{kind=link}

Executive Summary

In the second report in a two-part series, we analyze which domestic industries could potentially benefit from increased production if industries re-orient their supply chains back toward domestic vendors. Our analysis shows that the industries that could potentially benefit the most include leather & apparel, electrical equipment, textiles, computers & electronics and plastics & rubber products.

What Do We Mean by “Supply Chains”?

In Part I of this series, we analyzed how different industries could be affected if they were to reorient their supply chains back toward the configurations that prevailed twenty years ago. We found that some industries, such as aircraft & aerospace, leather & apparel, machinery, auto & auto parts and electrical equipment, have relied increasingly on foreign vendors to supply their inputs since the late 1990s. Therefore, these industries would potentially face some of the largest adjustments if they were to re-orient their supply chains away from foreign vendors and back toward domestic suppliers. But we also noted in Part I that the domestic suppliers of these inputs could benefit via higher demand if supply chains were brought back onshore. So which domestic industries could potentially enjoy the biggest windfall from a re-orientation of supply chains?

Before answering that question, we should first clarify what we mean by “supply chains.” Demand for goods and services can arise from two sources: as inputs into the production of other goods and services and as final demand. For example, consider a firm that manufactures wiper blades for automobiles. Automakers purchase wiper blades to install on the automobiles that they sell to consumers. In this case, wiper blades are an input into the production of automobiles. But individuals can also purchase wiper blades to replace the old ones on cars they currently own. In this case, the wiper blades are purchased on a final basis.

Over the past twenty years, automakers may have shifted their purchases of wiper blades from domestic producers to foreign producers. Retailers that sell wiper blades directly to consumers may also have shifted their purchases from domestic vendors to foreign vendors. For the purposes of this report, we consider only the first channel. That is, we analyze “supply chains” in the narrow sense of the term: the use of goods and services only as inputs into the production of other goods and services. We do this to make the methodology in this report consistent with the analysis we undertook in Part I. We will postpone consideration of changes in final demand for goods and services to another time.

Also, it is also important to note that supply chain re-orientation will not just affect the dynamic between industries, but also within industries. Many companies import products from within their own industry in order to assemble or refine them for final sale. For instance, some auto parts are imported as inputs for other industries, but the majority remain within the auto industry, such as wiper blades in the example above.

Which Industries Could Benefit from Supply Chain Re-Orientation?

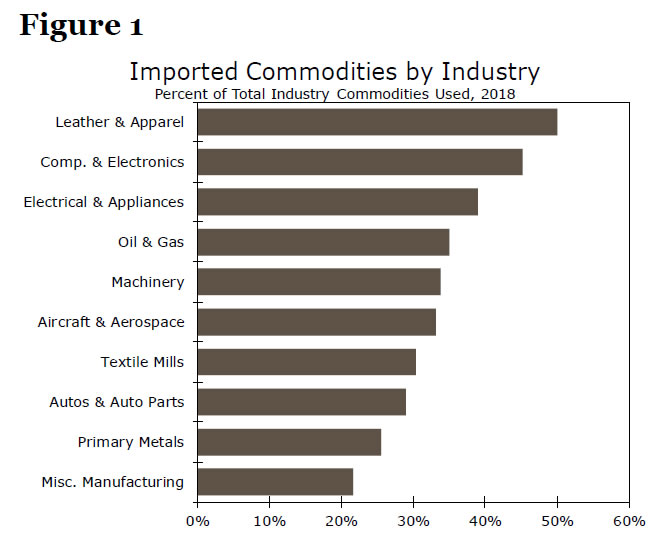

So which domestic industries compete most with foreign vendors as suppliers of inputs? Figure 1 shows that 50% of apparel & leather inputs were imported in 2018, and 45% of inputs of computer & electronic products came from abroad. Roughly 40% of electrical equipment inputs were imported. The industries shown in Figure 1 all have imported input ratios that are well above the average of only 9%. As we noted in Part I, the overall ratio is dragged down by inputs of services, which tend not to be imported.

