{kind=link}

For the 24 hours to 23:00 GMT, the EUR declined 0.69% against the USD and closed at 1.1178.

On the data front, Euro-zone’s industrial production rose 2.3% on a monthly basis in January, registering its first increase since August and more than market forecast for a rise of 1.4%. In the previous month, industrial production had recorded a revised drop of 1.8%. Separately, the European Central Bank (ECB), in its latest monetary policy decision, kept its interest rate unchanged at 0%, as expected. However, the central bank announced measures to support bank lending and expanded its asset purchase program by EUR120bn. Meanwhile, members expect the interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon.

In the US, the producer price index dropped to 0.6% on a monthly basis in February, more than market anticipations for a fall of 0.1%, compared to a rise of 0.5% in the previous month. Additionally, initial jobless claims unexpectedly eased to a level of 211.0K in the week end 7 March 2020, defying market expectations for a rise to a level of 218.0K. In the prior week, the number of initial jobless claims had recorded a revised level of 215.0K.

In the Asian session, at GMT0400, the pair is trading at 1.1215, with the EUR trading 0.33% higher against the USD from yesterday’s close.

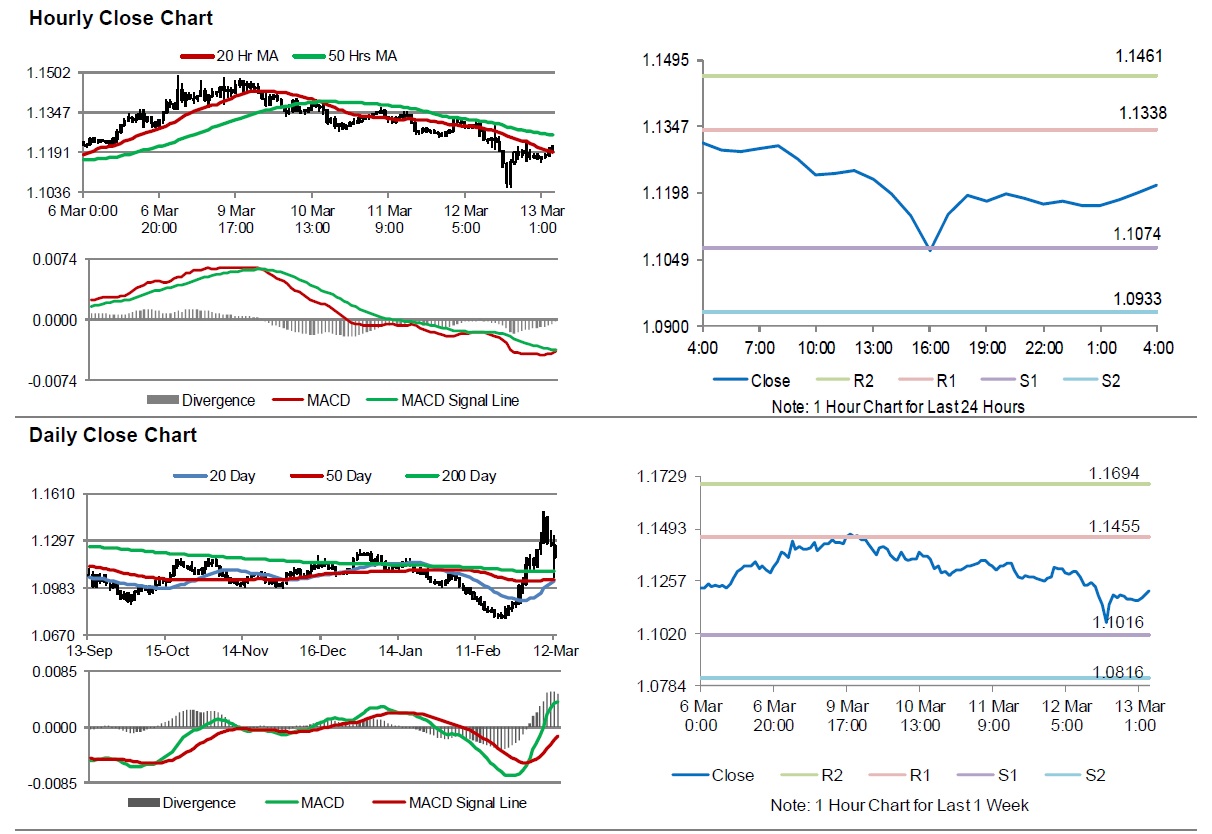

The pair is expected to find support at 1.1074, and a fall through could take it to the next support level of 1.0933. The pair is expected to find its first resistance at 1.1338, and a rise through could take it to the next resistance level of 1.1461.

Moving ahead, traders would keep an eye on Germany’s consumer price index for February, slated to release in a few hours. Later in the day, the US Michigan consumer sentiment index for March, would keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.