{kind=link}

European stocks and US index futures were trading back in the positive territory this morning after doubts over the prospects of a Covid-19 vaccine (one of the main reasons said to be behind Monday’s big rally) caused a late sell-off on Wall Street on Tuesday. In case you missed it, a STAT expert report poured cold water on Moderna’s vaccine trial, suggesting “there’s no way to know how impressive, or not, the vaccine may be” and that “we don’t know if the antibodies are durable”.

However, the larger driver behind equity markets have been optimism surrounding easing of lockdown measures, as well as the recent actions of governments and central banks, especially the latter’s promise of doing whatever it takes to support their respective economies.

Still, Tuesday’s late sell-off serves as a reminder that these markets are still very much headline-driven and you will see sharp moves on any future vaccine news. Investors know that a vaccine could be the best solution to mitigate risks of future covid-19 related shutdowns, so the market’s wild reaction makes some if not total sense.

FX update

Dollar Index was down for the third day as European currencies finally joined the Aussie in staging a relief this week. Fed’s Jay Powell reiterated yesterday that the Fed is ready to basically do whatever is needed to help the US economy – this explains the greenback’s weakness. The latter is also undermined by reduced haven demand as equity markets push higher (see above)

GBP/USD was holding key support circa 1.2225 following this week’s rally. Earlier news that UK CPI fell to a 4-year low of 0.8% has been largely shrugged off. The cable is also supported thanks to weakness for US dollar

EUR/USD has extended its gains for the fourth day. A couple of positive developments has helped to fuel the rally in this and other euro crosses recently, including an upbeat German ZEW economic sentiment reading, which was released yesterday, and as European leaders proposed a €500 billion relief package. Meanwhile the ECB President Christine Lagarde has indicated that QE will continue despite the German’s constitutional court ruling

Commodities update

Gold continues to edge higher thanks to ongoing central bank bond purchases, which is helping to depress yields, while the weakness in the dollar is also helping more directly

Crude oil is holding steady too on hopes demand will recover with lockdown measures being lifted in parts of the world and on OPEC+ supply cuts. It remains to be seen how much further crude will recover given that it is likely to face some resistance amid concerns over weakness of the rebound in demand

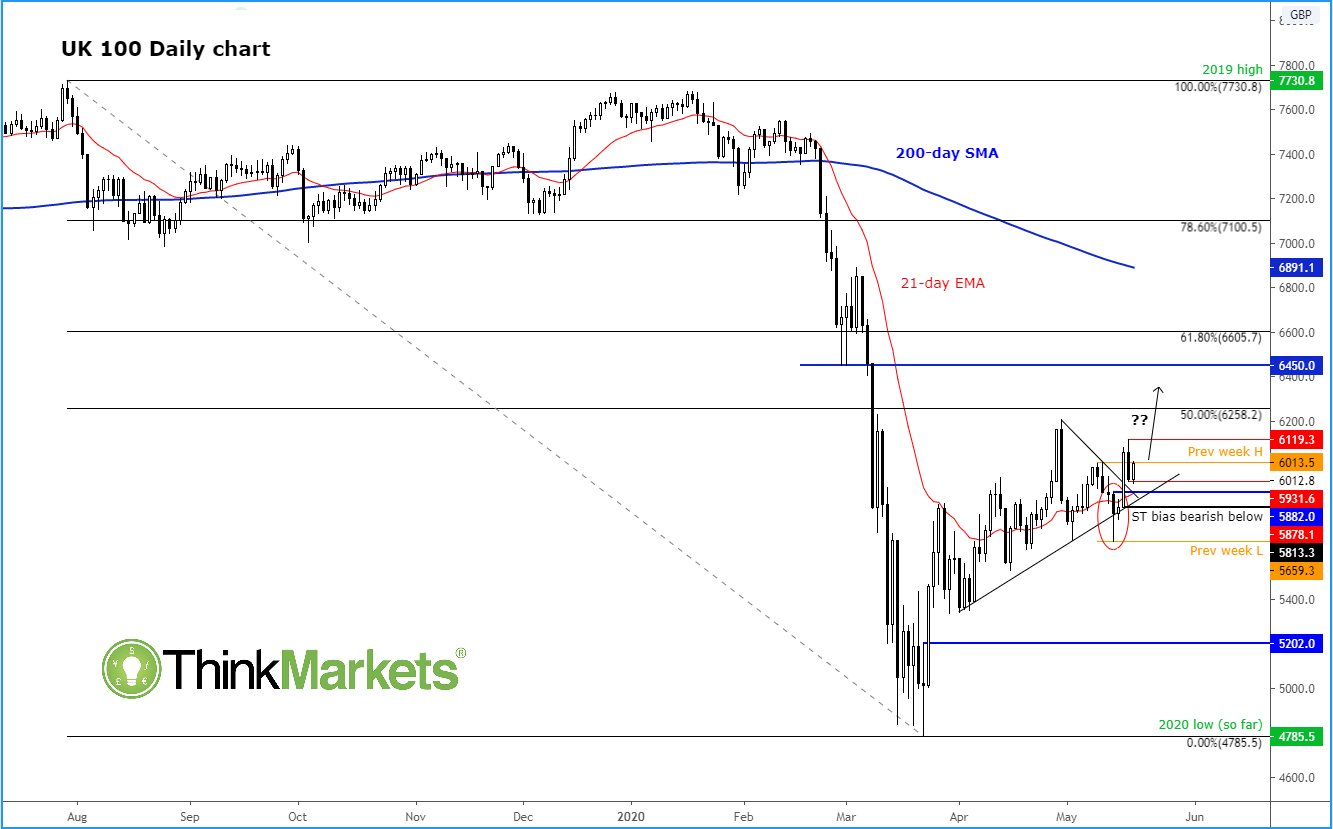

Chart to watch: FTSE

The UK benchmark index continues to drift higher along with the global equity markets. Currently it is showing some bullish characteristics given the broken trend line and as it is holding above the now-rising 21-daye exponential moving average. So, the path of least resistance remains to the upside despite yesterday’s sell-off. However, a break below Monday’s thrust candle could spell trouble for the bulls. If that were to happen, the we would turn technically bearish on the FTSE again.