{kind=link}

In Britain, the preliminary PMIs for May will hit the markets at 08:30 GMT Thursday, ahead of retail sales for April at 06:00 GMT on Friday. The PMIs are expected to rise, but to remain deep within contractionary waters, while retail sales are primed for a record collapse. As for the pound, it is being battered from all sides. The UK economy will reopen very slowly, investors are worried that today’s exploding deficit will result in austerity tomorrow, the BoE is considering negative rates, and to top everything off, the risk of a no-deal Brexit is back on the radar.

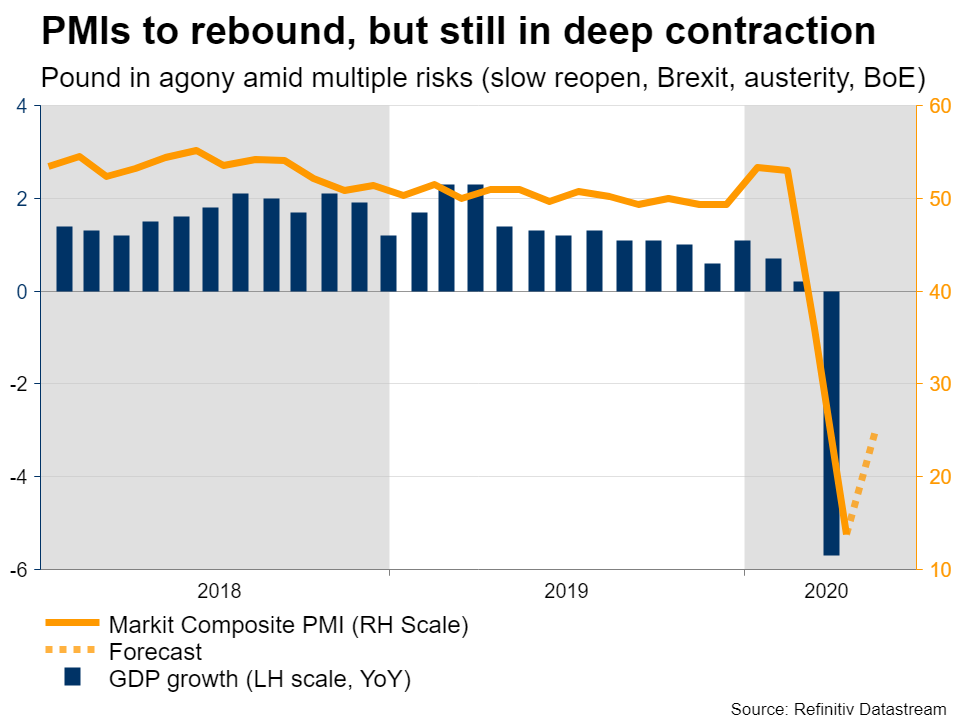

PMIs to improve from depressed levels

The UK economy was among the last to go into lockdown in late March, and with the health crisis still raging, it’s only natural that it would be among the last to re-open. Economic growth for March – which only captured a few days of the lockdown – was a catastrophic -5.8%, and the data for April might be even worse. Indeed, retail sales for April are forecast to show a record collapse of -16% from the previous month.

But the PMIs for May are set to provide a glimmer of hope. The manufacturing index is expected to tick up to 36.0 from 32.6 in April, while the all-important services print is seen at 25.0, a notable improvement from the all-time low of 13.4. Alas, while these increases would be encouraging, both figures would still be a far cry from the 50 level that separates expansion from contraction, signalling that the economy remains in a deep recession.

Sterling besieged from all sides

Turning to the pound, it has been in agony lately amid a toxic cocktail of developments. First, markets weren’t impressed by the government’s handling of the health crisis, as the early hesitation to shut down the economy now means a longer period of things staying shut. Second, there are growing fears the exploding government deficit will result in ‘belt tightening’ austerity once the crisis ends, either via tax increases or by spending cuts or both, sapping demand as the recovery begins.

Third, Brexit negotiations have resumed but they’ve been fruitless, and we might be headed for more drama soon. The UK has until the end of June to decide whether it wants to extend the current transition period beyond December, and Prime Minister Johnson has been most adamant that he won’t. If not, that would make a no-deal Brexit at the end of the year the default option, and while this may ultimately be a negotiating tactic by Johnson to extract concessions, what’s certain is that the threat of a no-deal exit will haunt sterling over the summer.

