{kind=link}

As US politicians squabble over the next fiscal stimulus bill and the country’s virus death toll ticks up again, markets may lean on the Federal Reserve next week for a quick fix. The Federal Open Market Committee (FOMC) meeting will undoubtedly be the most eagerly awaited event of the week. But second quarter GDP prints out of the United States and the euro area will not be far behind as the full extent of the economic shock from COVID-19 is laid bare. In the meantime, as tensions between the US and China continue to simmer, how much longer will traders be able to brush this risk under the carpet?Fed may not ease virus and stimulus jitters

Cracks have started to appear of late in America’s economic recovery from the pandemic as the resurgence of virus cases has forced several states to halt or even reverse the easing of lockdown restrictions. But the prospect of the US falling behind the recovery curve has merely taken the steam out of the incredible stock market rally rather than spark panic selling. That is because investors are certain that fiscal and monetary stimulus will be there to save the day once again.

However, this time round, a fresh round of stimulus may not arrive quite as quickly as markets are anticipating. Many are expecting the Fed to strengthen its forward guidance on how long the ultra-loose policy will stay in place when it announces its July FOMC decision on Wednesday. But after Chairman Powell famously said he was not “not even thinking about thinking about raising rates” at the last meeting, policymakers may not see the need to go beyond that statement at this point.

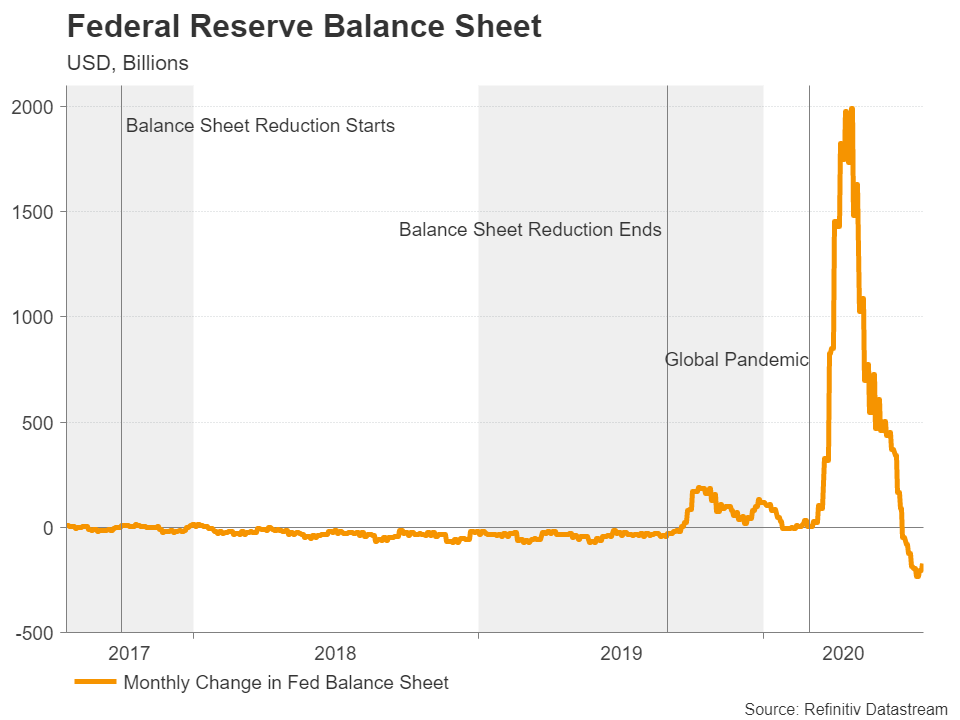

After all, as the virus situation is still unfolding in the US and it’s too early to get a good read on the state of the recovery, the Fed will be hesitant to give out more precise forward guidance so soon. At best, Powell will probably address concerns about the unexpected shrinkage of the Fed’s balance sheet in recent weeks as well as maybe fine tune some of the emergency lending facilities.

