{kind=link}

Highlights

- Unprecedented demand destruction – the duration of which is subject to significant uncertainty – will continue to dictate global oil markets in the near term.

- OPEC+’s 10th extraordinary meeting and Friday’s G20 negotiations culminated with a historic agreement to cut oil production by a combined 9.7 million barrels per day (bpd). This supply-side response, combined with market-driven declines elsewhere, should stabilize prices and lessen the expected inventory build-up going forward.

- We have modestly downgraded our Q2 price forecast to account for weaker tracking, the accelerating slump in consumption, and storage risks. However, supply-side adjustments have prompted us to upgrade our profile for Q4 and beyond.

- Canada’s energy sector and its oil-producing provinces are struggling with slashed capital spending, production shut-ins, and dampened incomes. OPEC+’s agreement should pave the way for a return to a more supportive price environment sooner than previously feared.

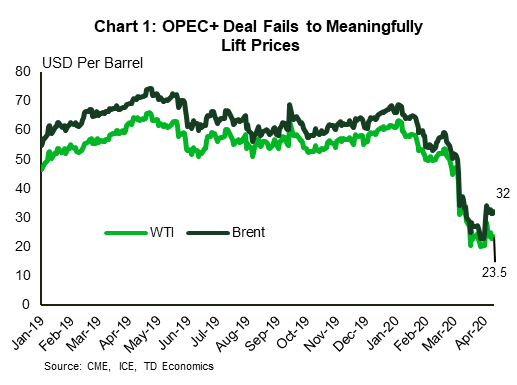

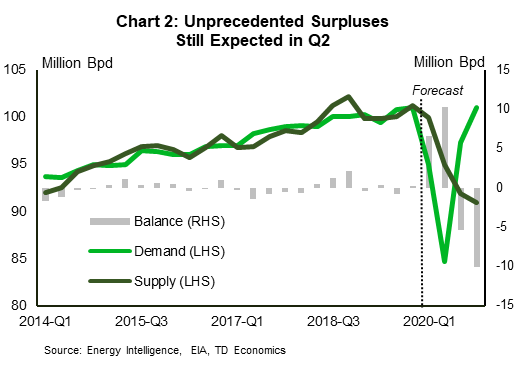

Prices for WTI and Brent have barely reacted to the historic OPEC+ deal, with both benchmark prices still more than 50% down since their peak in January (Chart 1). The scale of the recent OPEC+ agreement is notable (at an initial 9.7 million bpd), and the group’s intention to maintain substantial curbs until early 2022, if achieved, will support an earlier-than-expected rebound in prices. Additionally, reassurances of substantial market-driven declines (reportedly expected to be around 3.7 million bpd) amongst non-OPEC+ producers should also be supportive. However, the degree of demand destruction is unprecedented and will keep prices under pressure in the near term. Even with the stated cuts, the global oil market is expected to face a surplus of around 10 million bpd (and possibly more) in Q2 (Chart 2).

For Canada, the special follow-up interviews with energy sector representatives in the latest Bank of Canada Business Outlook Survey demonstrate the direness of this shock (see note). Indeed, respondents viewed this experience as being worse than the 2008 financial crisis and the 2014 oil shock recession. Canadian heavy oil prices have seen outsized impacts during the crisis, sinking to single-digit levels that are barely sufficient to even cover transportation costs. This has led to production shut-ins, with reports of up to 1 million bpd expected in the next few months. This would be a deviation from the 2014-15 price shock, when overall production in Canada kept growing – as conventional oil production dropped and bitumen production kept spiking. Looking ahead, supply-side adjustments should set the stage for a recovery in prices during the second half of the year in tandem with global benchmarks.

For Canada, the special follow-up interviews with energy sector representatives in the latest Bank of Canada Business Outlook Survey demonstrate the direness of this shock (see note). Indeed, respondents viewed this experience as being worse than the 2008 financial crisis and the 2014 oil shock recession. Canadian heavy oil prices have seen outsized impacts during the crisis, sinking to single-digit levels that are barely sufficient to even cover transportation costs. This has led to production shut-ins, with reports of up to 1 million bpd expected in the next few months. This would be a deviation from the 2014-15 price shock, when overall production in Canada kept growing – as conventional oil production dropped and bitumen production kept spiking. Looking ahead, supply-side adjustments should set the stage for a recovery in prices during the second half of the year in tandem with global benchmarks.

Supply Cuts Will Be More Relevant In The Medium And Long Term

Stealing the show in the past week were OPEC+’s 9th and 10th emergency meetings (see final press release) and Friday’s G20 negotiations. These concluded with a deal to cut 9.7 million bpd, with each OPEC+ producer promising to reduce output by around 23% from its baseline. Details included:

- An agreement to cut global oil production by an initial 9.7 million bpd for two months starting on May 1st. Cuts will then be eased to 7.7 million bpd until year-end, and then to 5.8 million bpd through April 2022.

- Saudi Arabia and Russia will shoulder 50% of the cut. Each will cut output around 2.5 million bpd from a baseline of 11 million bpd. For the remaining producers, October 2018 production will be used as the baseline.