The final nail on the coffin is that the Bank of England is thinking about negative rates. Some policymakers – including chief economist Haldane – recently pointed out they’d be open to that. It’s a controversial option because judging from the European experience, negative rates can weaken the financial sector that Britain’s desperately relies on.

Note however that this could also be a ‘trick’. Simply by not ruling anything out, the Bank can get markets to bet on negative rates, which loosens financial conditions and has similar effects to a rate cut – but without actually cutting rates. Either way though, as long as this option is on the table, it’s just another factor that will limit any sterling upside.

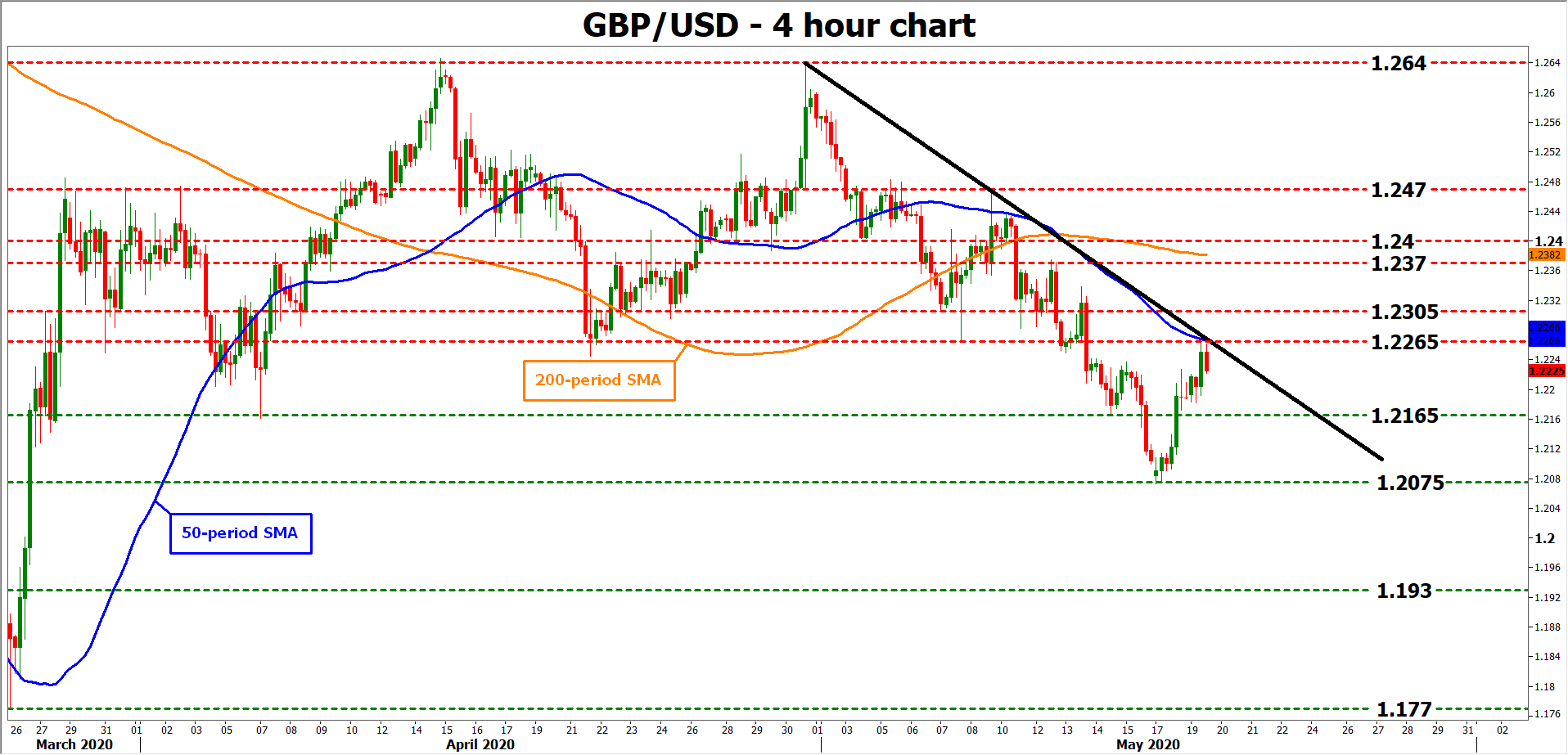

Looking at sterling/dollar technically, it has been trading beneath a downtrend line since early May and if the bears stay in charge, their next target might be the 1.2165 zone.

On the upside, if the bulls penetrate above 1.2265 and that downtrend line, the next area to offer resistance may be near 1.2305.