{kind=link}

U.S. Highlights

- COVID-19 continued to dominate headlines this week. But, hopes that the virus’ spread may soon peak, together with new details on the Fed’s support measures, helped support risk-on sentiment. Equities soared as a result.

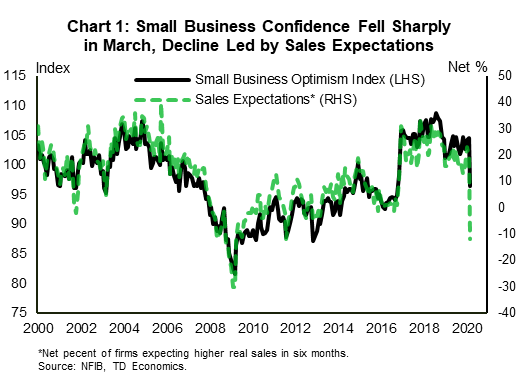

- The mood remained decisively downbeat on the economic data front, however. Small business confidence deteriorated sharply in March, with the NFIB index recording the largest monthly decline in the data’s 35-year history.

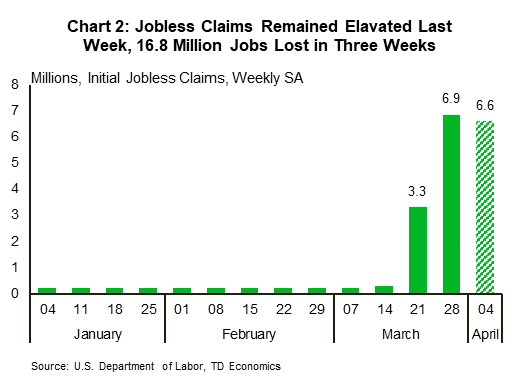

- Initial jobless claims came in at 6.6 million last week, bringing the three-week tally to 16.8 million. This means that one in ten American workers has already filed for unemployment insurance. At this pace, we expect the unemployment rate to be well into the double digits in April.

Canadian Highlights

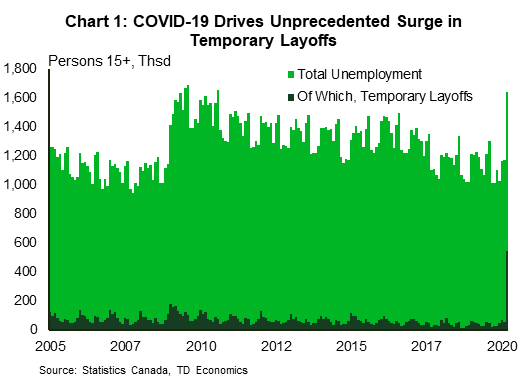

- The March jobs report gave us a sense of the economic impact of COVID-19. Although it only captured the impact at mid-month, when social distancing measures were just beginning, an unprecedented 1.01 million Canadians lost their job last month.

- Governments continue to adapt their responses. The Federal government further tweaked its wage subsidy plan to broaden eligibility. Indications are that more than 4 million Canadians have applied for EI or other benefits since mid-March.

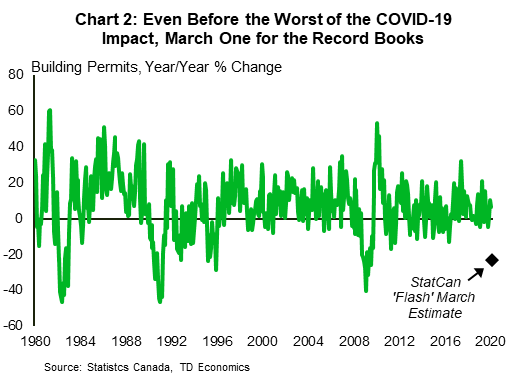

- Other early signs of the COVID-19 impact were equally eye-popping. Statistics Canada’s flash March building permit issuance estimate dropped by more than 20% year-on-year.

U.S. – Markets Roll With COVID-19 Punches

COVID-19 continued to dominate headlines this week, with U.S. cases topping 430,000 by early Thursday. But, signs that the virus’ spread may soon peak – a message echoed by top White House health advisor Dr. Fauci mid-week – supported risk-on sentiment. Equity markets rebounded, with the S&P 500 up over 12% on the week as at the time of writing. New details on the Fed’s upcoming aid to the economy and clarity on who will lead the Democrats in the fall election appeared to lend a helping hand. Politics have been on the back burner, but with Senator Sanders out of the Democratic race, investors can now more clearly weigh the policies of the two key candidates running for President in the fall. Speaking of clarity, today’s OPEC+ meeting, where production cuts are high on the menu, and tomorrow’s G20 meeting, may also offer a new sense of direction for energy markets.

