{kind=link}

- Non-farm payrolls rose another 1.8 million in July

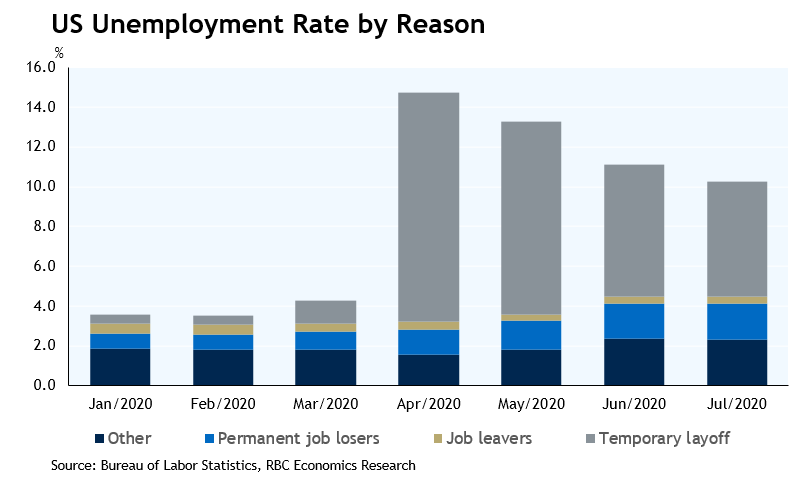

- Unemployment rate fell to 10.2%

- Hours worked still down 9% vs. pre-pandemic; concerns linger over long-run outlook

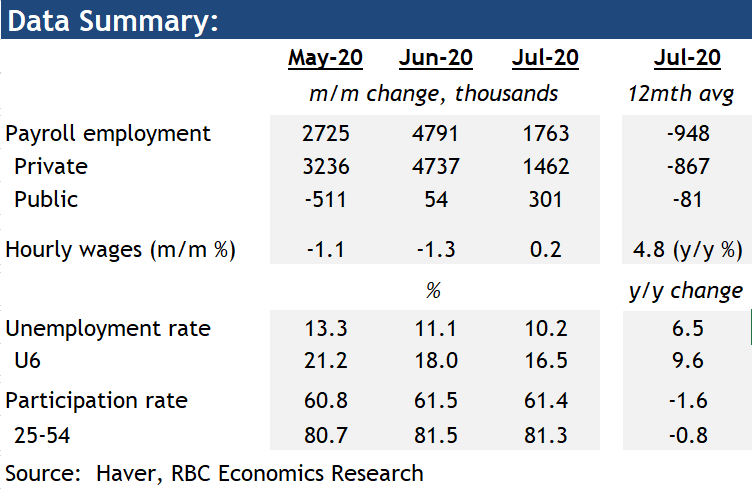

Payroll employment was broadly in line with consensus expectations in July, increasing 1.8 million and signaling continued recovery in the labour market despite escalating virus spread in some regions. Overall employment rose 9.3 million cumulatively since May, retracing 42% of the unprecedented drop over March and April. 10 out of 13 private industries added jobs, led by leisure and hospitality, adding one third of the total gain in July. Government employment also added to the increase, boosted in part by a seasonal bump in education services.

The unemployment rate fell to 10.2%, with much of the drop again coming from a decline in workers on temporary layoff. Though the number of people that are unemployed but on permanent layoff was virtually unchanged in July after having increased throughout the lockdown period as well as the initial recovery. The labour force participation rate unexpectedly ticked slightly lower. That combined with broader measures of under-utilization continue to point to more weakness in the labour market than the official unemployment rate would suggest. Although the gap between the U3 (official unemployment rate) and the U6 (broader measure including discouraged workers, involuntary part-time workers, and other ‘marginally attached’ workers) has been narrowing since April.

The end of July saw the expiration of the $600/week federal top-up of unemployment benefits, which to-date has been successful at providing a floor for household income, and subsequently helps boost household spending. But the labour market backdrop is still exceptionally weak. Hours worked (for private employees) remained 9% below its February level in July and initial claims rose again in the two weeks immediately after July’s payroll survey week, before falling in the week after. On the plus side, growth in new virus cases in states over the south and west appeared to be decelerating again since mid-July. And we expect that Congress will ultimately agree to some form of additional fiscal aid. That should continue to offer relief to household finances, though likely less generous than the last iteration. We maintain our view that output and labour market conditions will both continue to broadly improve, but remain weak, for the remainder of 2020.