Besides, all it might take is some reassuring words from Powell to quash fears about the Fed scaling back its bond purchases too quickly. But it may not be quite so simple when it comes to Congress agreeing on another virus relief bill.

Aside from the fact that the Republicans and the Democrats are so far apart on the size and content of the next fiscal package, there are divisions within the Republican party, amid growing worries by some about the ballooning deficit. Thus, it’s quite possible that lawmakers will only agree to a stopgap bill while negotiations drag on.

US GDP and consumption data eyed

Disappointment from the Fed and Capitol Hill is the biggest threat to risk appetite in the near term, posing a downside danger for stocks and an upside one for the dollar. Although with its haven-like status diminishing slightly, the greenback may no longer get much of a boost from increased risk aversion. But for risk assets, the moves are likely to be exacerbated if any stimulus setback is complemented by weak data out of the US.

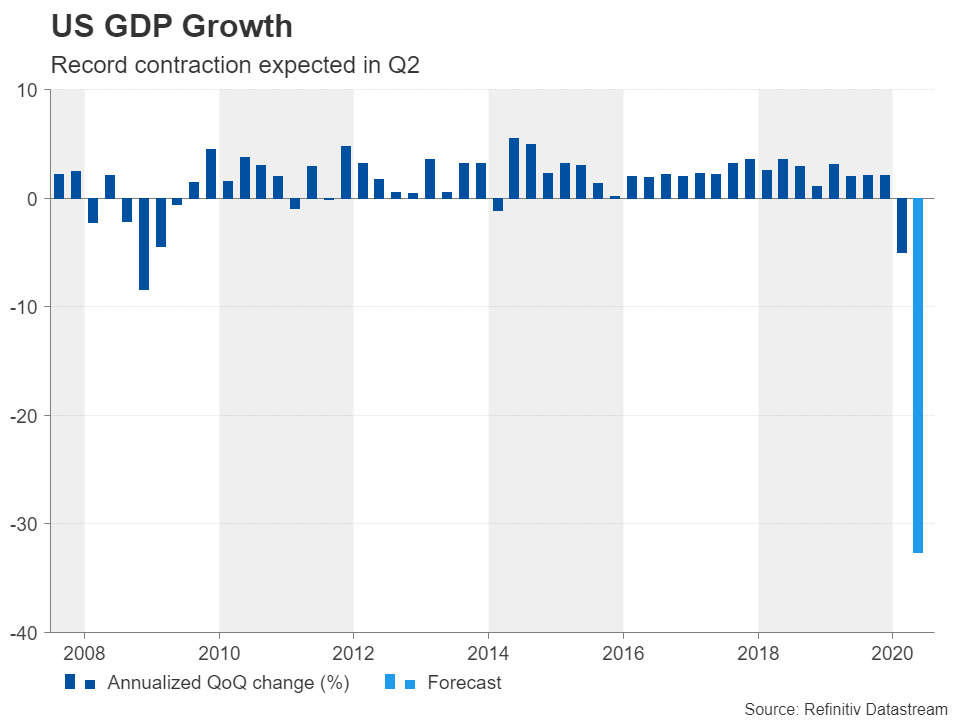

Durable goods orders out on Monday are forecast for a 6.5% monthly gain in June. The Conference Board’s closely watched consumer confidence gauge due on Tuesday may rattle investors if it shows worsening sentiment for July. Pending home sales will be the next major release on Wednesday, while on Thursday, all eyes will be on the advance GDP report for the second quarter. US economic output is expected to have plummeted by an annualized rate of 32.6%, in what would be the biggest quarterly contraction on record.

However, possibly softening this blow will be the June personal income and spending numbers on Friday. Personal consumption is forecast to have recovered by a further 5.8% month-on-month in June, which would suggest the virus escalation hasn’t significantly hurt spending just yet. Other data on Friday will include the core PCE price index and the Chicago PMI.

No letup in US-China frictions

Whichever way domestic developments out of the US sway markets in the coming days, the souring of relations with China is guaranteed to add a negative element. Tensions have been steadily intensifying in the last few months, with China’s handling of the coronavirus outbreak and tightening grip over Hong Kong adding to Washington’s long list of grievances with Beijing. The latest spat over China’s consulate in Houston, Texas, being used for spying on the US just made that list longer.

