{kind=link}

For the 24 hours to 23:00 GMT, the EUR rose 0.79% against the USD and closed at 1.0982.

On the macro front, Germany’s GfK consumer confidence survey climbed to -18.9 in June, in line with market expectations and compared to a revised reading of -23.1 in the previous month.

In the US, the Chicago Fed National Activity Index dropped to -16.7 in April, compared to a revised reading of -5.0 in the previous month. Additionally, the consumer confidence advanced to 86.6 in May, compared to a revised level of 85.7 in the earlier month. Moreover, the Dallas Fed manufacturing business index increased to -49.2 in May, compared to a revised reading of -74.0 in the prior month. Furthermore, new home sales unexpectedly advanced 0.6% on a monthly basis in April, compared to a revised drop of 13.7% in the previous month. Meanwhile, the housing price index rose 0.1% on a monthly basis in March, less than market expectations for an advance of 0.3% and compared to revised rise of 0.8% in the prior month.

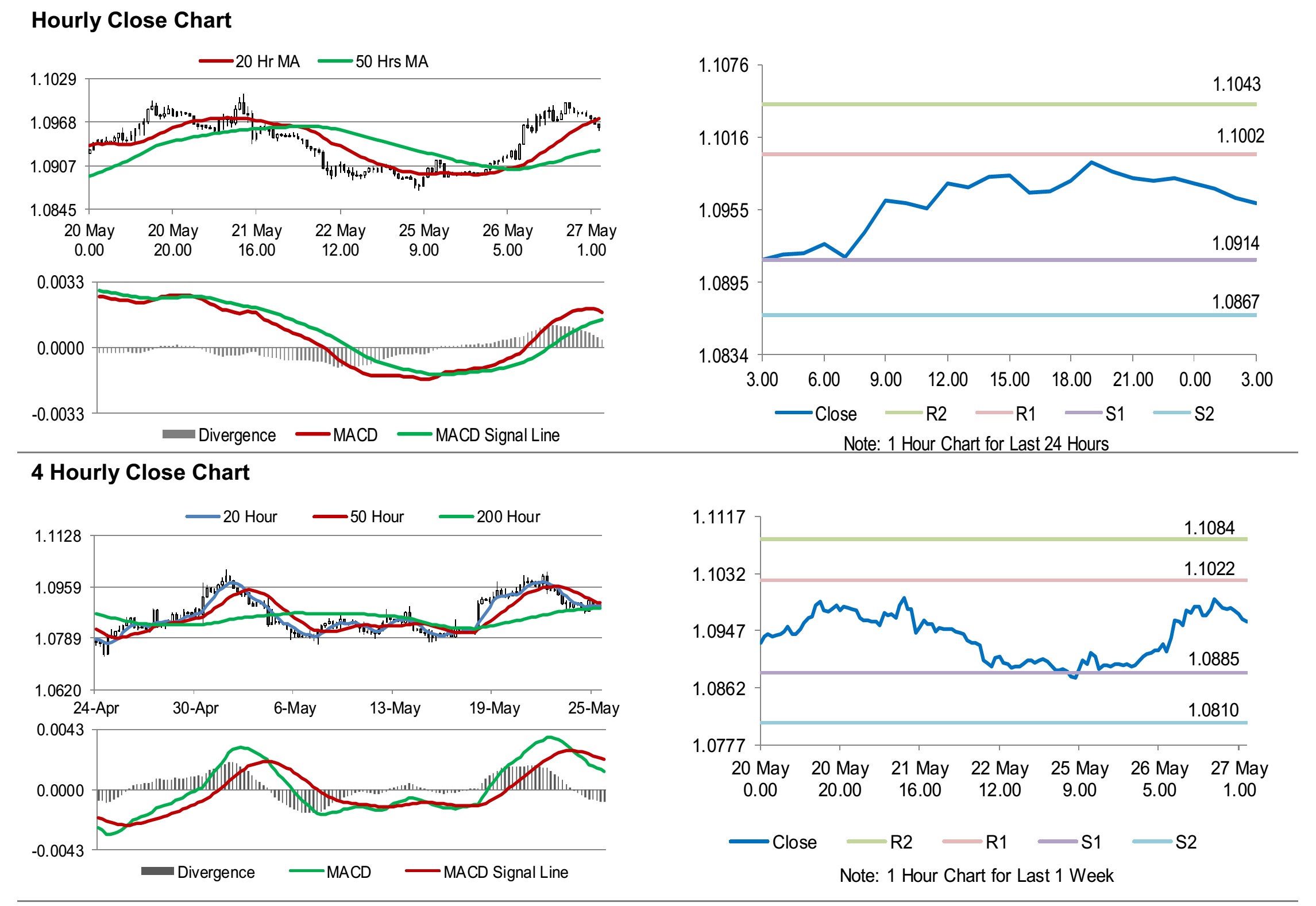

In the Asian session, at GMT0300, the pair is trading at 1.0961, with the EUR trading 0.19% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.0914, and a fall through could take it to the next support level of 1.0867. The pair is expected to find its first resistance at 1.1002, and a rise through could take it to the next resistance level of 1.1043.

Moving ahead, traders would keep a watch on European Central Bank President Lagarde’s speech, slated to release in a few hours. Later in the day, the Richmond Fed manufacturing index for May along with the MBA mortgage applications and Fed’s Beige Book report, would keep investors on their toes.

The currency pair is trading below its 20 Hr moving average and trading above its 50 Hr moving average.