{kind=link}

- Overnight rate held at “effective lower bound” of 0.25%

- BoC reducing frequency of some liquidity-providing operations

- QE will continue until recovery is “well underway”

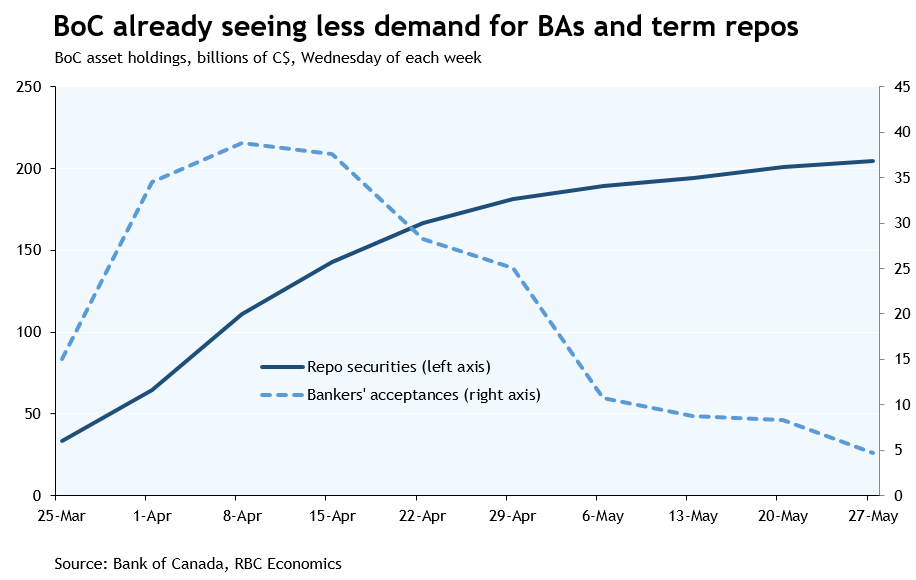

Today is Governor Macklem’s first day on the job, though this morning’s policy statement is a hold-over from the Poloz era—a note accompanying the statement said Macklem participated in Governing Council’s deliberations as an observer and endorsed its policy decisions. Those decisions included leaving the overnight rate at the “effective lower bound” of 0.25% and reducing the frequency of some of the central bank’s liquidity-providing programs. The latter is a positive development as it signals the BoC is comfortable enough with market functioning to scale back some of the support put in place since March. Market participants were already doing that on their own, though, with now bi-weekly bankers’ acceptance purchases having been unused in the past month while uptake of now weekly term repos has also slowed. Even so, the BoC is committing to continuing with those programs (at their new frequency) until the end of October.

While the BoC has also framed its bond buying (QE) program as liquidity support, the central bank reiterated its commitment to continue large scale asset purchases “until the economic recovery is well underway.” As the BoC shift its focus from crisis management to “supporting the resumption of growth in output and employment,” we think QE will be key to its stimulus efforts. Provincial and corporate bond purchase programs are scheduled to last a year, and it’s hard to see the BoC easing up on its $5 billion weekly GoC purchases over that time frame. Those purchases will help offset upward pressure on borrowing costs due to higher debt issuance and keep interest rates low for individuals and businesses as well as the government. As the economic outlook—and required stimulus—becomes clearer, we might get some more detailed guidance on the minimum duration and size of the bank’s GoC purchase program

On the economic outlook, the bank said incoming data suggest the economic impact of the COVID-19 pandemic appears to have peaked but that the shape of the recovery remains highly uncertain and is likely to be “protracted and uneven” globally. Canada has avoided the more severe downturn scenarios laid out in the BoC’s April MPR though a 10-20% decline in Q2 GDP is still expected (our own forecast is on the more optimistic end of that range). The outlook for the second half of the year is “heavily clouded” but growth is expected to resume in Q3—indeed, economic activity already appears to be picking up as restrictions ease. The speed of that recovery, and the extent to which the economy continues to operate below full capacity, will be key to the inflation outlook. At this point, all the BoC could say is that temporary factors (including a sharp drop in gasoline prices) will keep inflation below its 1-3% target band in the near-term. Recent comments suggest the BoC is more concerned about underlying inflation remaining below its target than above, and we agree that an extended period of low inflation is a greater risk than excessive inflation. That should keep the BoC’s foot to the floor with low interest rates and asset purchases in the early stages of the Macklem era.