{kind=link}

U.S. Highlights

- A tug of war between encouraging vaccine news and hopes of new economic stimulus, and early indications that the recovery might be stalling, is fueling financial market volatility.

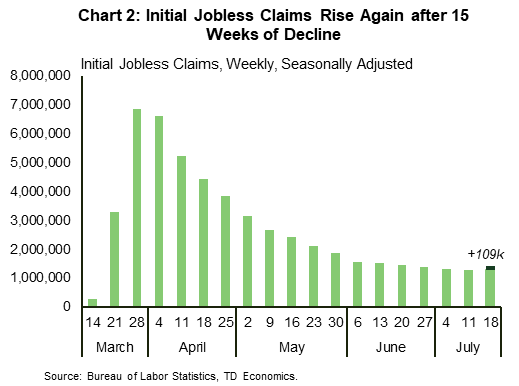

- Jobless claims rose to 1.42 million last week after declining for 15 consecutive weeks, suggesting that the labor market recovery might be weakening. By contrast, the housing sector continues to impress as existing home sales soar by 20.7%.

- Congress returned to work and is crafting the next installment of aid to household and businesses. Divergences remain, but an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week.

Canadian Highlights

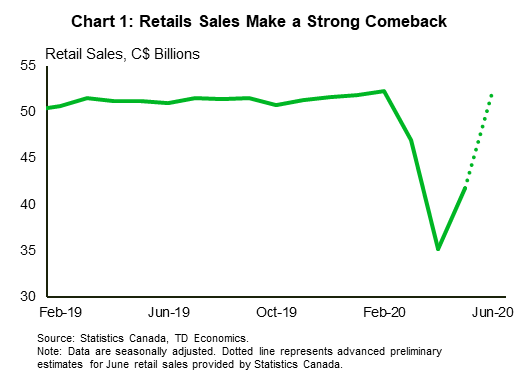

- Retail sales registered a strong comeback in May on the back of easing lockdown measures. Gains were seen across the board, with 10 out of the 11 sectors reporting an increase in sales.

- Thanks to unprecedented monetary and fiscal support, deflationary fears have been allayed, at least for now. Consumer price inflation moved into positive territory, increasing 0.7% compared to the same period last year.

- Reopenings have led to a resurgence of new cases in some provinces. To prevent a second wave, British Columbia has already re-enacted some restrictions that were previously lifted.

U.S. – Recovery Risks Stalling Out as Pandemic Worsens

Financial markets were in a tug of war this week as investors weighed encouraging vaccine news and hopes of new economic stimulus against indications that the recovery might be stalling. Later in the week, flaring tensions between the U.S. and China also weighed on sentiment. As of writing, the S&P 500 was on track to end the week flat.

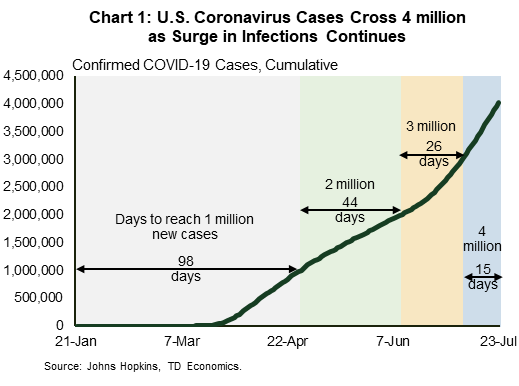

The pandemic marked another gloomy milestone in the U.S. as confirmed coronavirus cases breached the four million mark. This represents a sharp acceleration from just two weeks ago when cases topped three million (Chart 1). From a regional standpoint, California has now surpassed New York for the highest number of cases at over 430,000. With cases continuing to soar in several states, reopening plans are increasingly being rolled back and restrictive measures reintroduced to curb the spread. In one of the latest developments, bars that do not serve food are no longer permitted to offer indoor seating in Chicago, while parties are now limited to six people at restaurants.

