{kind=link}

The coming week seems relatively quiet. The preliminary PMIs for April in the UK, US, and Eurozone will give us an update on how much businesses have suffered, while the minutes of the latest Fed meeting might reaffirm the central bank’s willingness to do even more, even as Chairman Powell hints that Congress should take the lead. Overall though, the most important variables for investors may be how quickly new virus cases increase now that economies are partially re-opening, and whether US-China tensions flare up any further.

Back to reality?

Stock markets went on a tear since early March, staging a powerful comeback thanks to a deluge of stimulus and liquidity by governments and central banks, but investors have turned a little more skeptical in recent days. Equities are ending the week in the red while the defensive dollar is ascending, on fears that the US is re-opening its economy too soon and amid boiling US-China tensions.

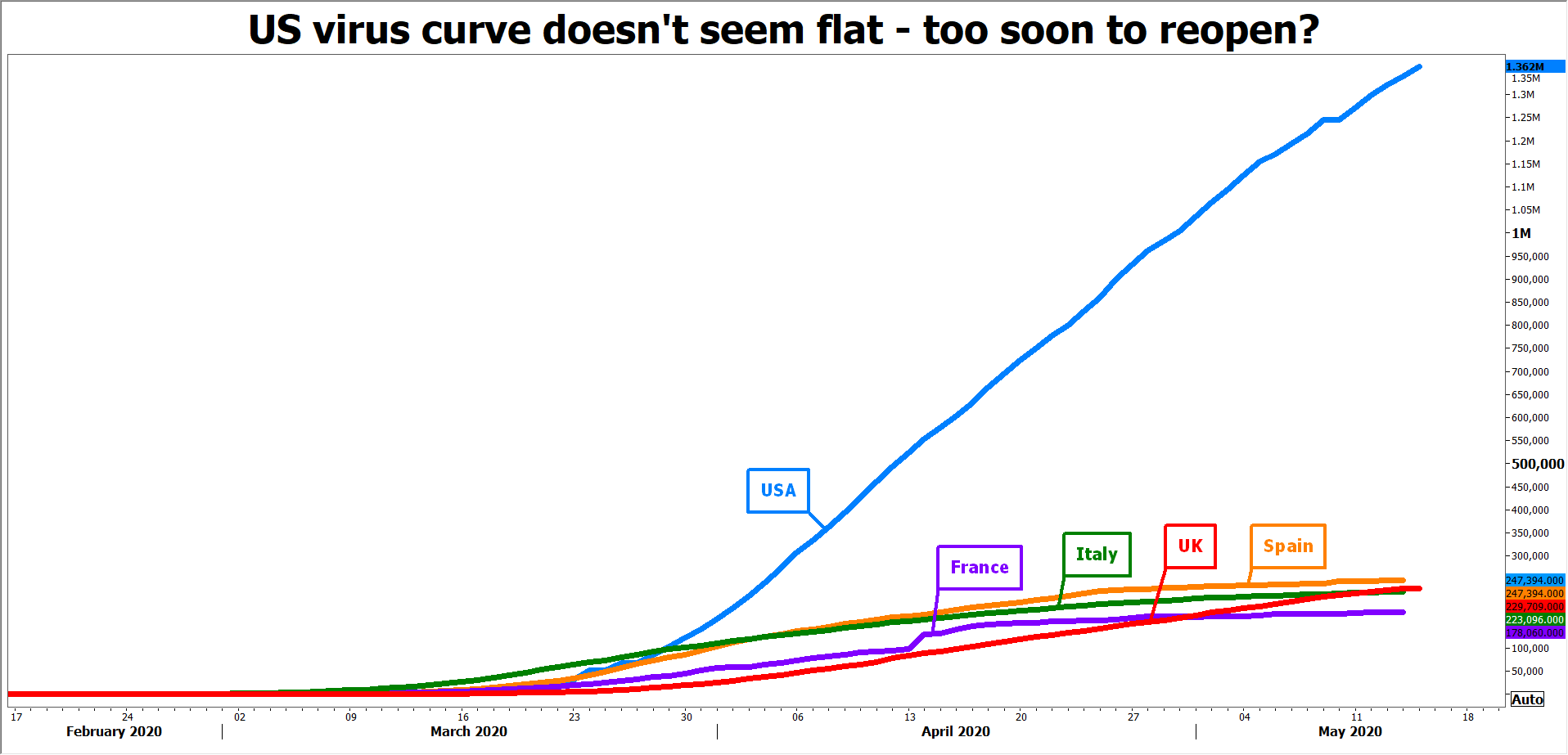

Many American states have partially re-opened already, but if one excludes New York from the nationwide US numbers, the outbreak elsewhere doesn’t seem to have reached its peak. The concern is that opening up too soon could ignite second waves of infection and force the US into future shutdowns, derailing the economic recovery.

