- Investors in panic mode as oil collapses, sending shockwaves through markets

- Global stocks plunge, commodity currencies flash crash, dollar in agony as markets discount aggressive Fed cuts

- Japanese yen the main winner, gold briefly tops $1700, euro capitalizes

Markets in mayhem as oil price war compounds virus fears

It’s been a dramatic beginning to the week in financial markets, with risk aversion being the only game in town as the weekend saw the OPEC+ alliance come to an end, igniting fears of an imminent oil price war that exacerbates the supply side shock from the virus. Talks of deeper output cuts between OPEC and Russia fell apart, ending a three-year long collaboration and raising speculation that the two sides will now fight for market share with US shale producers by ramping up their own production.

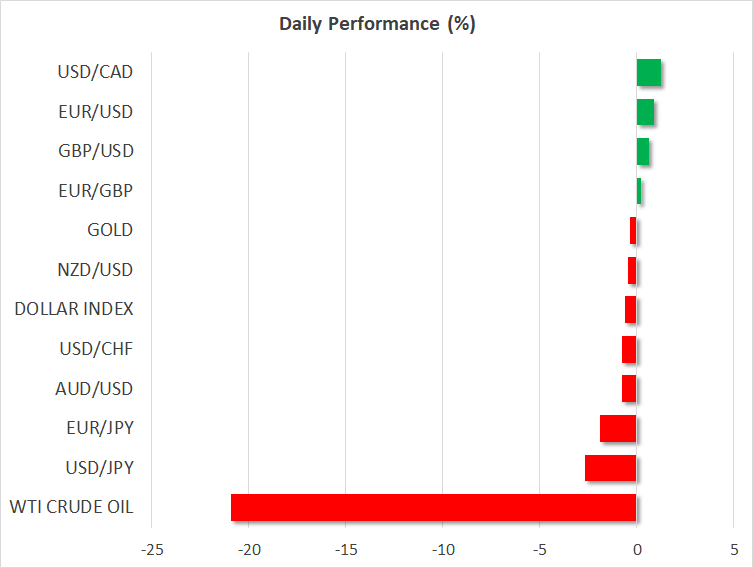

WTI crude fell by more than 20% to approach its record lows amid concerns that global oil supply is about to surge to unprecedented levels at a time when demand is plummeting, with the travel industry in ruins after the virus hit.

The suffering wasn’t confined to energy markets though. Stock indices were a sea of red in every region, with most European bourses down by more than 7% at the time of writing and while futures point to a 5% lower open for the S&P 500, that’s only because US circuit breakers are preventing even sharper losses. In the FX arena, the oil-sensitive Canadian dollar is the worst performer, followed by the Australian and New Zealand dollars, both of which experienced a ‘flash crash’ but later recovered as the US dollar lost ground.

It seems that the OPEC fallout was the straw the broke the camel’s back. With most of Northern Italy placed under quarantine and the US government acting painfully slowly to contain the virus, speculation about the negative impact on global demand is running wild, and an oil price shock is the last thing the world economy needs right now.

Fed rate cut bets mount, pushing dollar lower

Unsurprisingly, markets are hoping central banks will step up again. A ‘triple’ Fed rate cut (75 basis points) is now fully priced in for the March 18 meeting, which has seen the yield on the 10-year Treasury note dive to a new all-time low of 0.34% today, in turn pushing the dollar even lower as its interest rate advantage has all but evaporated. All this, despite a strong US jobs report on Friday.

The oil price plunge is a game changer for central banks. Up until now, everyone admitted rate cuts wouldn’t do much to fix supply chains, and the easing was mainly aimed at shoring up confidence. However, plummeting oil prices mean that inflation expectations are falling even faster, which adds another dimension to the concerns for central bankers.

But ECB might be a different story

Still, it’s highly questionable if the ECB will join the rate-cutting party this week. Markets are fully pricing in a 10 basis-points rate cut, but the central bank is highly divided and almost out of ammunition, so by no means is it ‘certain’ that it will cut rates. Rather, it might opt for more specific measures, like providing ultra-cheap loans to businesses affected by the virus. If so, that would argue for more upside in euro/dollar this week.

Likewise, the risks surrounding dollar/yen look tilted to the downside in the very near term, and a test of the ¥100 area might be on the cards in an environment of heightened risk aversion and falling inflation expectations.

Overall, it’s hard to envisage a real turnaround in risk sentiment for now. Central banks are already throwing everything they have at this problem but that hasn’t even been enough to halt the plunge in stock markets, and there’s little scope for news flow to improve with the virus spreading so quickly in the US and Europe.

{kind=link}