However, as far as markets are concerned, they only care about the ‘phase one’ trade deal and as long as that is left untouched, everything else will be seen as a sideshow and unlikely to have a huge impact. Except on the yuan and Chinese equities, that is. The Chinese currency and stocks are the most sensitive to geopolitical tensions between the two superpowers and further flare-ups could derail the yuan’s two-month long rebound versus the US dollar.

On the data front, traders will be observing Friday’s official manufacturing and non-manufacturing PMIs for clues on the speed of China’s economic recovery in July.

The Australian dollar will also be paying attention to China-related headlines, as well as to domestic quarterly inflation figures due on Wednesday. Australian building approvals might attract some interest too on Thursday, though lately, local indicators have played second fiddle to global risk sentiment when it comes to the aussie. Having said that, the currency is looking a little overvalued around $0.71 so it is vulnerable to a sharp correction if there was a market wobble.

Lockdowns likely crushed Eurozone GDP in Q2

Things are looking up for the Eurozone economy as, apart from some worries about Spain, the virus outbreak has been largely brought under control and business restrictions across the continent are gradually being lifted. And although there is still a long way to go for a full recovery, the fiscal package that was just agreed by EU leaders should go a long way in safeguarding the economic revival.

The brightening outlook has finally reawakened the euro bulls that had all but disappeared, sending the currency to 22-month highs versus the greenback. The euro’s appeal is being further augmented by America’s virus and political woes, the UK’s Brexit drama and soaring virus cases in major emerging markets such as India, Brazil and South Africa.

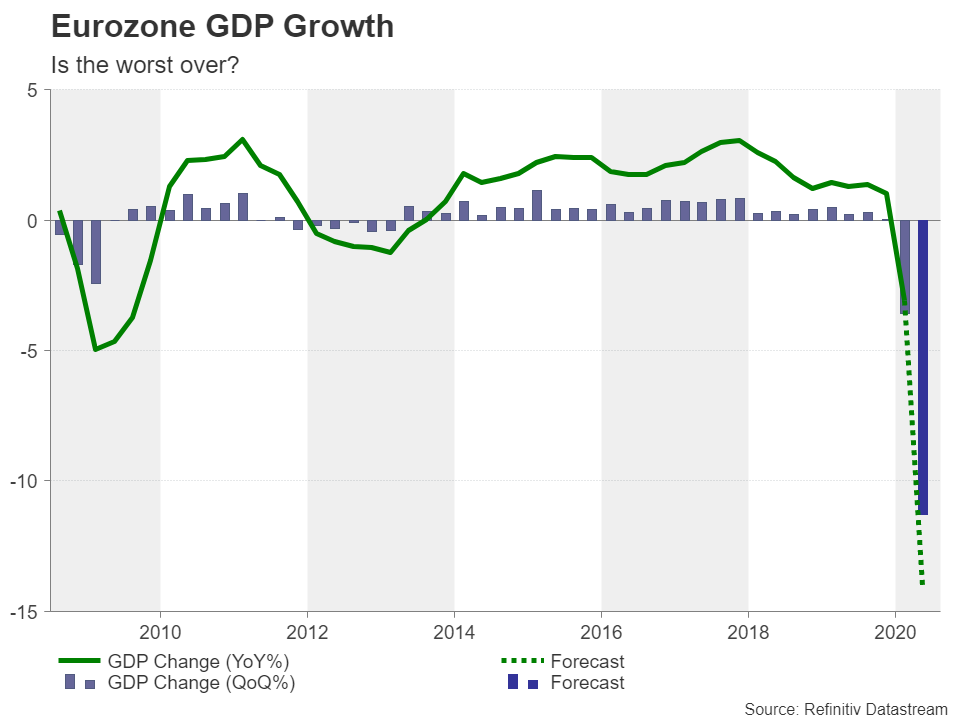

It’s highly unlikely therefore that the Eurozone’s preliminary GDP estimates for Q2 due on Friday will be able to stop the positive shift towards the euro even if the numbers are as catastrophic as the forecasts suggest. The euro area economy is expected to have dived by 11.3% over the quarter when much of the region was shut down, taking the year-on-year contraction down to 14.0%.