To make matters worse, US-China relations were already icy cold before the pandemic, but things have escalated to a new level lately as Trump attempts to pin the blame for the outbreak on Beijing. It’s now clear that his election strategy is to launch a political broadside on China, so tensions will likely escalate further ahead of November’s election. But perhaps this time he won’t go for tariffs, as other options being floated are blocking US pension funds from investing in Chinese stocks or restricting the access of Chinese companies to US capital markets.

The icing on the cake is that the Fed is quietly suggesting more stimulus will be needed, but that it should come from the fiscal side. That was the implied takeaway from Chairman Powell’s comments this week, even though he naturally pledged that the Fed will also do whatever is necessary. Unfortunately for Powell, the Republicans seem to have little appetite for more stimulus as the exploding deficit could tarnish their fiscal-discipline image in a crucial election year.

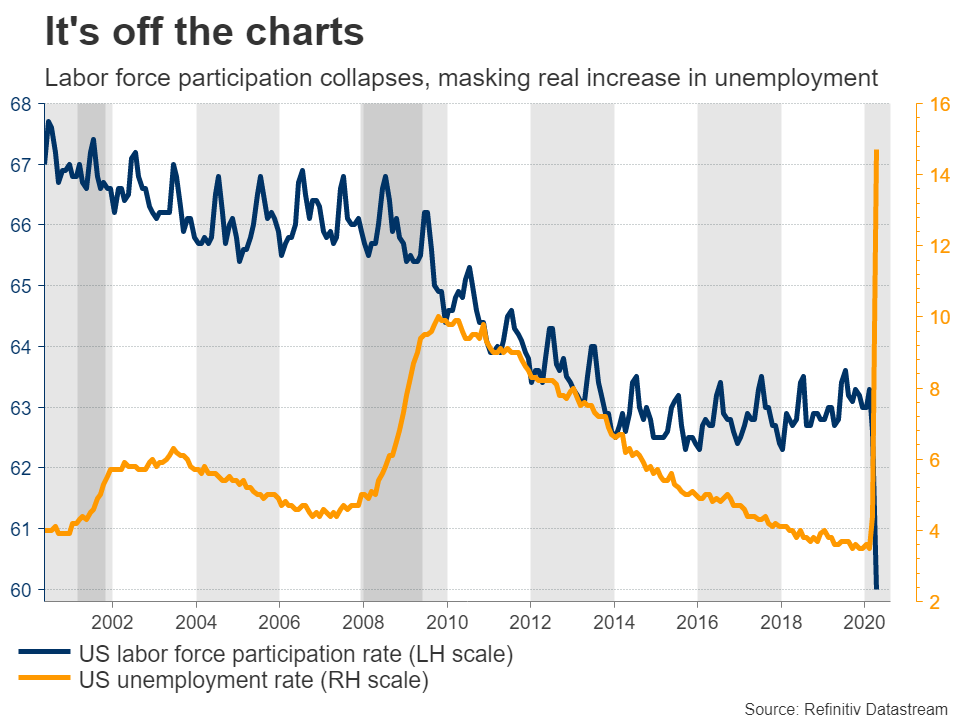

So to recap: the world’s biggest economy may be making a policy mistake by opening too quickly, trade tensions have returned with a vengeance, and the Fed is implicitly saying fiscal policy should take the lead – but Congress is hesitant. Meanwhile, 36 million Americans have lost their jobs, and recent data from China adds to a body of evidence that consumers remain reluctant even after the economy reopens. That seems like a toxic cocktail for riskier assets like stocks going forward, but a recipe for success for safe havens such as the yen and gold.

