{kind=link}

- Worries of a second infection wave kill the euphoria in markets

- S&P 500 loses almost 6%, dollar and yen shine again, commodity currencies crumble

- But risk sentiment back on the mend Friday, with most moves retracing a little

- Just a mild correction or start of something bigger? Daily virus numbers might decide that

Risk aversion returns with a vengeance

Just when it seems that all the bears have capitulated and that stock markets can’t bleed anymore, risk sentiment falls apart and equities record their worst day since March. The Dow Jones (-6.9%) was in the eye of the selling storm, though the benchmark S&P 500 (-5.9%) and the tech-heavy Nasdaq (-5.3%) didn’t fare much better.

The catalyst seems to have been the resurgence in US virus cases and hospitalizations. Even though the nationwide picture is still not that worrisome, there are large discrepancies between states, with the most populous ones – California, Texas, and Florida – displaying warning signs of a potential ‘second wave’. Most alarmingly, this latest spike probably doesn’t reflect the impact of the massive protests yet, which may have inflated the infectivity rate.

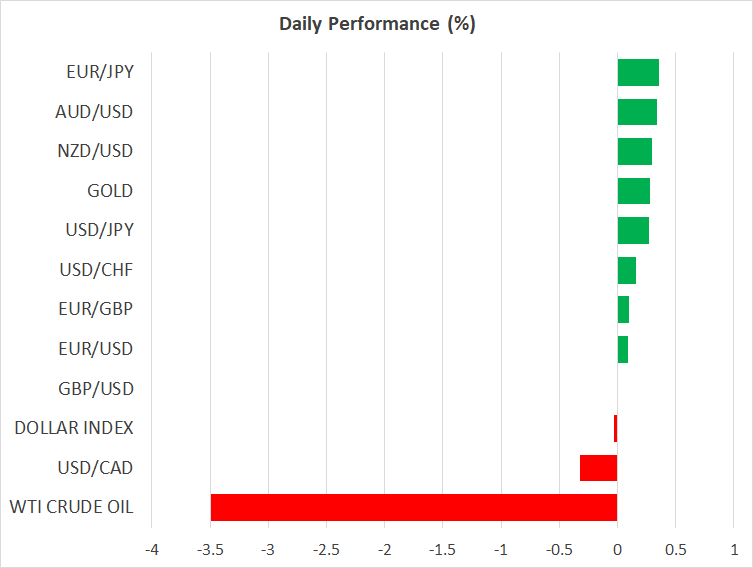

The stock market blues also spilled over into the FX arena, boosting defensive plays like the dollar and the yen while ravaging commodity-linked currencies and to a lesser extent the British pound, which has become highly sensitive to risk appetite. Indeed, it’s not just the pound. Almost every FX chart has become a byproduct of risk sentiment lately, in part because the dollar is now a haven-like asset and in part because interest rate differentials that used to drive the currency market have been virtually wiped out, leaving risk appetite as the dominant driver.

But risk tones stabilize – just a correction or more to come?

Nerves appear to have calmed on Friday though, with futures pointing to a modestly higher open on Wall Street and yesterday’s risk-averse FX moves retracing a little. The question now is whether this was just a long overdue correction in risk trades following a monster rally or whether the pullback has more room to run.

In a nutshell, that will probably hinge on how virus numbers evolve in the coming days. The recent euphoria in markets has been built on three key pillars: interest rates will remain low ‘forever’, fiscal discipline is ‘dead’ globally, and the global virus picture is improving. If any one of those falls apart, the risk trade might follow suit, and we got a small taste of that yesterday on mere concerns of a second infection wave.

As such, investors will likely turn their attention back to the daily virus numbers, particularly out of the US. The White House has made it clear that it won’t shut down the economy again even in case of a second wave, but ultimately, that decision comes down to state governors.

Dollar rebound clips gold’s wings

The odd one out yesterday was gold, which seemed unable to capitalize on the risk averse mood, possibly due to the sizeable gains in the dollar. Bullion contracts are generally priced in dollars, so when the greenback soars it becomes more expensive for investors using foreign currencies to buy gold, curbing demand for the metal.

In other words, the dollar and gold are typically inversely related, and even though that traditional correlation has weakened substantially over the past year and a half, it may have been what clipped gold’s wings yesterday.

Staying in the commodity sphere, oil prices are coming down quickly amid the realization that the pandemic may not be over. A second outbreak could dim the outlook for demand at a time when some supply seems to be coming back online following the surge in prices.