{kind=link}

The Canadian dollar may show fresh volatility on Wednesday after the Bank of Canada’s new chief holds his first policy meeting, with the rate announcement scheduled to be released at 14:00 GMT. Interest rates are expected to stay steady, while additional lending through corporate bond purchases cannot be excluded if the central bank wants to help more amid the uncertainty around the COVID-19 and the elevated domestic risks. Yet, what could attract a greater attention, and hence move the loonie, is the central bank’s forward guidance as markets are looking for clues on where monetary policy may be going next under the new governor.

Why negative rates may not be an option yet

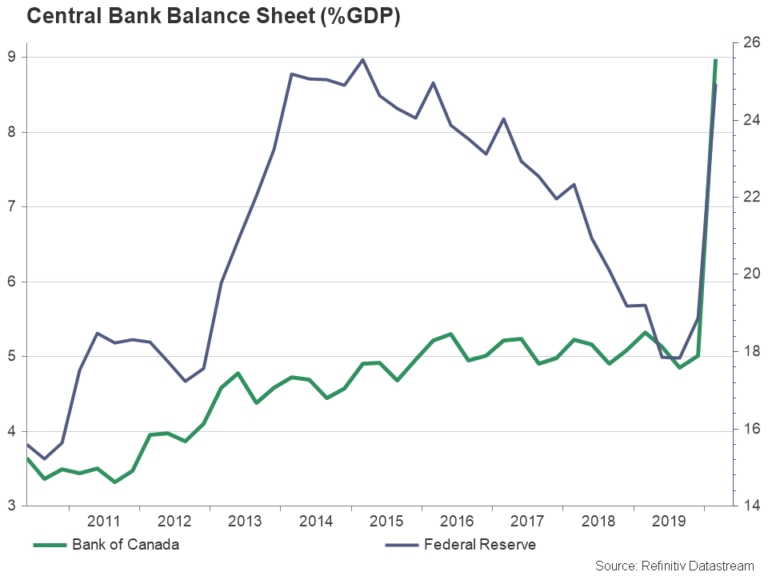

In his last speech as Bank of Canada’s head, Stephen Poloz, who spent his seven-year term putting the economy back to its feet following the previous economic recession, said that additional stimulus is necessary to continue the rebuilding process. Previously, the Bank was forced to slash its benchmark interest rate to 0.25% from the pre-virus level of 1.75% and push up asset purchases particularly government bonds by a massive amount – similar at the Fed’s scale in terms of percent of GDP– to ensure that there is enough liquidity to serve the financial system.

Markets are now wondering if the central bank will deliver similar substantial stimulus packages in the foreseeable future to further aid the economy or whether it will adopt a wait-and-see approach as lockdown measures are easing and Tiff Macklem takes the BoC’s lead. The certain thing is that the virus saga has not been solved yet and fears of a second wave of infections will always keep some pressure on governments and central banks and therefore weigh on traders’ sentiment until an effective vaccine is finally invented. Therefore, Macklem, Poloz’s successor, will likely say that plans for additional support may remain on the cards, but at the current reopening phase he may keep the powder dry in the main policy tools, which are at their limits, and see how the gradual reopening will play out before the board commits to inject more liquidity.

That is also the reason why the Bank of Canada did not rule out negative interest rates but admitted that the benchmark rate could be driven below zero only in extreme conditions and if fiscal policy is not used. Thinking rationally, Canada could handle negative rates better than other key economies such as the EU and Japan at some degree. Canadian banks don’t face reserve requirements and the system operates under few reserves, while unlike the US, where the five biggest banks hold around 35% of the market share, this more than doubles to 89% for the oligopolistic Canadian banking sector. Therefore, it can be argued that the banks could deal with extra charges more efficiently. On the negative side though, Canadian banks are heavily dependent on foreign capital which could immediately be withdrawn if foreign investors face negative rates. Therefore, the BoC is highly likely to stand pat on borrowing costs at least till the end of this year or until the data suggest otherwise. Besides, in April’s policy statement, the effective lower bound below which rates cannot go lower as investors would remove funds, was mentioned at 0.25% compared to -0.5% previously, adding more evidence that policymakers may not adjust interest rates lower in the short-term.