The surge in infections is weighing on economic activity, and this is starting to come through in high-frequency indicators. Initial jobless claims, which had declined for fifteen straight weeks, rose for the week ended on July 18, 2020 (Chart 2). Indeed, filings for unemployment insurance increased by 109,000 to 1.42 million last week, up from 1.31 million in the week prior. While the latest reading is still far below the late-March peak when weekly filings topped 6.9 million, it suggests that the recovery may be losing steam. The historical relationship between claims and employment suggests that employment growth will slow in July relative to the strong gains seen in June and May. This view was also echoed in the Census Bureau’s Household Pulse Survey, which points to increased job losses in July.

On a more positive note, the U.S. housing market is showcasing a recovery that appears to be stronger than other areas of the economy. Following three consecutive months of contraction, sales of existing homes made a soaring comeback, increasing by 20.7% in June. Similarly, new home sales shattered expectations with a 13.8% jump. As noted in a recent report, strong demand from millennials taking advantage of falling mortgage rates is a big factor driving this resiliency. In the months ahead, homebuyers from this age cohort should put a floor under housing demand. However, the resurgence in COVID-19 cases will likely weigh on the recovery here as well.

With risks increasingly tilted to the downside, policymakers are working on the next set of measures to help support the economy. Across the Atlantic, hard-fought negotiations between EU leaders finally came through earlier in the week in the form of a €1.8 trillion stimulus package. Closer to home, Congress returned to work this week and is crafting the next installment of aid to households and businesses. While divergences over the scope and the size of the next package remain, an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week. Here’s hoping that the next array of policy responses is enough to keep the recovery on track.

Canada – Retail Activity is Back with a Bang

Financial markets started the week on strong footing but ended on a more subdued note as the S&P/TSX Composite registered a 1% loss (as of writing). However, the index is still 42% higher than the lows seen in late-March. Elsewhere, oil markets seesawed this week, but WTI managed to record a 1.6% gain as of writing, settling down at around US$ 41.

In terms of economic data, Canadian retail sales registered a strong rebound in May, surging 18.7% as lockdown measures began to ease (Chart 1). Pent-up demand also contributed to the rebound, with the strongest gains in sectors – such as clothing and autos – that were hit the hardest by the lockdown. Gains were seen across the board, with 10 out of the 11 sectors reporting an increase in sales. June sales will be approaching pre-lockdown levels if they grow according to Statistics Canada’s preliminary forecast of 24.5%.

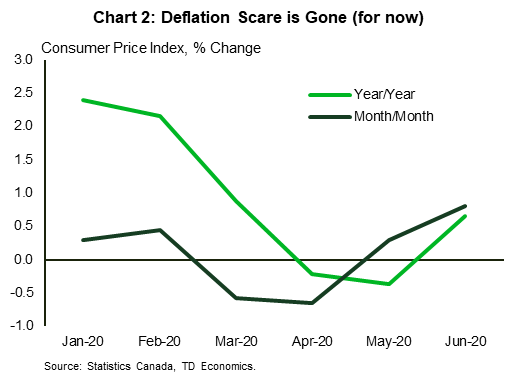

Thanks to unprecedented monetary and fiscal support, deflationary fears have been allayed, at least for now. Consumer price inflation in June bounced back into positive territory, to a reading of 0.7% (from -0.4% in May) compared to the same period last year (Chart 2). The positive year-on-year metric was largely due to goods categories, which went from -2.3% in May to -0.2% in June. Excluding food and energy, prices were up 1% (0.8% in May). The sectors that faced the brunt of the lockdowns – clothing and transportation – had particularly strong rebounds.

Elsewhere, total investment in building construction increased 60.1% in May compared to April. Investment in residential and non-residential construction rose 57% and 66%, respectively. Gains were made across all components, especially in Ontario and Quebec. Although construction is rebounding, investment remains 16.5% below pre-pandemic levels.

Meanwhile, S&P reaffirmed Canada’s AAA rating with a stable outlook. The rating agency expects the Canadian economy to recover next year, citing the Government’s timely intervention to absorb the pandemic shock as a key reason. S&P’s view is in contrast to Fitch, which caught headlines in June when it downgraded Canada to AA+ from AAA citing Canada’s weak fiscal position.

In other news, the Bank of Canada (BoC) announced that since conditions in short-term funding markets have improved, it will reduce its Government of Canada T-bill purchases from 40% of tendered amounts to 20%. This will bring the purchases in line with pre-pandemic average levels. The BoC also announced a reduction in purchases (from 40% to 20%) for provincial short-term paper.

