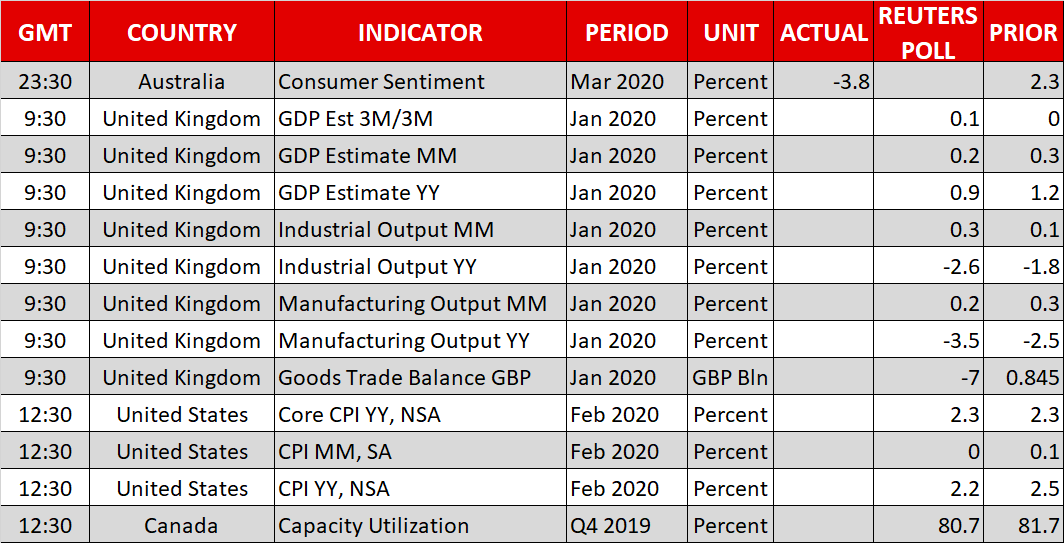

{kind=link}

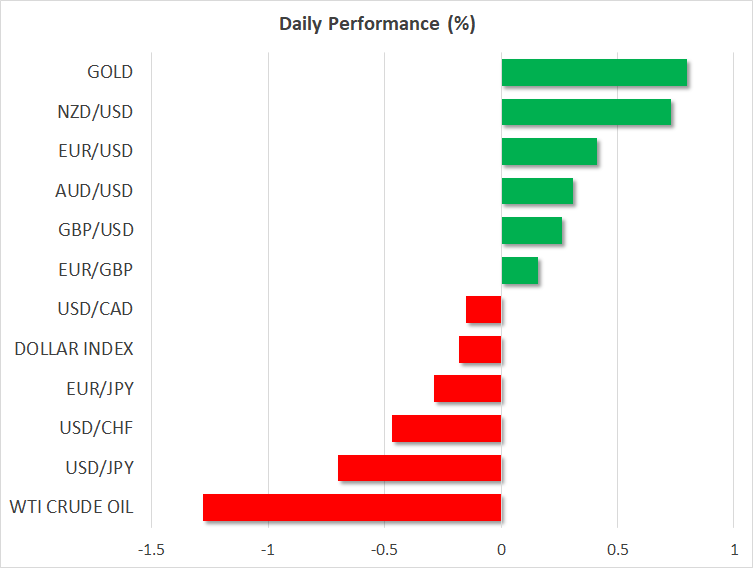

- Sterling recovers after BoE cut, on hopes for a stimulative budget later today

- Market mood sours again as news flow stays negative and Trump’s stimulus plans underwhelm

- Dollar stages a comeback as US Treasury yields rebound somewhat

BoE mimics Fed, slashes rates between meetings

The Bank of England (BoE) took a page out of the Fed’s book today, unexpectedly cutting rates by 50 basis points from 0.75% to 0.25% between scheduled meetings to negate the economic impact of the coronavirus. The central bank also set up a special lending scheme aimed at boosting loans to small and medium sized firms, to help them cope with cash flow problems and ultimately prevent this temporary shock from causing long-term damage.

Cable fell by one big figure on the news, but quickly recouped all its losses to trade even higher, as the move was more or less priced in for the March 26 meeting and the only real surprise was the timing. Another reason the pound wasn’t spooked by the cut is that the UK government budget is due to be unveiled later today (12:30 GMT) and with the BoE choosing this specific day to act, this smells of coordinated fiscal-monetary stimulus to recharge the economy.

In other words, the upcoming budget may also be quite large as the UK authorities seem to be trying to get the maximum ‘bang for their buck’ by synchronizing their actions.

While the pound may bask in the sun today, bolstered by markets upgrading their expectations for the British economy amid the sizeable and coordinated stimulus measures, the bigger outlook is still clouded. The Brexit negotiations have finally resumed and judging by recent comments by PM Johnson about not adhering to EU rules and being prepared to walk away from the talks, it may be just a matter of time before the threat of a no-deal exit comes back to the table to haunt sterling.

Easy come, easy go?

Global markets continue to trade like a rollercoaster, as investors weigh the policy responses and the promises of fiscal stimulus against the sustained barrage of negative virus headlines. Wall Street closed 5% higher on Tuesday, albeit in a very volatile session where the major indices even traded negative at one point, while futures point to another 1.5% drop today for the S&P 500.

While traders initially took heart by signals the White House is preparing powerful stimulus measures, the optimism started to fade once details rolled in, with President Trump picking a temporary payrolls tax cut as his weapon of choice. That received a cold reception from lawmakers in Congress, as it would fall short of providing paid sick leave to help contain the spread of the virus, overwhelmingly benefit higher income earners, and balloon the enormous deficit even further.

Overall, Trump’s response seemed out of step with Congress, which likely reminded markets that any relief might be delayed by partisan politics in Washington DC, especially in an election year. American news flow around the virus was exceptionally negative too, with many events being cancelled and the number of cases soaring.

Dollar comes back to life

In the FX market, the safe-haven yen was the worst performer on Tuesday while the greenback staged a major comeback, drawing strength from the rebound in US Treasury yields and the broader risk-on mood.

The dollar continues to be positively correlated with risk sentiment and is therefore on the back foot today as risk aversion has returned, prompting a further unwind of carry trades that benefits funding currencies like euro.

That said, this won’t continue indefinitely. At some point, the unwinding process will run its course and the dollar will likely reclaim its status as safe haven, as it always does when the global economy goes south and investors seek shelter.

US CPI data today are unlikely to be a game changer for Fed policy – a 75bp rate cut next week is all but certain.