{kind=link}

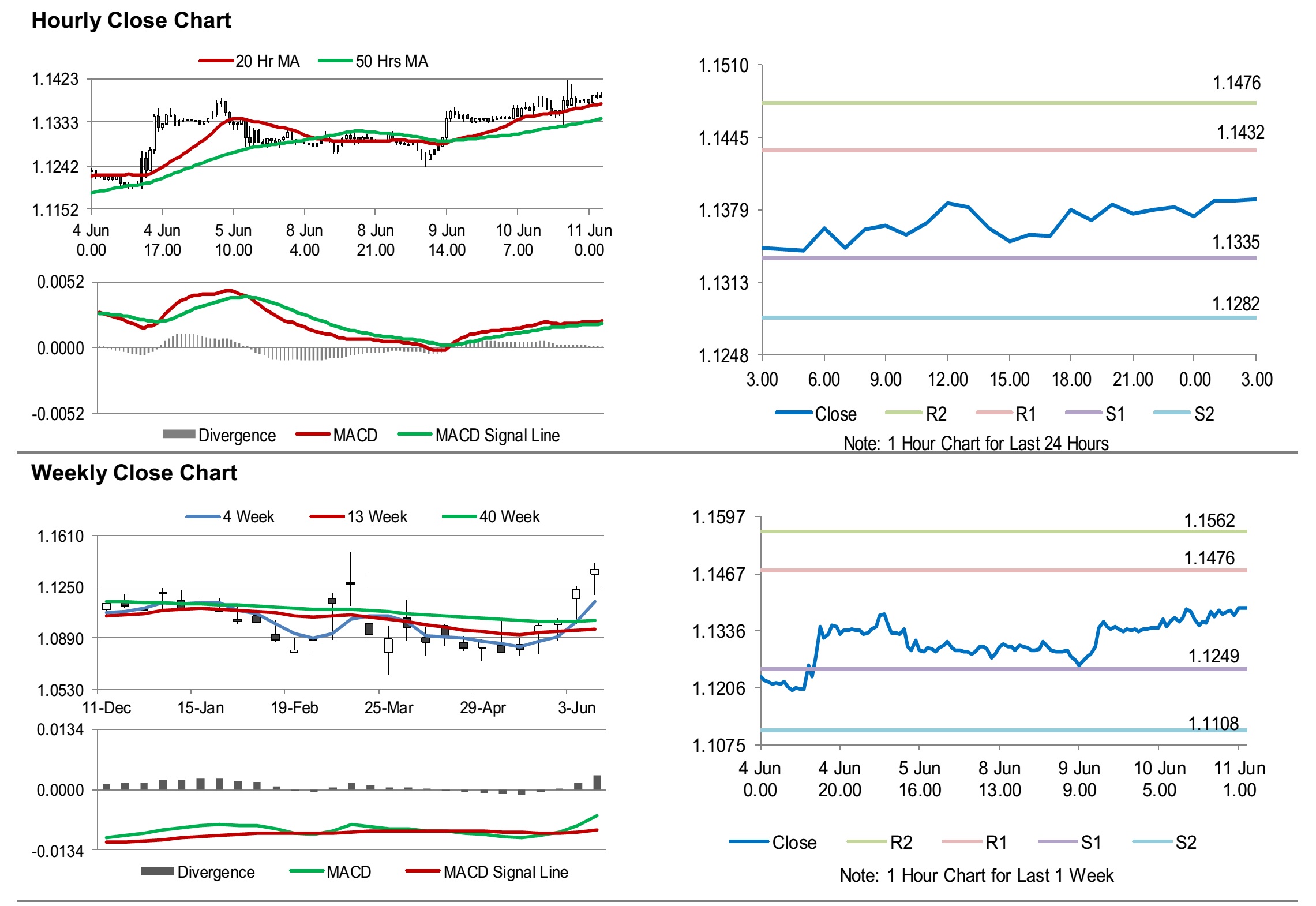

For the 24 hours to 23:00 GMT, the EUR rose 0.36% against the USD and closed at 1.1382.

The US dollar dropped against the euro, after the US Federal Reserve (Fed) signalled no hikes through 2022 and projected a more sluggish recovery.

In the US, the consumer price index fell 0.1% on a monthly basis in May, amid a continued decrease in oil prices and compared to a decline of 0.8% in the prior month. Meanwhile, the MBA mortgage applications jumped 9.3% in the week ended 5 June 2020, compared to a fall of 3.9% in the previous week. Moreover, budget deficit narrowed to $399.0 billion in May, more than market expectations and compared to a deficit of $738.0 billion in the previous month.

Separately, the Fed, in its interest rate decision, kept its key interest rate unchanged at 0.25%, as widely expected. Moreover, the central bank warned that the US economy will contract 6.5% in 2020 due to the coronavirus pandemic. Further, the Fed reiterated that it expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals. Also, the Fed signalled that it does not expect to lift its benchmark interest rate until 2023.

In the Asian session, at GMT0300, the pair is trading at 1.1389, with the EUR trading 0.06% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1335, and a fall through could take it to the next support level of 1.1282. The pair is expected to find its first resistance at 1.1432, and a rise through could take it to the next resistance level of 1.1476.

With no macroeconomic releases across the Euro-zone today, traders would look forward to the US producer price index for May and initial jobless claims, slated to release later today.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.