{kind=link}

Economic data has become sidelined during the virus crisis as the market’s attention has focused on policymakers’ response to the fast-spreading pandemic. However, as we now start receiving data for March – when the outbreak escalated outside of China – investors are likely to start taking more notice of the incoming releases. The flash PMI reports will be the first big numbers for March in the euro area, due on Tuesday at 09:00 GMT.

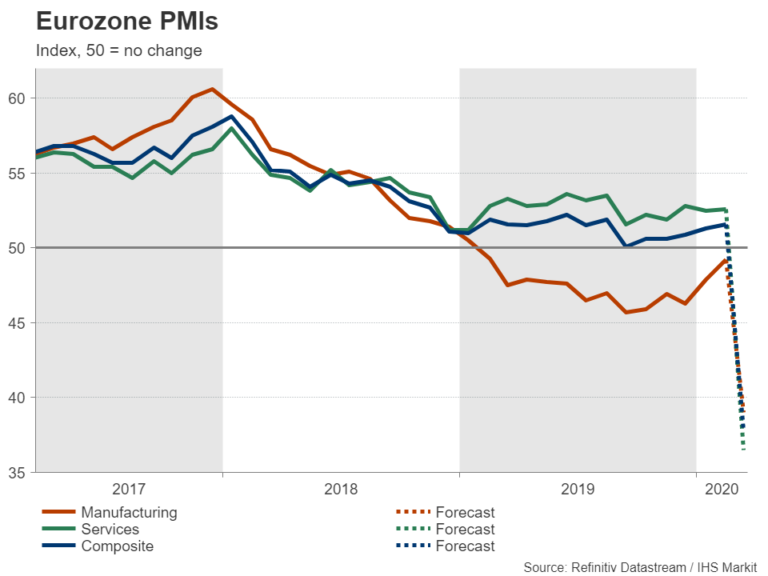

Flash PMIs to reveal virus damage

The Eurozone PMIs by IHS Markit are considered an accurate barometer of GDP growth so the recovery in both the services and manufacturing PMIs in late 2019 was seen as an encouraging sign that things were on the up. But although the region is no stranger to crises, the outbreak of the coronavirus could yet prove to be the biggest challenge the currency bloc has had to overcome.

Given that many parts of Europe started imposing lockdowns during March, analysts’ forecasts for the flash releases are pretty grim. The manufacturing PMI is expected to drop from 49.2 to 39.0 and the services PMI is forecast to plunge from 52.6 to 36.5. The composite PMI is projected to fall from 51.6 to 37.8.

