{kind=link}

- Fed funds rate held in current 0-0.25% range…

- …and expected to remain there through 2022

- 2020 GDP forecast (-6.5% y/y in Q4) slightly more pessimistic than RBC’s (-5%)

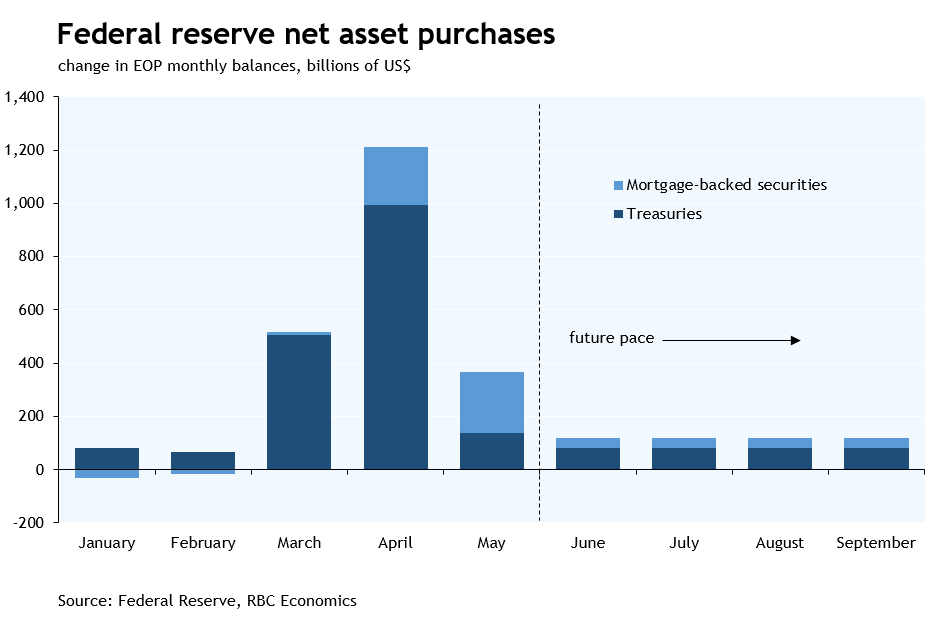

The Fed didn’t make any major policy changes today but gave a better idea of the extent of support it will provide in the months and years ahead. The committee’s dot plot (making a return after March’s hiatus) showed all but two FOMC members expect the fed funds rate will have to remain at its current near-zero level through the end of 2022. The Fed also gave more guidance on asset purchases, which have slowed down in the past several weeks after increasing to an unprecedented pace in late-March and early-April. Going forward, the Fed will continue to expand its Treasury holdings by roughly $80 billion per month, and agency mortgage-backed securities by approximately $40 billion per month. (That compares to monthly purchases of $45 billion and $40 billion, respectively, at the height of the Fed’s ‘QE3’ program back in 2013.) There was no guidance on how long those asset purchases (which can be scaled up if needed) will continue, though discussions on forward guidance (and potentially even yield curve control) will continue at upcoming meetings.

The need for this extensive support was underlined by the Fed’s updated economic projections. The median forecast looks for a 6.5% decline (on a Q4/Q4 basis) in 2020 GDP followed by a 5% recovery in 2021 (also Q4/Q4) that would still leave the economy operating below its end of 2019 level. RBC’s forecast is slightly less pessimistic this year (-5% Q4/Q4) but anticipates a similar 5% rebound in 2021. The unemployment rate (which has understated labour market slack during this crisis) is projected to remain elevated at 9.3% in Q4/20 before falling to 6.5% at the end of next year (it was 3.5% at the end of last year). Economic slack is expected to keep core PCE inflation below the Fed’s 2% objective through the end of 2022. The Fed noted significant uncertainty around these projections, and reiterated that it will use the full range of its tools to support the economy as needed.

US Treasury yields have hovered around record lows in the past two months, and the combination of ongoing asset purchases (helping to absorb some of the increased issuance to fund fiscal programs) and indications that fed funds will be held close to zero in the coming years should keep borrowing costs low. The Fed also has a number of programs in place (or about to be rolled out) to supply liquidity to key markets and ensure credit continues to flow to borrowers. Uptake of those programs will contribute to ongoing balance sheet growth (Fed assets are already a record 1/3 of GDP). Substantial monetary and fiscal support is laying the groundwork for an economic recovery over the second half of the year as health restrictions continue to be eased. However, as the Fed’s projections suggest, a full economic rebound will take years.