Y and 30Y securities, new and reopened auctions are set to increase by $6 billion, $5 billion and $4 billion, respectively. The median primary dealer expected quarterly increases of $3 billion, $2 billion, and $3 billion for the 10-, 20-, and 30-year respectively.

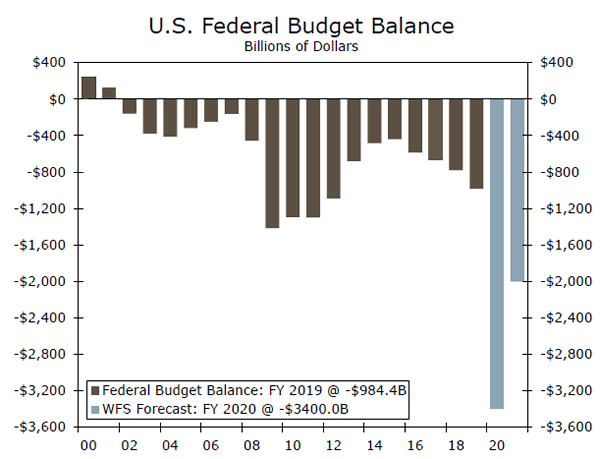

Given the highly uncertain fiscal outlook, we are somewhat surprised Treasury moved so aggressively. Accurately estimating the Treasury’s financing need remains the biggest question mark in the outlook. In Q2- 2020, the financing need was more than $1 trillion smaller than Treasury projected in May 2020, highlighting just how uncertain the current situation is.

Our financing need estimate for H2-2020 is around $1.5 trillion. Treasury’s projection for the same period is about $3.0 trillion, but this estimate assumes $1 trillion of borrowing in anticipation of additional fiscal legislation being passed, something our forecast does not explicitly incorporate. Yet, even with such an aggressive pace of long-term debt issuance, net supply of securities 2Y and longer is still likely to be negative for 2020 after accounting for Fed purchases (middle chart).

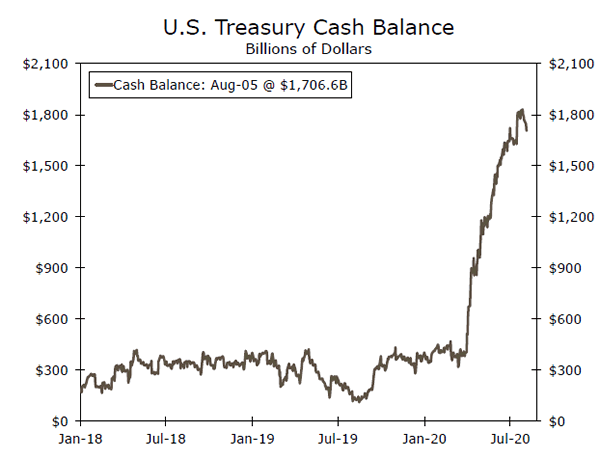

In short, Treasury is playing it safe in its baseline borrowing plans, but the Treasury supply outlook over the next few months could change on a dime. Fortunately for the Treasury, it is sitting on an extraordinarily large cash balance, which gives it flexibility should another fiscal relief package quickly come to fruition (bottom chart).

We have repeatedly refrained from adding a large fiscal package to our baseline forecast, and the ongoing negotiations over the past few weeks illustrate one key reason why. At this point, we would not be surprised if the negotiations are put on hold until after the August recess. But even if a package comes to fruition, the size and composition is highly uncertain, and by extension so is the outlook for the financing need and issuance of Treasury securities.

Credit Market Insights

Argentina Finally Reaches a Deal

After months of difficult talks, Argentina and a group of major bondholders reached an agreement to restructure roughly $65 billion of its foreign-law bonds on Tuesday. According to the statement released by the Argentine government, the deal will provide “significant debt relief” to the country after the government has defaulted on its sovereign debt obligations nine times, including the most recent May default when the country failed to make a $500M interest payment. As outlined, in the agreement, payment dates for some new bonds will be adjusted, moving its coupon payments to January and July from March and September. This will improve the value of the proposal for creditors without increasing the total amount of principal or interest payments. Although the official statement did not provide the amount of principal haircut, the deal may be worth about $0.55 on the dollar. The deadline for additional creditors to formally accept the debt offer has been extended to August 24 from August 4, while the settlement date remains unchanged on September 4.