But whether the actual figures come in a few percentage points above or below the projections won’t matter much as the worst of the virus fallout is now over and Europe has a plan for a way forward. In addition to the GDP report, other data that might draw some attention for the euro next week are Monday’s Ifo business survey out of Germany, Thursday’s economic sentiment indicator and Friday’s flash inflation numbers.

Japanese and Canadian data also on the radar

Like the dollar, the safe-haven yen has been on the backfoot lately and like the US, the Japanese economy is in danger of seeing a slower recovery than many of its peers. Japan’s high exposure to global trade and domestic demand being undermined by the resurgence in new virus infections in Tokyo means the Bank of Japan will probably maintain an accommodative policy stance long after other central banks have exited theirs. Hence, the yen could have more downside on the way if this diverging outlook persists.

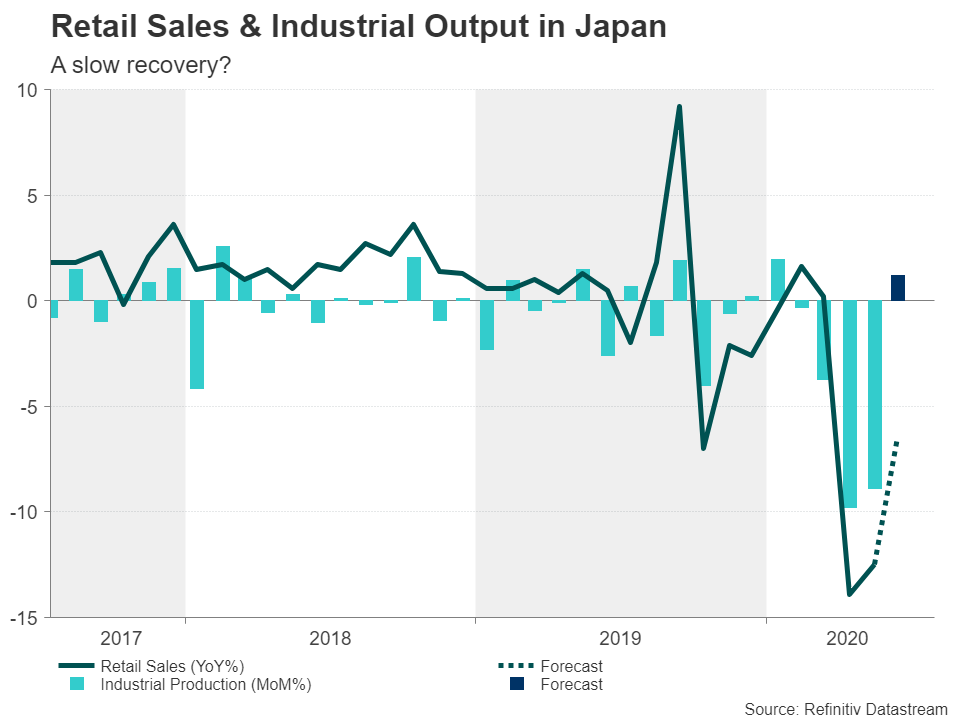

Next week’s releases are not expected to alter this picture. Retail sales figures due on Thursday are predicted to reveal a third straight month of annual decline in June, while the forecast for Friday’s preliminary industrial output reading is for a meagre rebound of 1.2% m/m.

In Canada, the monthly GDP print on Friday will be the main focus for the loonie. The Canadian dollar has not been able to benefit as much from the risk rally as its aussie and kiwi cousins have. Fears about the US recovery flattening out have been holding the loonie back as this could hamper the economic rebound in Canada too. A weak pickup in GDP growth in May would add to those worries.