For the purposes of this report, however, we are more interested in changes in import ratios since 1997 than we are in the absolute levels of the ratios in 2018. A domestic industry that had a high import ratio in 2018 would not likely experience a marked increase in production from a reorientation of supply chains if its import ratio has not changed much over the past twenty years. Rather, the domestic industries that would enjoy the largest increases in production from a reorientation of supply chains are those that have experienced a significant increase in foreign competition over the past 20 years.

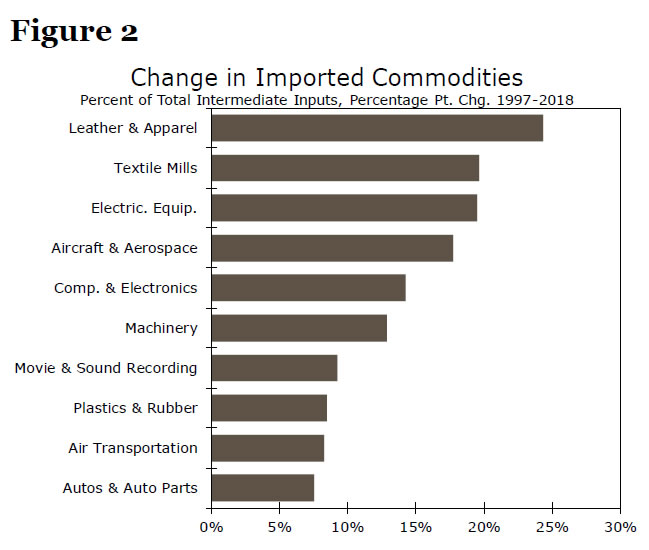

Many of the industries that had high import ratios in 2018 (Figure 1) have also experienced large increases in their respective ratios over the past twenty years (Figure 2). For example, the apparel & leather industry has seen its ratio nearly double since 1997, an increase of more than 24 percentage points. In short, domestic producers of apparel & leather goods face significantly more competition today from foreign suppliers than they did twenty years ago. Producers of textiles have had to contend with a 20 percentage point increase in the amount of imported textile products that American industries use, and producers of electrical equipment have also experienced a 20 percentage point rise in their import ratio over the past twenty years. Domestic producers in these industries could potentially enjoy marked increases in output if supply chains in the United States are re-oriented back to their 1997 configurations.

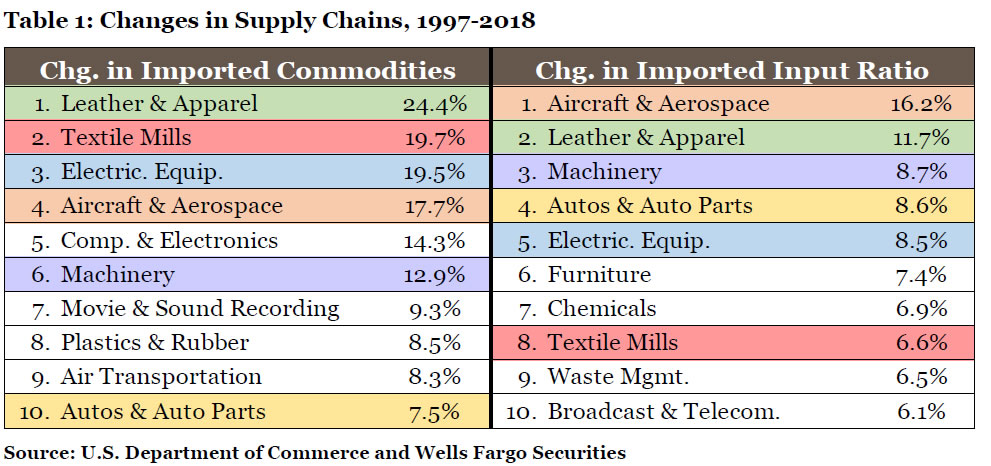

Interestingly, many of the domestic industries shown in Figure 2 would also face some significant adjustments in their own supply chains because they have also turned increasingly to foreign suppliers over the past twenty years, which was the subject of Part I. The left column of Table 1 lists the ten industries that are shown in Figure 2. The right column lists the ten industries that were shown in Figure 3 of Part I (i.e., the industries that have engineered the most significant increases over the past twenty years in the amounts of imported inputs that they use).