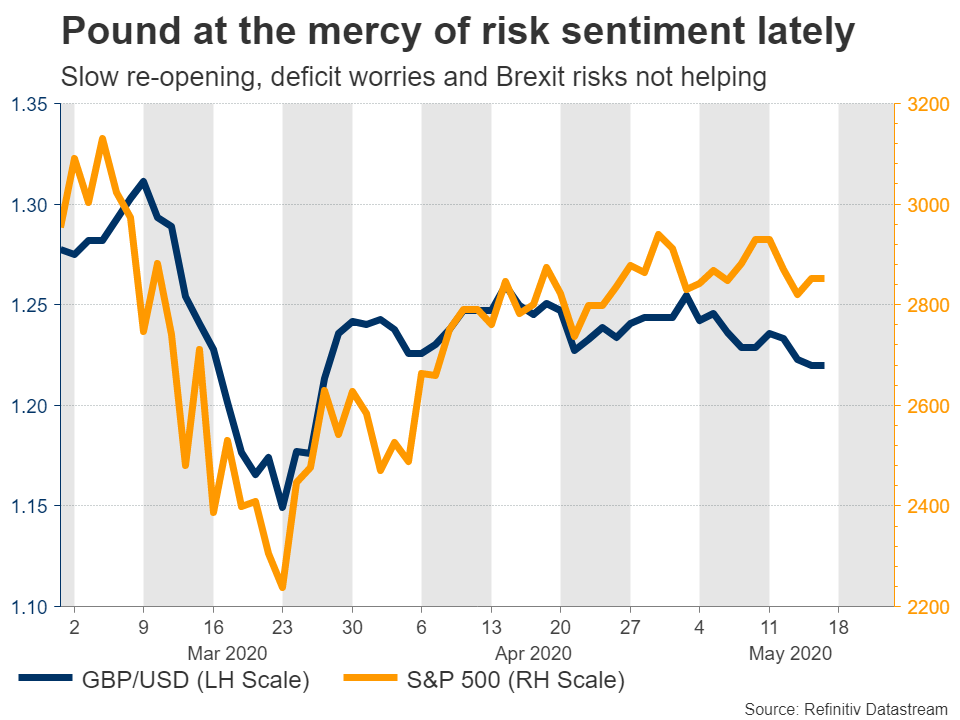

The dollar is trickier. Even though it’s been the market’s beloved haven in this crisis, that might be called into question if the US is forced into rolling shutdowns. Not to say that any major downtrend would be forthcoming, but rather that it could lose a little of its shine.

US PMIs eyed as Fed’s upper echelon speaks

Beyond how the US virus numbers evolve, there’s a lot to keep traders busy in America. On Wednesday, the Fed releases the minutes of its latest meeting, where policymakers are nearly certain to reiterate they stand ready to act again, even though they are almost out of ammunition. Thursday will bring the weekly jobless claims and the preliminary Markit PMIs for May. Admittedly though, the market doesn’t react much to data nowadays.

Instead, investors might tune in for some remarks by Fed Chairman Powell, Vice Chairman Clarida, New York Fed President Williams and board member Brainard, all of whom speak on Thursday. They are all permanent FOMC voters and arguably the Fed’s ‘top four’. Ahead of all this, Powell testifies before Congress on Tuesday.

Flood of UK data due, Brexit talks a risk

In Britain, there’s a flood of economic data coming up, starting with the employment figures for March on Tuesday. Then on Wednesday, inflation numbers for April are due, ahead of the flash PMIs for May on Thursday, which could attract the most attention. The week culminates with retail sales for April on Friday.

As for the pound, it has been besieged lately by a blend of weak risk appetite, concerns about the UK government’s handling of the crisis, and by fears that the exploding fiscal deficit might result in ‘belt-tightening’ down the road, crippling demand as the recovery begins.