The mood remained decisively downbeat on the economic data front, where the U.S. continued to take it to the chin. More evidence of the pandemic’s damage to the economy continued to emerge. Small business confidence deteriorated sharply in March, with the NFIB index recording the largest monthly decline in the data’s 35-year history. Declines among the subcomponents were led by sharp pullbacks in expectations regarding sales and the economy, and the belief that now is a good time to expand (Chart 1).

Small businesses are in the line of fire given significant exposure to sectors that have been shut down to stem the spread of the virus. Recent government measures, such as the Payroll Protection Program (PPP), should help cushion the impact of the crisis (see our recent report). More help should be on the way, with new details on the Fed’s $2.3 trillion aid package unveiled this morning. Of note, the Main Street Lending Program will help fund up to $600 billion in loans to small and medium-sized enterprises. Timely access to funds remains of the essence, however, since many businesses do not have large cash buffers to ride out a drop in revenues – a point corroborated by a recent New York Fed report – and layoffs have already begun in earnest.

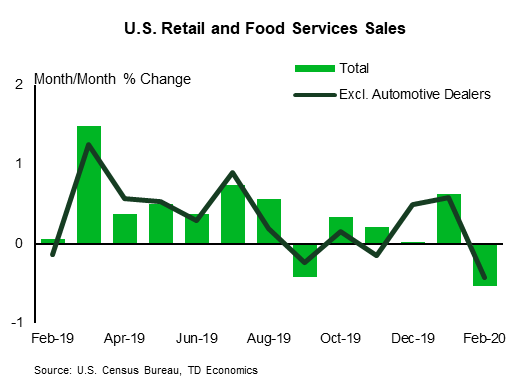

The initial jobless claims report continued to provide timely evidence of the pandemic’s massive impact on the U.S. labor market. Jobless claims remained at unprecedented highs for the third week in a row, coming in at 6.6 million last week (Chart 2). This brought the three-week tally to 16.8 million, which means that about one in every ten American workers has already filed for unemployment insurance. While fiscal and monetary measures should help stem the bleeding, the hemorrhage is likely to continue in the near-term, particularly as restrictive physical distancing measures remain in place. At this pace, we expect the unemployment rate to be well into the double digits in April.

All told, there may be some faint lights appearing at the end of the tunnel on the spread of COVID-19, which raises hopes for the potential for a move toward normal for the U.S. economy. However, the virus’ path remains uncertain and will continue to necessitate close monitoring. For now, sour economic data will continue to roll through, with April likely to be a particularly bad month..

Canada – COVID-19 Hammers Employment

It was a generally upbeat week in markets. In Canada, a rise in the price of oil on hopes of a global production cut agreement, helped support market sentiment. Stateside, markets were buoyed by additional Federal Reserve actions, as well as indications that the government would increase funding for forgivable payroll support loans.

This week brought some further adjustments to federal income support measures, notably changes to the qualification for the Canada Emergency Wage Support (CEWS). In effect, the government is working to make it easier for firms to qualify for the subsidy, which pays 75% of salary up to roughly $58k (see our report this week for further details). This, and the Canada Emergency Response Benefit (CERB) will be crucial bridges for Canadian households and businesses who have seen their incomes hit due to pandemic response measures. Indeed, reports suggest that more than 4 million applications had been received for EI/CERB as of Tuesday, with that number likely to rise given the government’s directions to stagger applications by birth month.

Application numbers speak to the scale of the economic impact of COVID-19, and the March job numbers speak to the speed. The employment survey was conducted mid-Month (March 15 to 21) when social distancing orders were just ramping up, but even at that time the measures drove some eye-popping figures. Employment dropped by more than a million positions on net, sending the unemployment rate to 7.8%. Given the ongoing pandemic, that figure understates the impact, as those that lost their job but didn’t look for work (presumably because of shutdowns and social distancing) aren’t counted as unemployed. Adding this group back in would mean an unemployment rate of 8.9%. The unusual nature of the shock can be seen in many aspects of the report. To choose just one example, temporary unemployment surged to half a million individuals, a never-before seen level (Chart 1). As severe as the figures are, it is safe to say that all these records are likely to be smashed again with the April data.

