{kind=link}

- At first glance, the ECB meeting next week is not expected to bring new policy measures after the host of measures taken by the ECB over the past six weeks, notably the PEPP programme of EUR750bn, collateral easing and abundant liquidity.

- However, new policy responses cannot be ruled out as the ECB seems to be the only game in town in the near term and will signal a readiness to act.

- We expect core/semi-core rates to remain range bound post ECB meeting. We recommend receiving Dec 20 3m Euribor.

Length and depth unknown…

While the worst in terms of COVID-19 infections is probably behind us for now, evidence of the severity of the economic fallout is just starting to emerge. Flash PMI readings for April pointed to the steepest fall in business activity for the euro area ever recorded. While the service sector bore the initial brunt of the corona crisis, the collapse in demand and supply constraints have now also caught up with manufacturers. Employment losses also gathered speed, although anecdotal evidence suggests short-term work schemes in Europe are helping to limit job losses.

We expect the ECB to acknowledge the severity of the current recession as the worst since the 1930s, but stress that uncertainty about its length remains significant. Uncertainty also reigns with respect to the inflationary impact. With the corona crisis constituting both a demand and a supply shock, its effect on medium-term inflation is not clear cut (see Euro Area Research – Euro inflation in the corona maelstrom, 1 April 2020). Added to this the data quality of the coming HICP prints will be lower than usual, with a significant part of the (services) sub-indices featuring imputed prices as price collection is severely hampered due to lockdown measures. Because of these issues of data reliability and country heterogeneity in imputation methods, central bankers and markets will probably also put less weight on the coming inflation prints.

… so no need for new easing…

As a result of the unknown length and depth of the crisis and with ECB having already launched its PEPP, buying EUR750bn until year end, an additional APP envelope of EUR120bn this year as well as its EUR20bn/month, we do not expect an increase in the purchase programmes (or rate changes) at this stage. The ECB has so far only used around 10% (EUR70bn) as of last Friday of the EUR750bn and likely around EUR30bn of the additional APP envelope.

Therefore, we expect the ECB to reiterate its commitment to stand ready to increase and extend the purchase programme and stand ready to act should more be needed.

… but targeted measures should not be ruled out

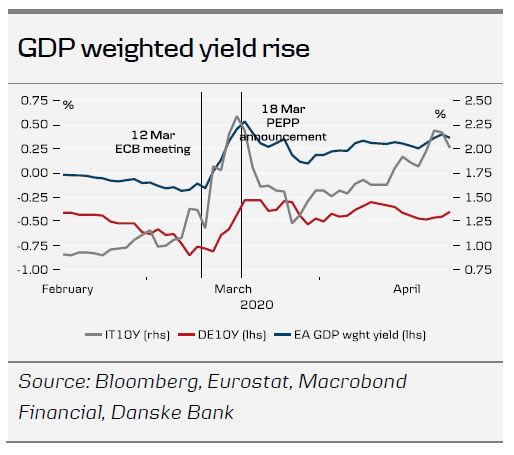

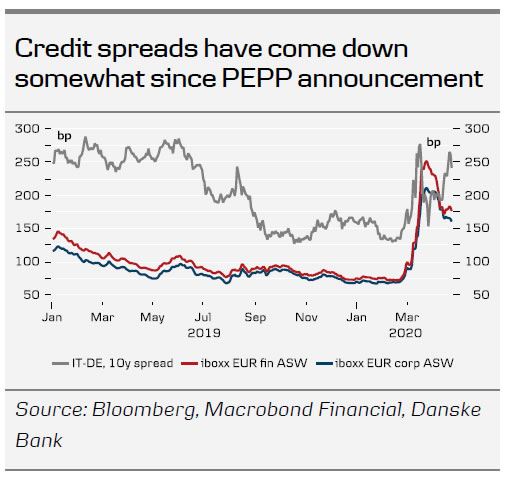

It is with some concern that we are observing the recent financial market fragmentation in specific market segments, though credit spreads have come down somewhat lower since the PEPP announcement. One of the ECB’s preferred measures, the GDP weighted yield has risen almost 30bp since the trough in late March on the back of particularly higher peripheral yields, and we are only some 40bp lower than at the announcement of PEPP.

