{kind=link}

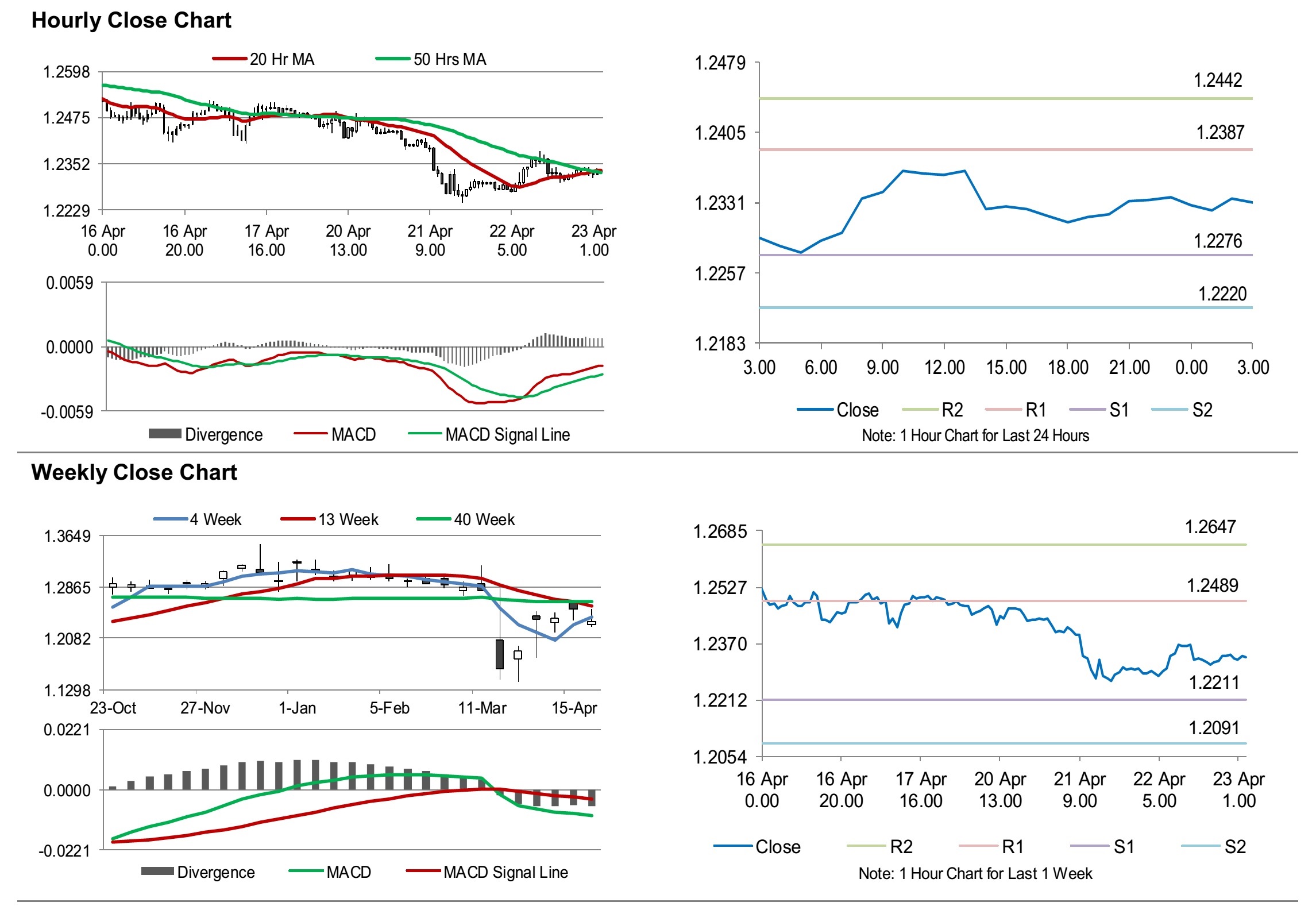

For the 24 hours to 23:00 GMT, the GBP declined 5.30% against the USD and closed at 1.2337.

On the data front, UK’s consumer price inflation slowed to 1.5% on a yearly basis in March, driven by fall in fuel, clothing prices and marking its lowest level since December 2019. In the previous month, inflation had recorded a level of 1.7%. Moreover, the DCLG house price index climbed 1.1% on an annual basis in February, undershooting market consensus for a rise of 2.2% and compared to a revised rise of 1.5% in the earlier month. Meanwhile, the nation’s seasonally adjusted output producer price index fell 0.2% on a monthly basis in March, less than market consensus for a fall of 0.4% and compared to a revised drop of 0.2% in the prior month. Additionally, the retail price index rose 2.6% on an annual basis in March, more than market forecast for a rise of 2.3%. In the prior month, the index had recorded a rise of 2.5%.

In the Asian session, at GMT0300, the pair is trading at 1.2332, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2276, and a fall through could take it to the next support level of 1.2220. The pair is expected to find its first resistance at 1.2387, and a rise through could take it to the next resistance level of 1.2442.

Moving forward, traders would keep a watch on UK’s public sector net borrowing for March, along with the Markit manufacturing and services PMIs, both for April, slated to release in a few hours. Later in the day, the GfK consumer confidence index for April, would keep investors on their toes.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.