{kind=link}

For the 24 hours to 23:00 GMT, the EUR declined 0.76% against the USD and closed at 1.0902.

On the macro front, US MBA mortgage applications advanced 7.3% in the week ended 10 April 2020. In the previous week, mortgage applications had recorded a drop of 17.9%. Meanwhile, the NY Empire State manufacturing index dropped to -78.2 in April, more than market expectations for a fall to a level of -35.0. In the previous month, the NY Empire State manufacturing index had recorded a reading of -21.5. Additionally, retail sales tumbled 8.7% on a monthly basis in March, amid coronavirus-induced lockdown and more than market forecast for a drop of 8.0%. In the previous month, retail sales recorded a revised decline of 0.4%. Moreover, industrial production slid 5.4% on a monthly in March, marking its biggest monthly decrease since January 1946 and compared to a revised rise of 0.5% in the earlier. Furthermore, business inventories decreased 0.4% in February, in line with market forecast and compared to a revised drop of 0.3% in the prior month. Also, the NAHB housing market index plunged to a level of 30.0 in April, hitting its lowest level since June 2012 and compared to a reading of 72.0 in the previous month.

Separately, the US Federal Reserve, in its Beige book report, the US economic activity contracted “sharply and abruptly” across all regions as a result of the coronavirus outbreak. The leisure, retail and hospitality sectors were most affected with severe job cuts. Looking ahead, the central bank warned that the near-term outlook was for even more job cuts in the coming months.

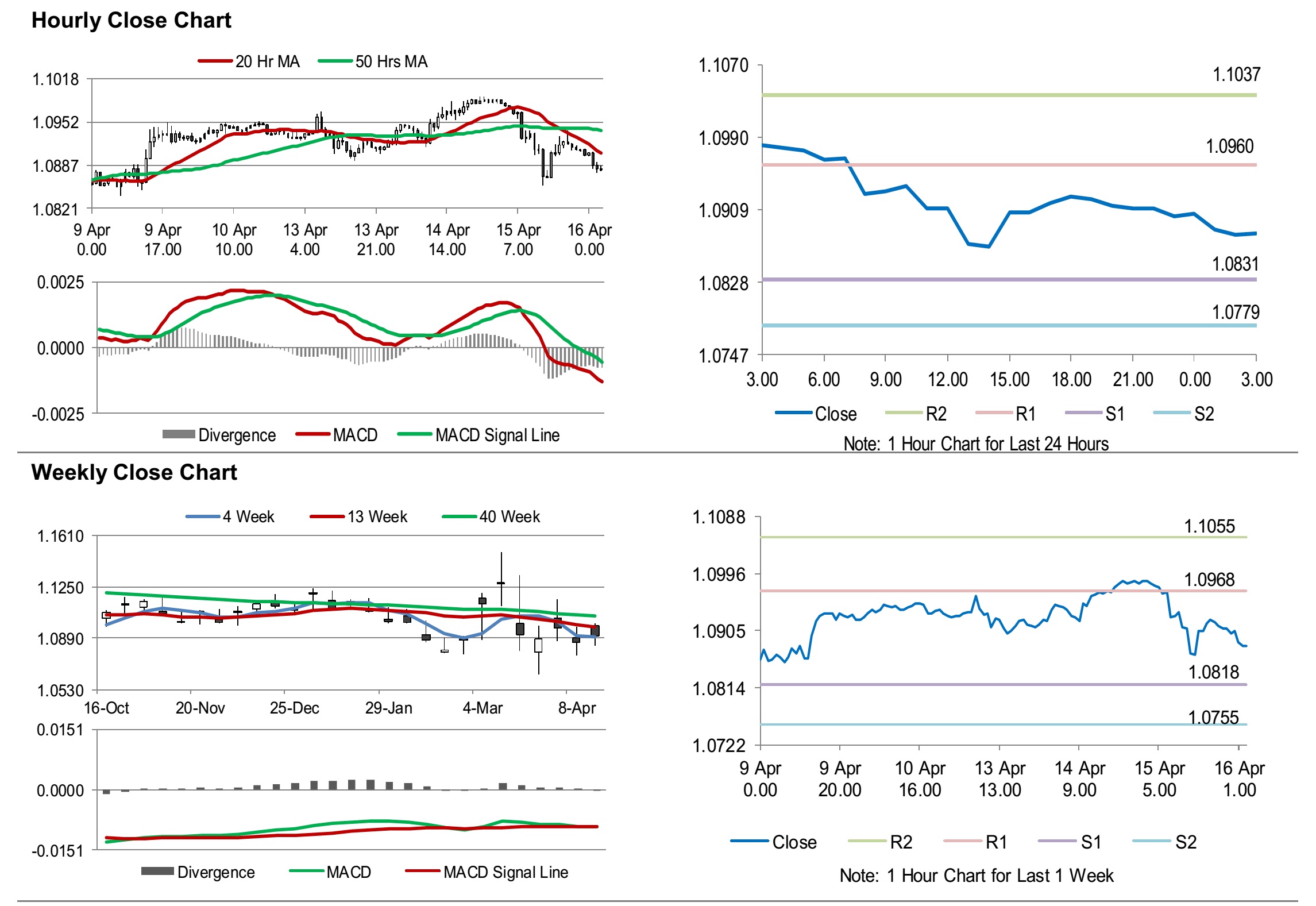

In the Asian session, at GMT0300, the pair is trading at 1.0882, with the EUR trading 0.18% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.0831, and a fall through could take it to the next support level of 1.0779. The pair is expected to find its first resistance at 1.0960, and a rise through could take it to the next resistance level of 1.1037.

Moving forward, investors would keep a watch on Euro-zone’s industrial productions for February and Germany’s consumer price index for March, slated to release in a few hours. Later in the day, the US building permits and housing starts, both for March, along with the Philadelphia Fed manufacturing survey for April and initial jobless claims, would keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.