Elsewhere, provinces continue to reopen their economies. However, the recent resurgence in cases provide reason to remain cautious. Alberta is a good case in point, where reopenings have led to a sharp increase in new cases. Numbers are on the rise in other provinces as well. In response to the recent surge, British Columbia has already re-enacted some restrictions that were previously lifted. The future economic path is contingent on the pandemic path, therefore, keeping a lid on new cases is essential for recovery.

U.S: Upcoming Key Economic Releases

FOMC Rate Decision – July

Release Date: July 29

Previous: 0.00-0.25%

TD Forecast: 0.00-0.25%

Consensus: 0.00-0.25%

Fed officials have made clear that they will be making their forward guidance more dovish and outcome-based soon, most likely in conjunction with the formal adoption of an average inflation targeting (AIT) framework when the ongoing review is completed. We don’t expect those developments until after the September meeting, but Chairman Powell is likely to continue the process of prepping markets for changes when he speaks at his press conference on July 29. Changes to the FOMC statement are likely to be minimal this time. Nor will there be new projections for the economy or the funds rate—they will be updated at the September meeting.

U.S. Real GDP Growth – Q2 A

Release Date: July 30

Previous: -5.0%

TD Forecast: -31.0%

Consensus: -35.0%

Real GDP likely fell at a record pace in Q2 (forecast: -31.0% q/q AR), with a surge in May and June as the economy “reopened” only partly offsetting a plunge in April. The trajectory in Q2 implies a relatively high starting point for Q3, so the Q3 pace could be fairly strong, even with the latest high-frequency data showing slowing, but the net of Q2 and Q3 is likely to be a sizable decline. That implies a net increase in slack and downward pressure on inflation, although we don’t believe the trend in inflation is as weak as the deflation-like data for Q2.

U.S. Personal Income and Spending – June

Release Date: July 31

Previous: Spending: 8.2% m/m; Income: -4.2% m/m

TD Forecast: Sending: 5.5% m/m; Income: -0.8% m/m

Consensus: Spending: 5.5% m/m; Income: -0.8% m/m

The second-consecutive surge in retail sales is likely to be mirrored in the broader consumer spending series, although more recent high-frequency data suggest slowing, starting in late June (TD: +5.5%). The slowing is likely due to a fading of support from stimulus payments as well as fallout from rising COVID cases. Income likely fell in June, even with employment up strongly (TD: -0.8%). PCE inflation likely picked up on a m/m basis, but not by enough to offset recent weakening; the 12-month change in core prices probably held at 1.0%, which is down from 1.7% in Q1.

Canada: Upcoming Key Economic Releases

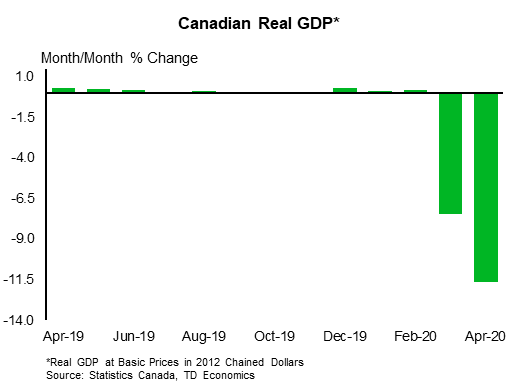

Canadian GDP – May

Release Date: July 31

Previous: -11.6%

TD Forecast: 3.9%

Consensus: 3.3%

TD looks for the Canadian economy to bounce back with a 3.9% m/m rebound following historic contractions in March and April. This is slightly above early estimates for a 3.0% increase which reflects the strength of data received over the last month but would still leave GDP ~14% below year-ago levels. We look for the service sector to drive the rebound, led by a strong performance in retail and food services, along with a sharp increase in real estate transactions. Goods-producing industries should fare slightly worse, with energy expected to weigh on the sector, although manufacturing and construction should see solid gains. A rebound of this size is an encouraging start to the recovery, especially with signs that growth accelerated in June, and would leave us on track to exceed BoC estimates for a 43% contraction in Q2.