{kind=link}

- GDP declined an unprecedented 32.9% (annualized rate) in Q2

- End of quarter likely less-bad than the beginning

- Concerns bounce-back faltering alongside virus spread in Q3

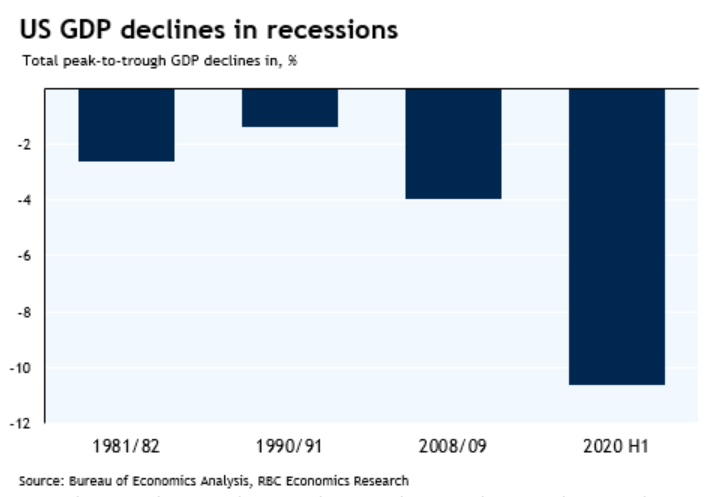

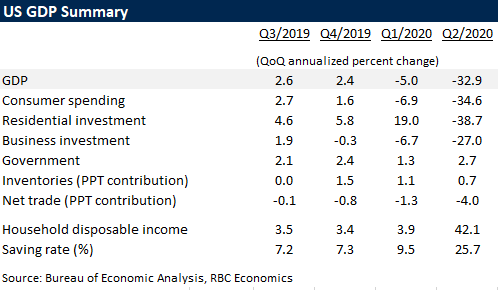

The drop in economic activity in Q2 was already widely known to have been unprecedented. The 33% (annualized) drop in GDP in the quarter was close to expectations but was still alone more than twice the total 6-quarter peak-to-trough drop in the 2008/09 recession. Weakness was widespread with households and businesses pulling back as containment measures kept workers (and spenders) at home across broad swaths of the economy. That meant that even spending that is normally resilient in an economic downturn was exceptionally soft. The (record) 35% drop in consumer spending in Q2 was led by a whopping 63% (annualized) drop in health-care spending as non-COVID services shut down.

The Q2 weakness was related to containment measures and consumer fear of going out rather than a drop in household purchasing power. Indeed, household disposable incomes surged 42% in Q2, and the saving rate spiked to 25.7% on average, as unprecedented government income supports helped to offset unprecedented wage losses.

Easing virus containment measures over May and June meant that household spending was likely significantly stronger at the end of the quarter than at the beginning. We expect tomorrow’s monthly spending report will show consumers purchased about 3% less goods and services than a year ago in June, still not good but significantly better than the 16% year-over-year drop in April. Still, business spending has, to-date, been slower to bounce back. The US Federal Reserve will keep interest rates low for the foreseeable future. But it remains unclear that further significant fiscal stimulus can work its way through congress, and that has left downside risks for near-term household incomes if additional support measures cannot be approved.

The resurgence of virus spread in much of the United States will stunt the pace of the near-term economic rebound, and is a reminder that there are limits to the extent that the economy can rebound to a ‘new normal’ in the absence of a vaccine or more effective treatments. Initial jobless claims have ticked higher over the last two weeks and are still at historically unprecedented levels. We continue to expect GDP will remain sharply below year-ago levels (-5%), and the unemployment rate elevated, at the end of this year.