Moreover, Brexit talks have resumed but they’ve been fruitless, and things might get worse. The UK must decide by the end of June whether it will request an extension to the transition period beyond December, and PM Johnson insists he won’t. That means a no-deal Brexit at year-end becomes the default, and while this may be a negotiating ploy by Johnson, it’s still difficult to have any confidence in the pound ahead of what promises to be a drama-packed summer.

Euro area PMIs unlikely to rescue battered euro

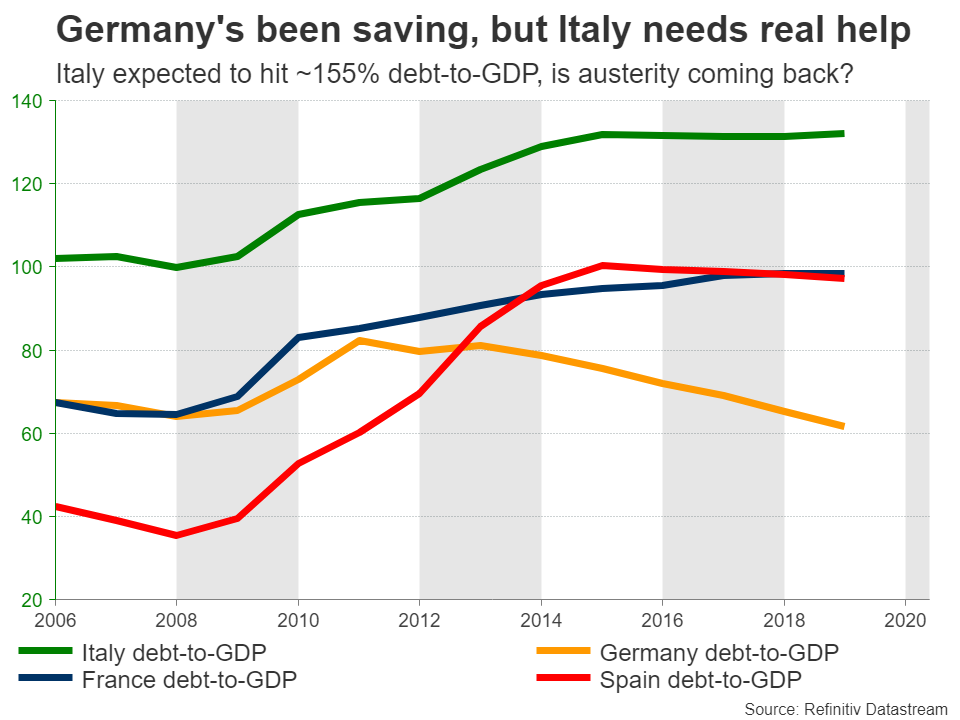

In euro land, EU infighting and the lack of a powerful stimulus package have wrecked the single currency, and the upcoming PMIs on Friday are unlikely to change that gloomy picture. The only catalysts that could turn the euro’s fortunes around are the EU finally delivering a large rescue package with favorable terms for highly indebted countries, or the dollar losing some ground as a result of second waves.

Alas, even in this case, it’s unlikely that the euro can stage a sustainable rebound. The EU has a broken institutional infrastructure that is both too slow to respond to shocks and not lenient enough with economies that need help the most, so the recovery might be anemic, especially if calls for fiscal ‘belt tightening’ return once the crisis blows over. The game changer to all this would be some risk-sharing mechanism like Eurobonds, but don’t hold your breath.

Commodity currencies at the hands of risk sentiment

While Australia and New Zealand handled the health crisis better than most, they are export-driven economies, so their currencies are mostly driven by global developments. In this sense, how US-China tensions evolve might be more important to the aussie and kiwi than either the RBA minutes on Tuesday or New Zealand’s retail sales for Q1 on Friday.

In Canada, inflation data for April are due Wednesday ahead of Friday’s retail sales for March.

Finally in China, the central bank will meet Wednesday ahead of the annual People’s Congress on Friday. It will be interesting to see what stimulus measures will be rolled out, especially in the face of a growing spat with the US.