{kind=link}

- Risk sentiment recovers on Tuesday, after a catastrophic Monday

- However, the rebound is relatively minor – a sign that concerns remain and that this may be a temporary calm

- Dollar stages a comeback, US Democratic primary continues today

Yen pulls back, stocks recover on ‘turnaround Tuesday’

After a wild session on Monday that saw riskier assets crash and burn, with the S&P 500 plummeting a stunning 7.6% and crude oil sinking by nearly 25%, markets have calmed down somewhat today, bolstered by hopes for fiscal stimulus. The White House floated several measures to soften the blow from the virus outbreak, including a possible payroll tax cut for American workers, while Japan’s government said it will unveil another package of fiscal steps today.

News about the spread of the virus were mixed, though. On the bright side, the pace of new infections in South Korea has slowed drastically, giving investors confidence that a well organized containment plan can actually pay dividends. Something similar is playing out in China, where the number of new cases continues to slow, so much so that President Xi visited Wuhan earlier today, the city at the epicenter of the outbreak.

However, the situation in Europe is worsening. Italy expanded its quarantine yesterday to include its entire country, meaning that Italians can no longer travel freely, while the number of infections in Germany, France, and Spain is rising rapidly. Over in the US, the state of affairs is not as dire according to the official numbers, but those may be artificially deflated due to a shortage of testing kits. As more Americans get tested in the coming weeks, that might change.

Dead cat bounce?

The question right now is whether this recovery in risk sentiment is durable, or whether this is merely a temporary calm before the next storm. On the margin, the latter seems more likely for now.

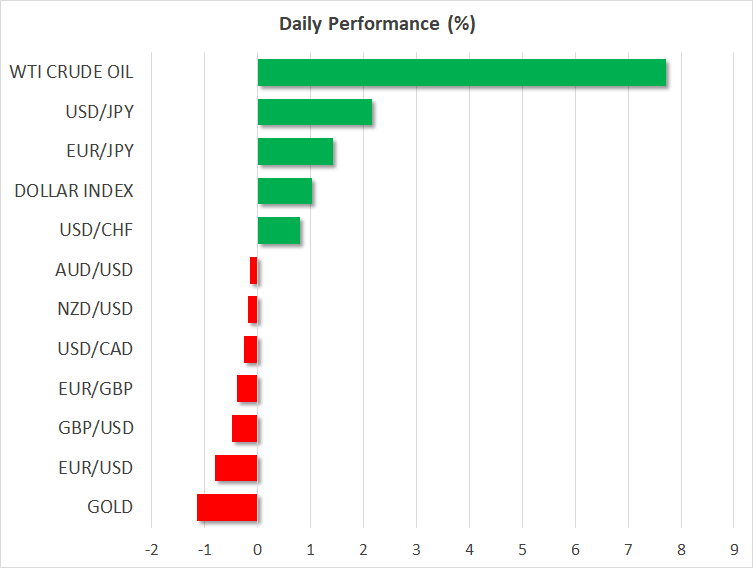

First off, the scale of this rebound is underwhelming. For instance, futures are pointing to a ~3.5% higher open on Wall Street today, which doesn’t even cover half the losses from yesterday. Oil prices haven’t even clawed back a third of their plunge. Meanwhile, the commodity-linked Australian and New Zealand dollars are in the red against the greenback today, signaling that concerns about the global economy have merely been put on ice, they haven’t evaporated.

The situation in China may be improving and even the devastated Hubei province seems ready to resume operations before long – the question is, what happens if Chinese factories go back online but demand for those goods from Europe and the US falters? In other words, while the primary supply side shock may fade soon, a secondary demand shock might emerge to fill that void as an increasingly frightened consumer reins back spending.

Dollar shows signs of life again

The world’s reserve currency is recovering ground on Tuesday, drawing strength from a rebound in US Treasury yields as investors bet that the Fed won’t have to cut interest rates as aggressively to shield the economy if the White House rolls out tax cuts.

The greenback has been behaving like a ‘risk on’ currency lately, so assuming that the worst is not over for risk sentiment, there might be some more pain in store in the near term, especially if the ECB doesn’t live up to market expectations for a rate cut this week.

That being said, the dollar still looks attractive in the bigger picture. The US economy was already much stronger than the Eurozone before the virus outbreak, and US authorities are getting ahead of this risk by adding powerful stimulus to shield their economy. The Europeans aren’t, and with Italy likely to enter a recession soon, the entire bloc could follow.

As for today, markets will continue to scrutinize virus-related news, though politics might also come back into focus as the US Democratic primary continues with another six states voting today. After Super Tuesday, Joe Biden has retaken a commanding lead and that has likely underpinned stocks, since betting markets give him an almost 90% probability of winning. Therefore, the risk now is that Bernie Sanders stages another comeback, which might add another dimension of pain for equities given his left-wing agenda.