Six industries that would face the most adjustment in re-orienting their own supply chains (right column of Table 1) could also benefit the most from a general re-orientation of supply chains (left column of Table 1). We used wiper blades, which is part of the auto & auto parts industry, as an example previously. If supply chains returned to their 1997 configurations, then the auto & auto parts industry would need to reduce its own imported input ratio by 7.5 percentage points, which would be a fairly significant adjustment. But the general re-orientation of supply chains means that the use of imported inputs of autos & auto parts would also decline by 8.6 percentage points. Perhaps industries, such as auto & auto parts, which have faced the most significant increases in foreign competition over the past two decades have also turned to foreign suppliers of inputs in an effort to reduce their own input costs.

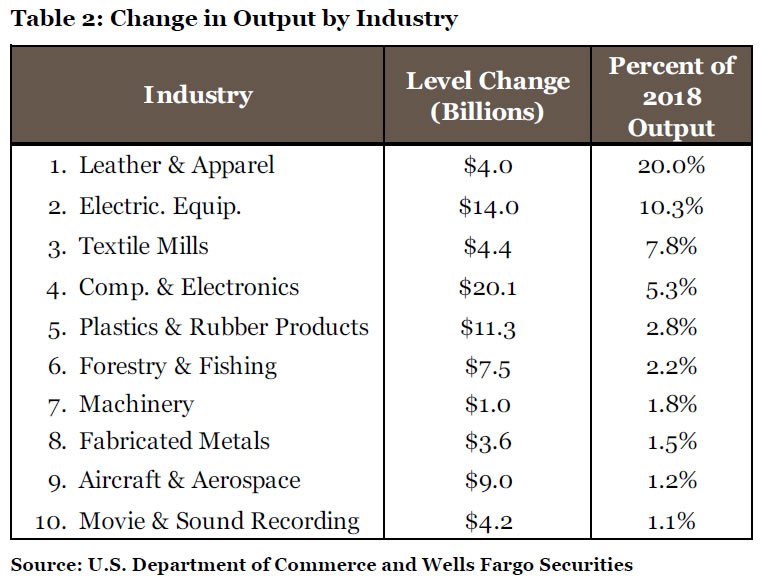

So how much could domestic producers of good and services gain if all American industries reorient their supply chains? We assume that industries revert from the supply chain configurations that prevailed in 2018 back to the configurations of 1997. For example, we assume that the amount of imported inputs of apparel & leather products used in domestic production reverts from 50% (the ratio in 2018) to 26% (the ratio in 1997). We make similar calculations for all the other industries that are based on their own import ratios, and list the results for the ten most affected industries in Table 2.

The top line of Table 2 shows that output in the leather & apparel industry in the United States could potentially rise $8 billion. Although this potential increase is not very large relative to some of the other changes shown in the middle column of Table 2, American production of leather & apparel products totaled only $20 billion in 2018. In other words, this industry could potentially experience a 40% increase in its production if U.S. firms turn to domestic suppliers of leather & apparel products. Other domestic industries that could potentially enjoy double-digit increases in output from a re-orientation of supply chains are electrical equipment, textiles, computers & electronics, and plastics & rubber products.

As we noted in Part I, individual industries could realize meaningful increases in production from supply chain re-orientation, but the macro effect on the $21 trillion U.S. economy likely would not be very significant. The service sector accounts for nearly 70% of value added in the economy and, as noted previously, services tend not to be imported. Furthermore, to the extent that businesses use imported inputs because of lower costs, a re-orientation of supply chains to domestic producers could potentially raise input costs, which would reduce the overall benefit to the macro U.S. economy.