The dramatic moves in the employment report are likely to capture many headlines, but it wasn’t the only report to provide a sense of the impact COVID-19 will have on the Canadian economy. Statistics Canada provided its first ‘flash’ estimate of building permit issuance in March, based on roughly 30% of municipalities where data were available. The report indicated that a 23% year-on-year drop is likely (Chart 2). This decline was driven by significant pullback in Ontario, Quebec, and B.C., attributed by Statistics Canada to the early implementation of social distancing measures. The pandemic response has since intensified, including the narrowing of essential service lists in several provinces. This, together with reports that some municipalities have completely halted permit issuance suggests that when the April data become available, it may set a new record for the scale of the contraction. As the old saying goes, the economic data are going to get worse before it gets better thanks to COVID-19. For the next few months, we’re going to be firmly in the ‘getting worse’ side of that adage..

U.S: Upcoming Key Economic Releases

U.S. Retail Sales – March

Release Date: April 15, 2020

Previous: -0.5% m/m, ex-auto: -0.4%

TD Forecast: -7.5% m/m, ex-auto: -5.0%

Consensus: -6.8% m/m, ex-auto: -3.5%

Social distancing likely resulted in dramatic weakening in total retail sales. We are projecting a large 7.5% m/m drop in the headline number for March, following a -0.5% print in February. Although a good chunk of the decline in total sales is likely to be explained by tumbling auto sales, we expect the headline ex-auto segment to also post a significant decline (-5.0% m/m). Moreover, we forecast sales in the control group to come in flat m/m, as weakness was probably limited by extra strength in food and beverage stores, health and personal care stores and non-store retailers.

Canada: Upcoming Key Economic Releases

Bank of Canada Rate Decision

Release Date: April 15, 2020

Previous: 0.25%

TD Forecast: 0.25%

Consensus: 0.25%

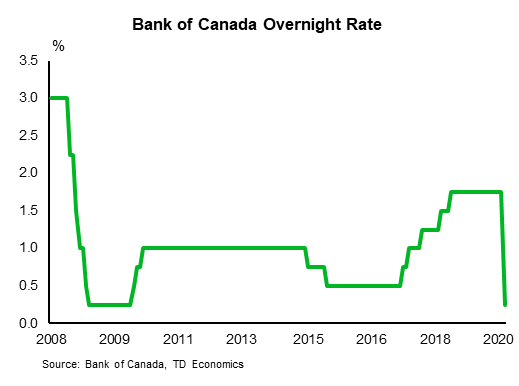

We expect the Bank of Canada to keep its remaining powder dry at the April meeting, leaving the overnight rate and Large Scale Asset Purchases (LSAP) unchanged at 0.25% and $5bn per week, after 100bp of intermeeting cuts since the March FAD. With the Bank sitting on its main policy levers, markets will turn their attention towards updated economic projections and the neutral rate estimate. While the former is likely to show a sharp contraction in 2020H1, we will be more interested in the annual averages for 2020 and 2021 for a barometer for Bank’s expectations around the duration of the shutdown and strength of the recovery. The April MPR also contains the Bank’s annual reassessment of the neutral rate which should reveal a modest downward revision from the current 2.25-3.25% range. March housing starts will give an early read on the impact of COVID-19 on the construction sector in Canada, with TD looking for a decline to a 180k annualized pace. Construction workers have been deemed essential in most jurisdictions that have closed non-essential firms, but anecdotal evidence suggests many are operating with reduced headcounts if it all. Furthermore, small business confidence in the construction industry fell to record lows in March which suggests a significant headwind to near-term residential investment.

Canadian Manufacturing Sales – February

Release Date: April 16, 2020

Previous: -0.2%

TD Forecast: 0.8%

Consensus: NA

TD looks for manufacturing sales to rise by 0.8% in February for one final increase before COVID shutdowns take hold next month. This follows broad strength in exports, led by a surge in aircraft shipments, and a sharp pickup for hours worked for the manufacturing industry. We look for gains to be led by durable goods, helped by higher auto production, while nondurables will be weighed down by the pullback in gasoline prices. The latter gives scope for an even larger increase on a volumes basis, although this will amount to little more than noise given the 35k jobs manufacturing sector jobs lost in March.