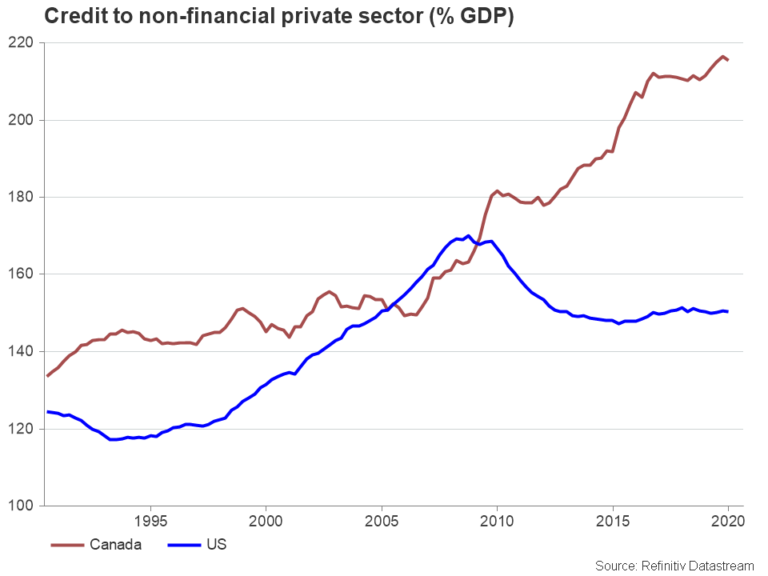

As regards asset purchases though, the BoC could buy new corporate bonds to finance business activities which continue to operate at a limited capacity, reducing the risk of defaults and higher unemployment. The boost in oil prices and the slight improvement in the small business sentiment in May indicated by the Canadian Federation of Independent Business is an encouraging sign, however the bias is still tilted to the downside in terms of layoffs and investments especially in the housing sector. This environment suggests further support as long as the spread between corporate and government bond yields remails positive. It is also worth noting that for this support to work, consumption needs to advance to push inflation higher. Otherwise, the country could face a debt deflation crisis if the Canadian business sector, which is among the most indebted in the world, could reduce prices to attract demand, forcing some companies to leave the market as they would not be able to survive with less income.

Where next for the loonie?

Turning to FX markets, traders are well aware that central banks could do anything if necessary, to reinforce a bridge to recovery, so the policy decision itself may not affect the loonie much. Nevertheless, since the BoC is now moving to new hands, markets would pay a greater attention to Macklem’s forward guidance to clarify whether monetary policy could take a different direction in the coming years. Although the virus situation hints that monetary strategy is currently a one-way path regardless of who is governor, any discouraging message about the economy’s outlook from Macklem and supportive comments on negative rates could eat into some of the loonie’s recent gains and vice versa.

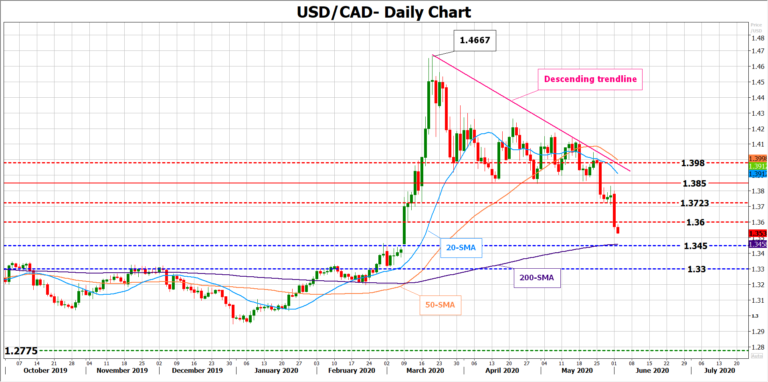

Looking at USD/CAD, from a technical perspective the pair has breached the 1.3600 support level on Monday and should that mark turn resistance, the pair could furher lose ground to test the 1.3445-1.3400 area where the 200-day simple moving average is currently hovering. Benenath the latter, the 1.3300 barrier could be the next target.

Alternatively, a break above 1.3600 may stall near 1.3723, while higher the 1.3850 number could prove a tougher obstacle. If it fails to hold, the price could move towards the 20-day SMA and the descending trendline.