- The group will meet on June 10th to assess the impacts on oil markets and discuss if further action is required. The extension of the agreement is set to be reviewed in December 2021.

- A statement was issued in the preceding G20 meeting reaffirming the importance of stability in global energy markets. There were reports of promises to cooperate and of ramped up efforts to purchase oil at current prices for strategic reserves. A Minister was also reported to have suggested a 3.7 million bpd cut by other producers (the U.S., Canada, Brazil, etc.). However, there is still some uncertainty on the degree of non-OPEC+ declines – which are market-driven, as opposed to explicit or binding commitments.

Meanwhile, despite the absence of an explicit commitment to curb production by other producers, market-based declines are already starting to take place:

- The IEA1 estimates that around 4% (3.8 million bpd) of global oil production would be uneconomic at a Brent price of US$30 (WTI of around US$26). At a Brent price of US$20, this proportion rises to 7.5% of total global production (7.5 million bpd). North American production accounts for a disproportionate share of these figures.

- Case in point, the latest Dallas Fed Energy Survey2 of U.S. energy companies revealed a WTI price range of US$23-US$36 for operating expenses in the U.S., which is the world’s largest producer. In Canada, shut-have already been confirmed, with reports of up to 1 million bpd expected overall in the near term.

- It is unlikely that all producers operating below their short-term breakeven costs would shut-in production. Some producers are temporarily hedged, while others will prefer to take a wait-and-see approach on other suppliers’ responses. For Canadian producers, a further cushion from the drop in the value of the Canadian dollar (5 cents since January) may also help modestly.

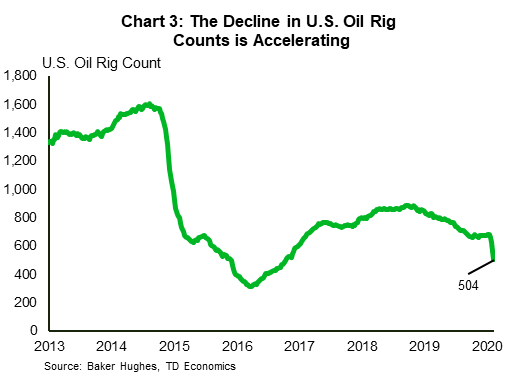

- From a medium-term perspective, the notable hit to capital spending globally will also impact production in the medium term. Globally, the IEA3 has cited a 20%-35% reduction in capital spending relative to pre-COVID-19 plans. In Canada, the Bank of Canada’s Business Outlook Survey cited a 30% drop in capital expenditures. This trend is also especially true in the U.S., where the persistent decline in rig counts since early 2019 has recently accelerated (Chart 3). Indeed, the EIA has recently trimmed expectations for U.S. oil production and is now projecting a 0.5 million bpd decline in 2020 on average and a further 0.7 million bpd decline in 2021. Production has already started declining, and the expected yearly drop in 2020 would be the first since 2016.

In the Near Term, Demand Remains Front and Center

These measures and the expected market-driven responses are by no means insignificant. However, they come against an even more substantial hit to demand. Overall estimates are subject to a significant amount of uncertainty, but consumption is expected to drop by at least 25 million bpd in April and by around 10 million bpd in Q2. This follows an already-weak backdrop in the second half of Q1 as China’s economy mostly ground to a halt. The hit is being felt throughout the product spectrum and the value chain:

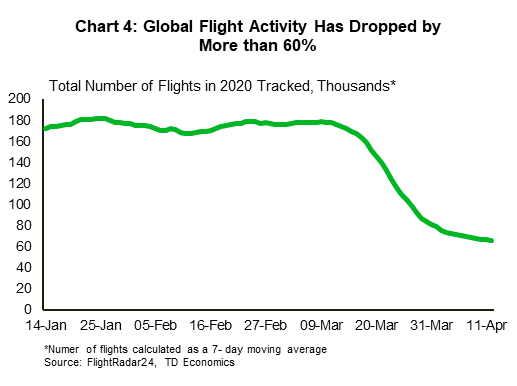

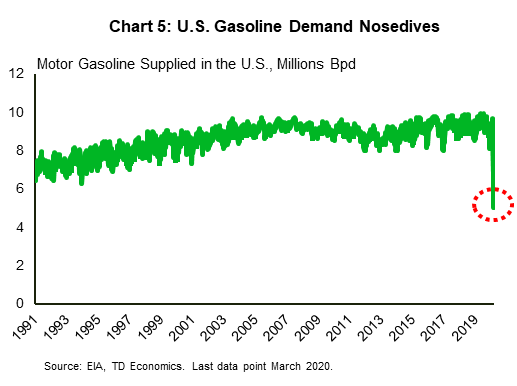

- Gasoline and jet fuel demand crumble: together, these two products represent slightly more than 35% of total global oil demand. Global flight activity has fallen by more than 60% since February – and is expected to decline more in the weeks ahead (Chart 4). For gasoline demand, the latest figures in the U.S. (the world’s largest consumer) show a steep 48% drop (y/y) in demand – to the lowest level since EIA data records began in 1991 (Chart 5). Lower retail prices aren’t expected to drive higher demand given the necessary stay-at-home measures.

