{kind=link}

Yesterday, US President Donald Trump spoke very unexpectedly in favour of a strong dollar. He said in a Fox interview: “It’s a great time to have a strong dollar. Everybody wants to be in the dollar because we kept it strong”. This is precisely the position that the US presidential administrations have publicly supported, at least since the 1990s. However, in 2017 Trump himself spoke about the advantages of a weaker dollar. The Fed’s constant push for a softer policy is also weakly combined with a commitment to a stronger dollar. So why did the rhetoric change? There are two reasons for that.

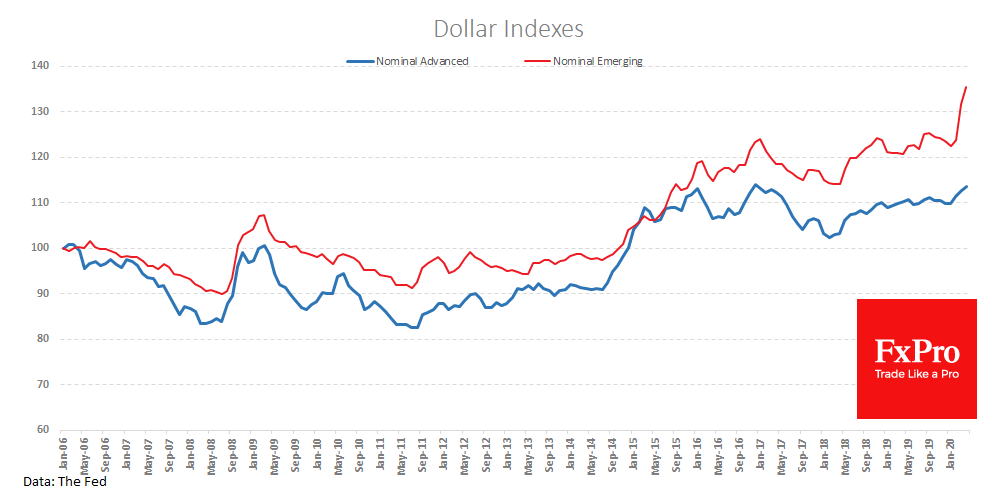

Firstly, it is a tactic common to politicians: if you can’t beat them lead them. The turmoil in the financial markets in the first quarter of this year, among other things, generated a high demand for the dollar. The capitals were returning home, and the dollar plays as safe-haven. If you look at the dollar against the euro or the yen, you won’t see any powerful shifts, because these currencies are mostly in the same weight category – currencies of rich economies, with low rates. However, the Brazilian real, the Turkish lira, and many other currencies have significantly decreased this year, underscoring the trend towards the growth of the dollar.

Secondly, it is time to compete for capital. Although the Fed buys assets on its balance sheet by unprecedented volumes, the US government’s borrowing is even more unprecedented. The US government plans to borrow more than $4.4 trillion by the end of the year and will clearly increase its appetite in the next few years. In other words, the US president should behave as a seller in the eastern bazaar, praising his merchandise and noting its value. After all, this “merchandise” may become very extended soon. The secondary market must not have a parallel increase in supply; that is, the existing owners of the “merchandise” do not begin to get rid of it.

The US. Treasury, in contrast to 2009, now relies on the issue of long-term government bonds to use a period of abnormally low rates and avoid the need to enter the market again and again to refinance debt. The rates on these long-term bonds are more volatile than short-term ones. Considering the long term horizons, investors demand more premium for long-term risks and also take into account exchange trends towards their main competitors. And here the dollar has something to boast about in recent years.

Thus, having recruited Trump into its allies, the dollar may well maintain an upward trend throughout the period when the US Treasury needs money outside, i.e. for the coming quarters.