Euro slide probably not over just yet

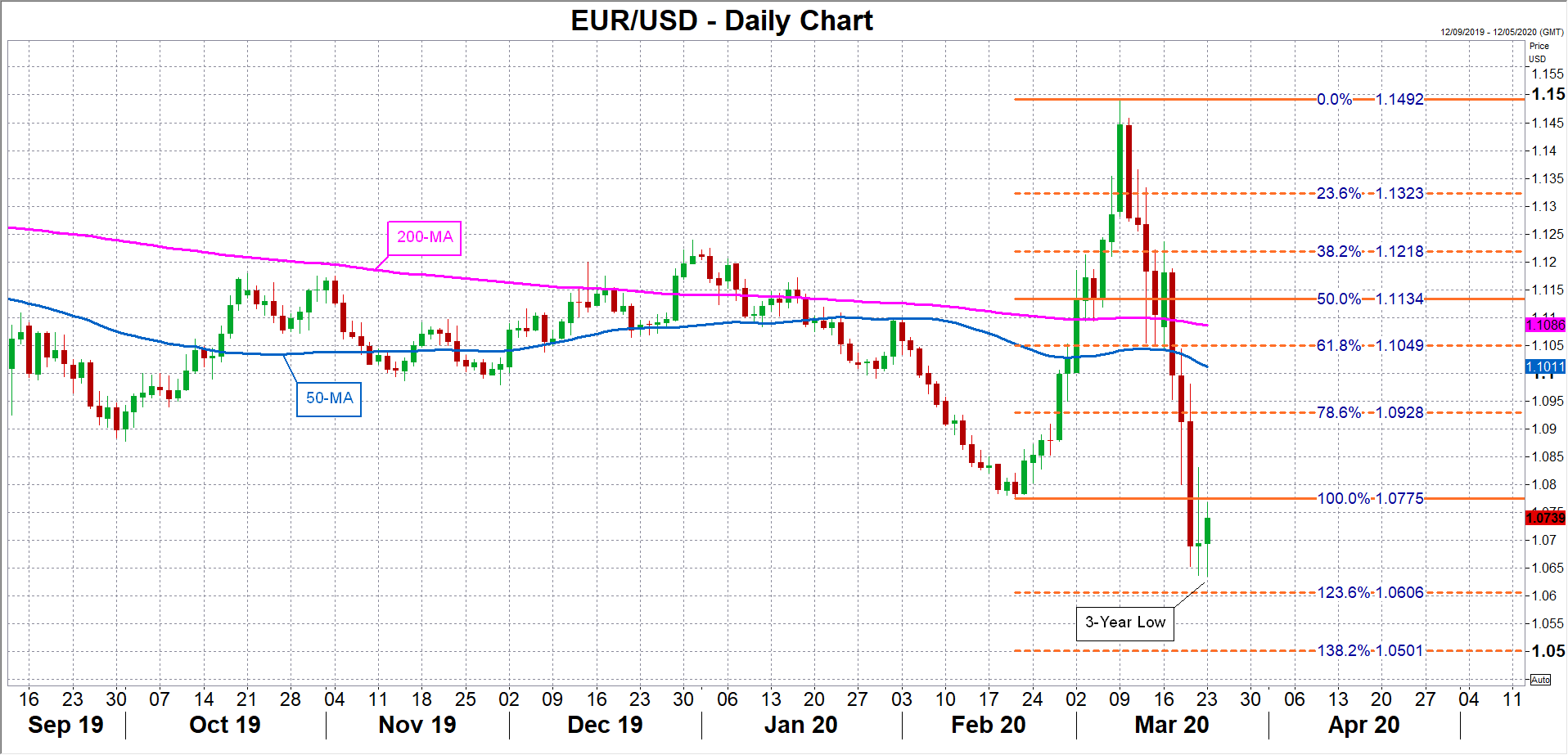

While the data is unlikely to significantly alter the Eurozone’s economic outlook, any negative shocks in the preliminary numbers could push the euro, which is reeling from the latest dollar rush, to fresh 3-year lows. Another bout of sell-off could stretch euro/dollar’s decline all the way down to the $1.06 level, which lies slightly below the 123.6% Fibonacci extension of the February-March uptrend, while steeper losses would open the way for the $1.05 barrier – the 138.2% Fibonacci.

On the upside, a positive surprise, accompanied by reduced market stress from the coronavirus, could help euro/dollar bounce above the February swing low of $1.0775.

So far, the euro’s carry trade status and the Eurozone’s current account surplus have provided the currency with some defence against the widespread sell-off in the FX markets in anything that isn’t the dollar or a safe haven. But going forward, how well the virus is being contained and the effectiveness of the already announced fiscal and monetary stimulus will be monitored to gauge potential downside risks for the euro.

More to come from ECB?

After coming under fire for not doing enough and for communication errors, the European Central Bank appears to have scaled up its response and announced last week that it will buy an additional 750 billion euros of public and private sector securities on top of its existing purchases.

The move seems to have gone some way in calming equity and bond markets and this likely means ECB policymakers will not be in a hurry to announce other bold measures anytime soon. Unless of course, the incoming data over the next few weeks, including the March PMIs, start to indicate that the Eurozone economy will require a lot more help than what’s already in the pipeline.