- Industrial and manufacturing activity will also be impacted: industrial and heating products, like LPG, naptha, and other fuel oils, are less impacted. However, they will still experience a hit from some factory closures and the usual reduction in global industrial activity associated with economic downturns.

- The combination of these factors is exhausting storage capacity globally: While there is a lack of data on global storage capacity, media reports of increased floating storage use and a spike in tanker rates suggest that capacities are approaching their limits. For landlocked producers in Canada and the U.S., this risk is greater given their lack of access to floating storage.

- The shock is reverberating across the entire value chain: Because of restrained end-product demand, refinery margins are being squeezed, and in some cases turning negative. As a result, refinery capacity utilization has declined in most of the U.S. PADD regions by at least 10% since February.

Price Upside Is Limited Until Demand Stabilizes

The most important pre-condition for a recovery in prices is the normalization of global demand. A return to moderate global growth is predicated on our assumption of a gradual return to more normal economic activity starting in May, accompanied by a sustained revival in risk appetite in financial markets. At the same time, however, it will take several quarters for global GDP levels and risk appetite to fully normalize from the losses suffered in May. Likewise, the recovery in oil demand to the 100+ million bpd range will not occur abruptly, but rather gradually.

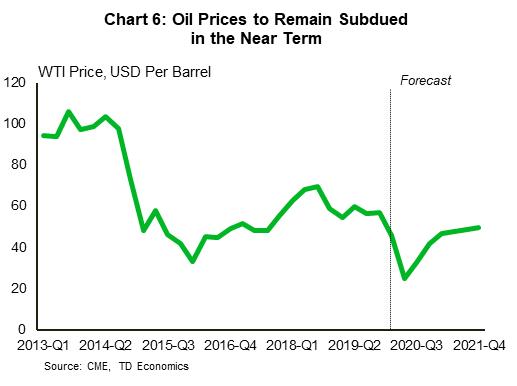

We lower our Q2 (quarterly average) price estimate for WTI to US$25 (from US$27) to account for already-weak tracking in April, slumping consumption in the U.S., and mounting global storage capacity concerns. After all, these cuts will only start in May – at which point inventories would have hit record levels. However, we also revise upwards our price profile for the Q4 to US$42, and more notably, for 2021, to an average of around US$49 for the year (See chart 6). Justifying this increase in the latter part of the horizon is the magnitude and the duration of the recent OPEC+ cuts – a portion of which is intended to last until early 2022. If the agreement is maintained, global inventories are likely to return to their pre-COVID levels by early next year after surging this quarter. Of course, this rests on a critical assumption that demand starts to normalize by May.

Outlook Subject To Heightened Uncertainty

With considerable uncertainty relating to the duration and degree of demand destruction and the stability of the supply response, the outlook is subject to several notable risks. On balance, risks are more tilted to the downside this year, namely due to the possibility of:

- Elongated demand destruction: The most significant risk is elongated demand destruction. Our base case assumes a rebound in demand beginning in May, but the speed and shape of the recovery could disappoint if containment measures are lifted more gradually and/or there are further waves of infection.

- Compliance Risks with OPEC+ Cuts: Under-compliance by some countries was reported in previous OPEC+ agreements – with Saudi Arabia usually offsetting with its own over-compliance and extra voluntary cuts. This time around, cuts are distributed relatively evenly across all producers, and risks to the agreement are likely to spike if significant under-compliance is reported.

- A rebound in drilling activity in non- OPEC+ producers once prices normalize: Not only would a significant rebound in drilling activity delay the demand-supply balancing process, it would also likely put the OPEC+ deal in jeopardy. For now, this scenario appears unlikely given the slashed capex guidance globally and the intent for global cooperation that was signalled in the G20 meeting.

There are also notable risks to the upside, but these become more relevant in the second half of the year and in 2021:

- Larger-than-expected and lasting market-driven declines: The extent of market-driven shut-ins outside of OPEC+ is difficult to pin down given that many producers are hedged, while others may whether some cash losses given their high costs of shutting-in production. However, the substantial drop in capital spending and the financial stress witnessed by some participants is likely larger than that seen in the past. If these pockets of production are permanently lost, instead of just temporarily paused, this could present a risk to future supply as demand rebounds to normal and inventories are depleted.

- Global stimulus efforts boosting consumption: For now, most of the stimulus measures seen by governments have been aimed at the most high-priority areas: providing temporary bridging support to impacted households and small business that are most vulnerable to COVID-19 impacts. The potential for further government stimulus – and notably a broadening in support measures towards infrastructure spending, could provide a much-needed boost to demand during the recovery period.

Bottom Line

Oil producers are facing a shock on a scale not seen in recent history. However, like all previous cycles, once demand normalizes, prices should gradually return to a level more conducive to a recovery in the sector. The recent supply-side adjustments may not help much in the near term. Much uncertainty remains, but the historic global curtailment agreement, if maintained, should speed up the recovery process once demand resumes to normal.