{kind=link}

For the 24 hours to 23:00 GMT, the EUR rose 0.41% against the USD and closed at 1.1341.

On the macro front, Euro-zone’s gross domestic product (GDP) declined 3.6% on a quarterly basis in the first quarter of 2020, recording its biggest fall since 1995 and compared to a rise of 0.1% in the previous quarter. The preliminary figures had recorded a fall of 3.8%. Separately, Germany’s trade surplus narrowed to €3.2 billion in April, more than market expectations for a surplus of €10.0 billion and compared to a surplus of €12.8 billion in the prior month. Additionally, the nation’s seasonally adjusted current account surplus narrowed to €7.7 billion in April, compared to a revised surplus of €25.6 billion in the previous month.

In the US, the NFIB business optimism index unexpectedly climbed to 94.4 in May, defying market expectations for a drop to a level of 86.0 and compared to a reading of 90.9 in the previous month. Moreover, the JOLTS job openings dropped to 5.04 million in April, less than market expectations for a drop to a level of 5.00 million and compared to a revised reading of 6.01 million in the earlier month. Meanwhile, the IBD/TIPP economic optimism dropped to 47.0 in June, compared to a level of 49.7 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1344, with the EUR trading marginally higher against the USD from yesterday’s close.

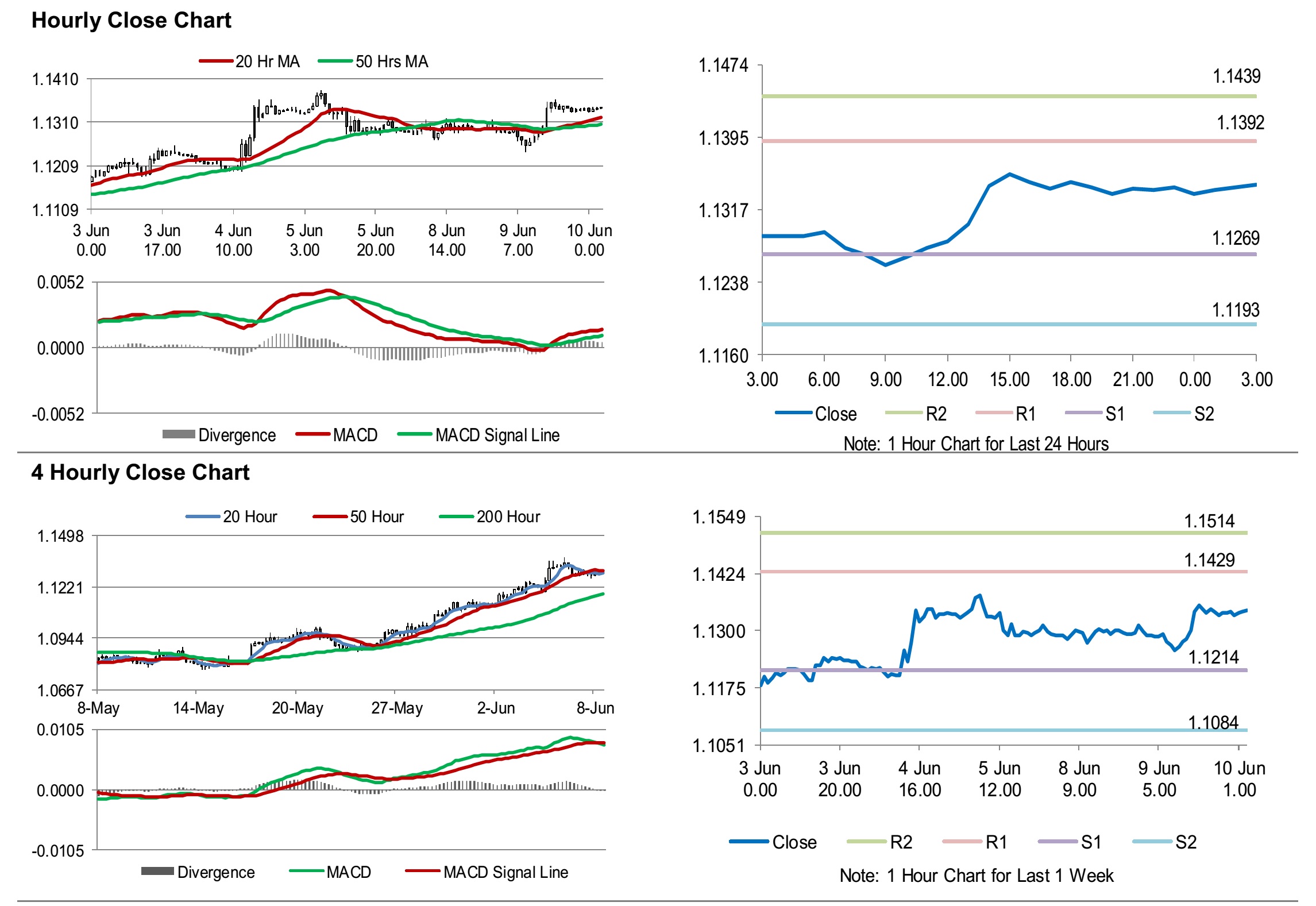

The pair is expected to find support at 1.1269, and a fall through could take it to the next support level of 1.1193. The pair is expected to find its first resistance at 1.1392, and a rise through could take it to the next resistance level of 1.1439.

With no macroeconomic releases across the Euro-zone today, traders would look forward to the US consumer price index for May and the MBA mortgage applications along with the Federal Reserve’s interest rate decision, slated to release later today.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.