Euribor concern – ECB to take a cautious stance

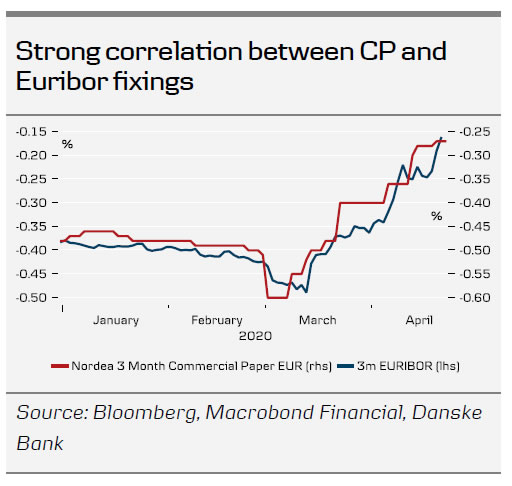

Notably, the Euribors have risen sharply in the past month by 30bp (3m Euribor) on the back of credit risk, increased issuance etc. The ECB has already tried to address this by reducing the haircuts applied to collateral on 7 April and with its most recent statement this week addressing rating downgrades (fallen angels), where even ‘junk’ bonds will be accepted as collateral, the ECB has already done a lot on collateral. While it has already deployed most of the usual mechanisms to address rising Euribors (liquidity, collateral, haircuts, even buying commercial paper, which is usually strongly correlated to Euribor fixings, in the PEPP), it still has the rate cut possibility. However, with EONA / €STR fixing stable around the deposit rate, we do not believe such a policy tool would be used, similar to its reaction function prevailing since late last year. It is still not clear to us how, and if, the ECB can address this directly and as a result, we expect the ECB to ‘sweat this one out’ as long as it does not become significantly worse, and refer to the already deployed measures needing to have time to work. Should the ECB try to address this, they could (on top of the measures above):

- Increase the focus on commercial paper (CP) in the PEPP. While daily data quality is rather poor in the CP market data, we note a close correlation between CP rates and Euribor fixings – and as such this may be the most direct impact on the Euribor fixings.

- Announce a purchase programme specifically designed to address short-end issuance (bills). While not all debt offices have published their issuance plans / structure, we could see up to EUR400bn in bills issues for the this year. That means the ECB could create an additional pandemic bills programme of at least that amount to address this. However, this is not a given as it may lead to lower Euribors and furthermore, the ECB can already buy 71d paper via the PEPP.

Liquidity is still abundant – receive 3m Euribor December 20 contract

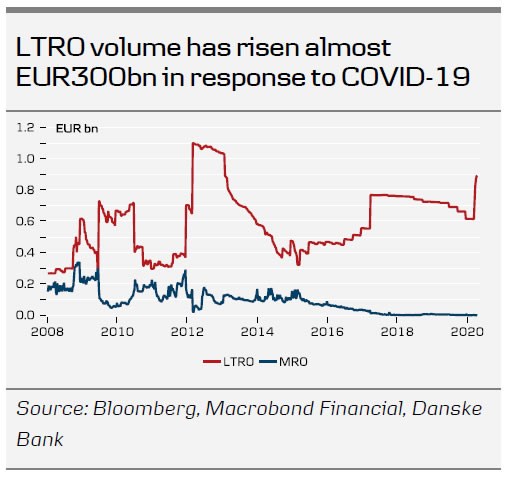

The very generous LTRO terms (weekly operations with maturity on 24 June to bridge finance to TLTRO) at the deposit rate of -50bp have been heavily used. Euro area banks have taken EUR276bn since the launch in March, however with collateral easing in the recent week and the eligibility pool increase in the TLTRO, we expect a significant rise in liquidity take up in coming weeks / months. In addition, the cheap funding in the TLTROs, where the lending rate is at -75bp (deposit rate-25bp subject to ease lending criteria) is expected to see a high take up (next TLTRO allotment is in June). More specifically, we expect June TLTRO take up in excess of EUR650bn.

With the collateral easing measures and lower haircuts, the ECB has significantly expanded the collateral pool to increase the potential take up at the LTRO and TLTROs. This is also why we expect no ECB action for now to address the higher Euribors. As a result, we recommend to receive 3m Euribor December 2020 contract at -29bp (price of 100.29). We target -40bp, with a stop loss at -23bp. The main risk to this trade is continued credit risk tightening and the new methodology being more sensitive to stress.

Rates to remain in consolidation

We do not expect a change to the current market sentiment / recent consolidation in the EGB market on the back of the ECB meeting next week. Near term, we expect Bunds to stay range bound in a -50bp to -35bp range. Notably Italy is of concern and will continue to trade weakly until either the economy opens up, albeit gradually, or a common response helps to absorb the significant supply of BTPs expected this year. As a result, we cannot rule out a further scale up of the PEPP later this year should financial fragmentation still prevail. A potential increase could be in the magnitude of EUR500bn.

FX – EUR/USD to remain weak

The ECB has made attempts to remedy the market volatility of which European institutions have otherwise themselves proved a source. The upcoming ECB meeting is unlikely to address such issues further and EUR is set to be haunted by this for some time. Indeed, with the EU council’s failure to reach a clear agreement, EUR/USD has moved lower still. This follows the somewhat clumsy communication by the ECB, where attempts at fixing the impression given have been unable to contain periphery spread widening. Clearly, it is not helping either, that all communication from officials tends to come with the word ‘temporary’ attached. In our view, this continues to suggest that the eurozone’s lack of coherence is amounting to a trending negative risk premium in spot.

That said, EUR/USD is now trading on the low side of recent ranges and one may be cautiously hopeful that the negative risk premium does not build further near term. However, it goes without saying that we continue to hold reservations as to the sustainability of EUR/USD upticks. If the ECB sticks to a wait-and-see policy with respect to the effects of what they have done as well as keeping soft guidance, this is unlikely to change much in the FX space. In turn, we look to the US and China to gauge the timing of a cyclical uptick which should instil some EUR confidence at a later point this year.