{kind=link}

Total employment: 5.9k from 25.6k (revised from 26.7k). Unemployment rate: 5.2% from 5.1% (unrevised 5.1%). Participation rate: flat at 66.0% (unrevised 66.0%)

Headlines

As we warned in a our preview, given the timing of the survey in the first two weeks in March a small surprise rise in employment was possible.

- Employment: +5.9k, exceeding our expectations (-20k) and the market (-30k)

- Unemployment: did lift to 5.2% from 5.1% softer than forecast (Westpac 5.3%, market 5.45) but consistent with a small gain in employment.

- Participation rate: was flat at 66.0% with both male and female participation flat at one decimal place.

Additional detail

As we noted in the preview the ABS had been emphasising that the reference period for the March survey was in the first two weeks of the month and the broad based lockdowns (stay at home orders) were not implemented until the second half of March. As such, while we thought an underlying weaker trend should have been enough to generate a negative print there was a chance, giving the timing of the survey, that it could print a modest positive, which it did.

As such, don’t read too much into the small rise in employment (+ 5.9k) or the very modest rise in unemployment (5.2% from 5.1%). We are expecting to see a more significant deterioration in the April survey.

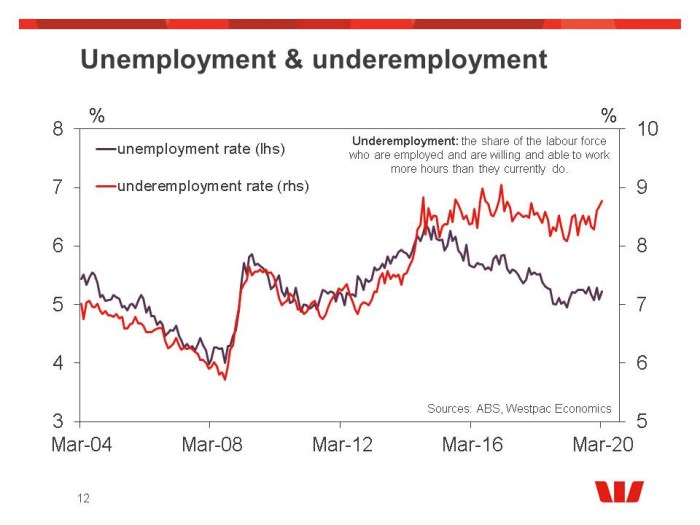

That is not to say there were not early signs of a COVID impact on top to the already weakening trend in the labour market. Underemployment has been on a rising trend and from a low of 8.3% in December it hit 8.8% in March.

Underemployment is going to become an increasingly importing for gauging the overall impact of COVID-19 on the economy. The JobKeeper package will encourage firms to keep employees that they would have otherwise let go but likely to do so on reduce hours reflecting the loss in activity. So there will be many workers who will still have a job but be looking for more hours. In addition, someone who is laid off temporarily without pay (that is there is a job to go back to when the economy recovers) will not be defined as unemployed by the ABS until four weeks after their last pay check. As many of those who have lost their jobs have been laid off, rather than dismissed, underemployment will spike ahead of unemployment.

By the states, in March unemployment rose in NSW (4.8% from 4.6%), Qld (5.7% from 5.6%), SA (6.2% from 5.8%) and WA (5.4% from 5.2%). Unemployment fell in Vic (5.2% from 5.3%).

Outlook

We are clearly looking for a larger negative shock to employment in April. The April Consumer Sentiment Survey reported that of those that were employed in March, 7% reported losing their job over the last month. If this was to translate fully across to the level of employment, a 7% decline in April would represent a fall of more than 900k. Now the Consumer Sentiment Survey can’t be translated one for one to the Labour Force Survey, and we have more work to do to finalise our April Labour Force estimate, but you can see it is going to be significant contraction.

Furthermore 14% in the Consumer Sentiment survey reported being temporarily stood down without pay. As noted above, these workers are unlikely to be reported as unemployed by the ABS for up to four weeks after their last pay check. They will, however, be picked up in underemployment which will surge well ahead of unemployment and is likely to be more representative of how the economy would have tracked without the JobKeeper package.