{kind=link}

For the 24 hours to 23:00 GMT, the EUR declined 0.61% against the USD and closed at 1.0838.

On the macro data, Euro-zone’s producer price index dropped 2.8% on a yearly basis in March, driven by sharp fall in energy prices and more than market forecast for a drop of 2.6%. In the previous, the index recorded a revised fall of 1.4%.

In the US, the trade deficit widened to $44.4 billion in March, compared to a revised deficit of $39.8 billion in the previous. Moreover, the Markit services PMI fell to 26.7 in April, compared to a level of 39.8 in the prior month. The preliminary figures had indicated a fall to 27.0. Meanwhile, the ISM non-manufacturing PMI contracted for the first time in over ten years to 41.8 in April, less than market consensus for a drop to a level of 36.8. In the previous month, the PMI had recorded a reading of 52.5. Additionally, the IBD/TIPP economic optimism climbed to 49.7 in May, compared to a level of 47.8 in the earlier month.

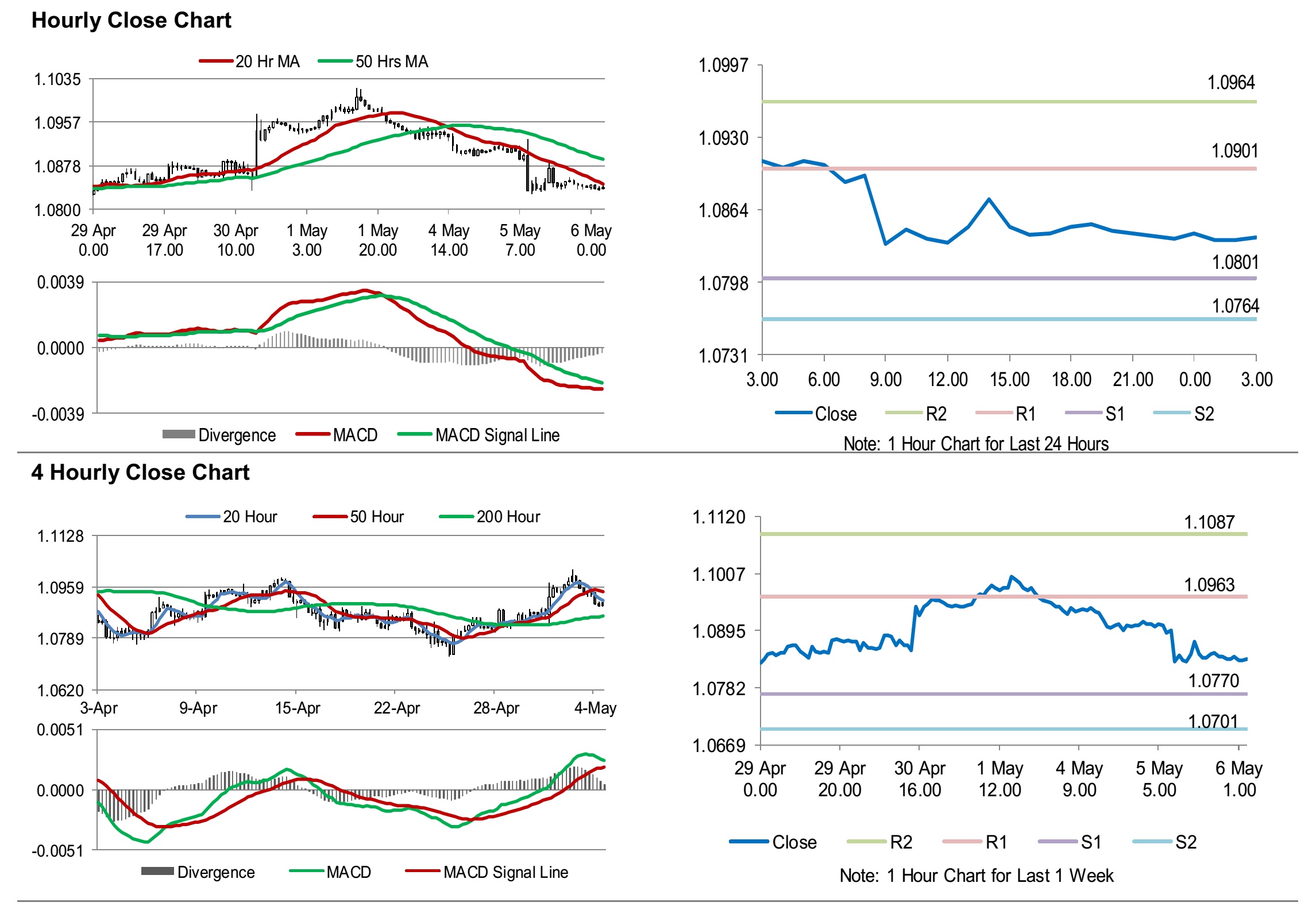

In the Asian session, at GMT0300, the pair is trading at 1.0839, with the EUR trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.0801, and a fall through could take it to the next support level of 1.0764. The pair is expected to find its first resistance at 1.0901, and a rise through could take it to the next resistance level of 1.0964.

Moving ahead, investors would keep a watch on Euro-zone’s Markit services PMI for April and retail sales for March, slated to release in a few hours. Additionally, Germany’s factory orders and the Markit services PMI, both for April, would keep investors on their toes. Later in the day, the US ADP employment change for April and the MBA mortgage applications, will be eyed by traders.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.