The agreement with bondholders is an encouraging step toward supporting the struggling economy and should allow the government to now focus on talks with the International Monetary Fund to restructure and replace its 2018 failed bailout agreement. Following the announcement, Argentine bonds rallied, with the 100-year dollar-denominated bond jumping roughly 10% on the day, to the highest level since February.

Topic of the Week

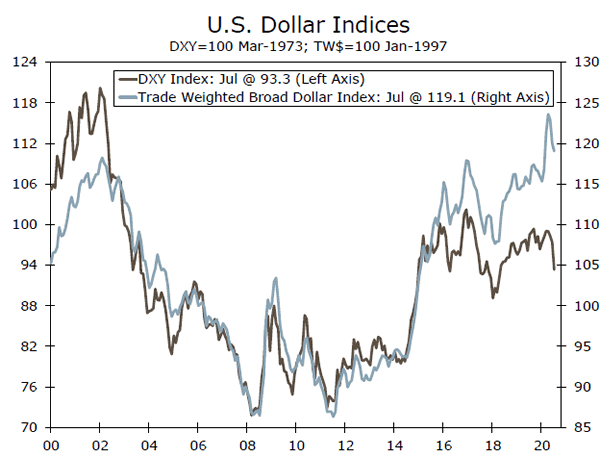

What Marks the Spot for U.S. Dollar Weakness?

The U.S. dollar has weakened in recent weeks, with the dollar spot index down around 4% over the past month, the most recent down leg of a weakening trend that has seen this measure of the greenback fall almost 10% since March to roughly its lowest level in the past two years.

While markets rely on dollar spot, or the DXY index, which is a reflection of FX markets globally, many economists follow measures that reflect trading activity like the Fed’s trade-weighted broad dollar index (TW$). As the name implies, this measure more accurately reflects the dollars’ eventual impact on trade. The key difference between the two is in their weighting of currencies. The euro accounts for more than 50% of the DXY index, which only includes five other currencies, while the TW$ gives a more considerable weight to 26 currencies based on their volume of bilateral trade.

While the two indices typically move together (top chart), they can differ based on what is driving dollar weakness, as is one of many factors today with the euro being a particular standout gaining more than 10% versus the dollar since mid-March. From its March peak until now, the TW$ is off just 7% versus the more-sizeable 10% decline in the DXY index.

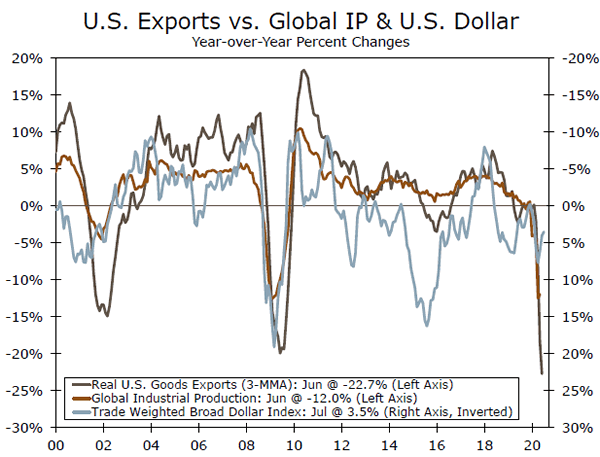

Recent dollar weakness raises concern of what further depreciation means for the economy more generally. In theory, and holding other factors constant, a weak dollar should make exports less expensive to foreigners and imports more expensive to U.S. buyers, and could result in higher inflation. Dollar depreciation should help exports at the margin, but growth in the rest of the world is a much larger influence on U.S. export growth (bottom chart). If, as we expect, the global economy begins to recover, export growth should pick up with a weaker dollar providing some extra wind in the sails. In terms of imports, total domestic demand began to recover in May and June and we expect that recovery continued into Q3. Imports are likely to rise as domestic demand increases, even despite a weaker dollar providing a modest headwind. Recent history shows a weaker dollar does not always lead to higher price growth. Take 2002- 2008 for example, there was sustained dollar weakness but that period actually saw inflation below 3% on average.