{kind=link}

The European Commission today unveiled its long-awaited recovery fund (‘Next Generation EU’) and revised EU budget, amounting to EUR1.85trn in total (11.2% of EU GDP). Here we summarise the key things to note from today’s proposal.

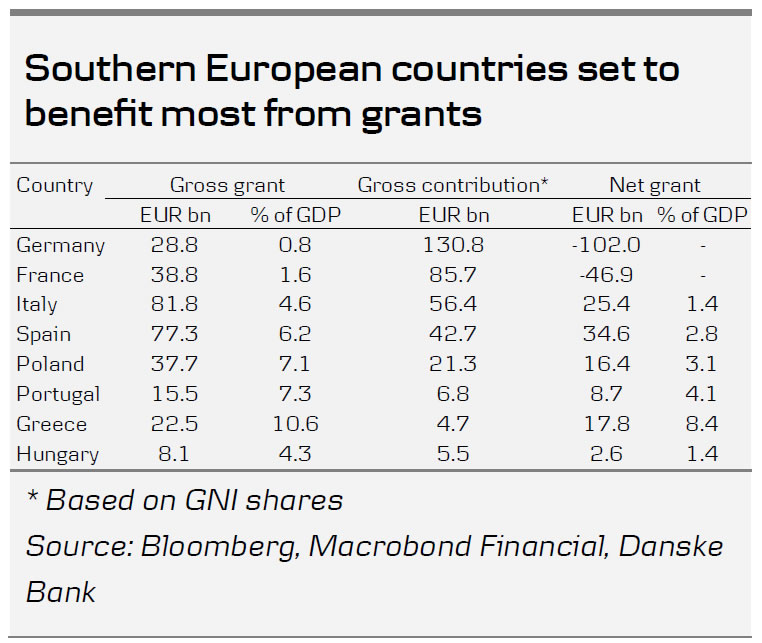

- Size of recovery fund: EUR500bn in grants + EUR250bn in loans (i.e. 66/33% split). The Commission plans to raise the money by borrowing in the financial markets. Overall, the amounts in grants for the hard hit countries (see table) are reasonably sizeable, considering that the money will be spent over a relatively short time span and is due to be repaid only some time in 2028-58.

- Structure of recovery fund: There are three pillars: (1) a Recovery and Resilience tool to fund public investment through grants and loans, (2) a private investment pillar, including creating a tool to invest in EU strategic supply chains and strengthen the InvestEU programme, and (3) a new health programme focusing on crisis-dealing capacity and cross-border health collaboration.

- MFF 2021-27 (EU budget): the EUR1.100trn proposal is below the level originally suggest by the Commission (EUR1.135trn) but higher than a compromise plan put forward in February by Council President Charles Michel (EUR1.095trn). It is likely the still-limited size is a nod towards the frugal countries.

- Next steps: Overall, we view this as an ambitious proposal and the loan element on top of EUR500bn of grants even exceeds the Franco-German proposal. The uncertainty is now where the proposal will land. Negotiations behind the scenes are due to start in the coming days and we expect markets to look out for comments on the proposal from different heads of state. We look to the 18-19 June EU council meeting for potential approval. The ‘frugal four’ countries have recently signalled their openness to negotiations (i.e. accepting the grant element of the recovery fund versus ensuring their rebates in the EU budget). Some of the recovery fund money might flow as early as H2 20 but we expect most of the fiscal boost to investments to materialise only in early 2021.

- How will the money be repaid? The money is not due for repayment before 2028 but as long as the recovery fund remains a temporary instrument, it is set to lead to higher EU budget contributions in the future (see table for net grants). To avoid having to ask member states for significantly higher budget contributions, the Commission is also exploring new revenue streams, i.e. a tax on large corporations, extending carbon market certificates to other sectors such as shipping and aviation, a carbon border tax, a new EU tax on plastic waste and a digital tax.

Overall, we believe the recovery fund proposal is a strong signal from the Commission and European leaders (if confirmed) of support for the European project. While the exact value of the grants is still difficult to assess (due to the repayment schedule being unknown), we remain cautiously optimistic on the periphery. With the ECB expected to step up its pandemic emergency purchase programme (PEPP) next week, we remain constructive on peripheral spreads. Looking ahead, this does not solve the matter of high debt levels but it should help European economies near term, reducing the risk of an asymmetric recovery.